Investment Summary

Loss of More than RMB60 Million in the Third Quarter

NavInfo recorded revenue of RMB451 million in Q3 2019, down 15.34% yoy. A net loss of RMB61,415,500 was recorded from singer-quarter result, approximately the lower limit of the result guidance interval, which represents a profit of RMB55.97 million in the same period last year.

The revenue in the first three quarters was basically the same, up 0.76% yoy to RMB1,535 million. The net profit attributable to the parent company was RMB24,184,800, down 89% yoy, with EPS of RMB0.01. The net profit attributable to the parent company in Q1 and Q2 decreased by 43% and 52% yoy to RMB42.03 million and RMB43.57 million, respectively.

Drag of Slump of Domestic Vehicle Market and Investment Loss

The domestic passenger vehicles in the first three quarters of 2019 decreased by 11.7% yoy. Due to weak demand and intense market competition, the pre-installed navigation map business, which accounted for 40% of the revenue, was dragged. The main clients of chip business (which accounted for one-sixth of the revenue), was self-owned brands, whose sales down 18.6% in the first nine months, which affected the result of chip business of the Company. Therefore, the gross margin in Q3 decreased by 12.54 ppts to 66.63%, and the gross margin in the first quarters decreased by 5.14 ppts to 71.9%.

On the other hand, the Company divested AUTOAI, the entity of Internet of Vehicles of passenger vehicles in 2018. AUTOAI was no longer consolidated with the Company in 2019, which affected the revenue (AUTOAI recorded revenue of RMB105 million in 2018), and relevant profit and loss were included in investment gains. After the divestment, the input into Internet of Vehicles continuously increased, which scaled up the loss and dragged the investment gains of the Company in the first three quarters for loss of RMB33.83 million, RMB52.39 million and RMB58.53 million, respectively.

High Investment into R&D and Result under Pressure in a Short Time

The sales expense ratio decreased by 0.7 ppts to 4.75% in the first three quarters, mainly due to the exclusion of sales promotion expense of Internet of Vehicles of passenger vehicles. The administration+R&D expense ratio decreased by 0.64 ppts to 64.37%, still maintain a high level. At present, the R&D input into fields such as the Self-Driving, Internet of Vehicles and chip continuously increased, which would still place the result under great pressure in the future one to two years. Before the maturity of new technologies and formal implementation of product commercialization, high R&D fee is the prerequisite to take advantages in the coming era of intelligent driving, and would lay the foundation for NavInfo to further build a five-in-one technology advantage of "Digital Map+ Internet of Vehicles+ Self-Driving+ Big Data+ Chip", as well as an industry leading position in Self-Driving field.

Daybreak after Discontinued Result

For Self-Driving at or above L3, only NavInfo as well as AMap of Ali and Qianxun SI could provide high-precision maps and high-precision positioning at the same time in China at present. The barriers of the industry are obvious. For high-precision map, NavInfo obtained the first production order of L3 passenger vehicle self-driving map in China. The high-precision positioning business of the subsidiary Sixents Technology has achieved the market leading level. NavInfo currently issued the announcement that Huawei purchased its high-precision map data products and services to show that the product strengthen and industry status were approved, which marked the formal implementation of Self-Driving cooperation project with Huawei. It is expected that the market would be opened up subsequently. AutoChips recently successfully developed the chip of TPMS, and had the mass-production capacity, which is expected to break the monopoly of Infineon in chip of TPMS.

From H2 2019, phased progress was made in market expansion: NavInfo obtained the orders from BMW, MITSUBISHI ELECTRIC, Ministry of Industry and Information Technology (MIIT), Ministry of Public Security, Daimule and Huawei, which would gradually contribute increment to the Company from 2021, and the elastic of result would be large in the future.

Valuation

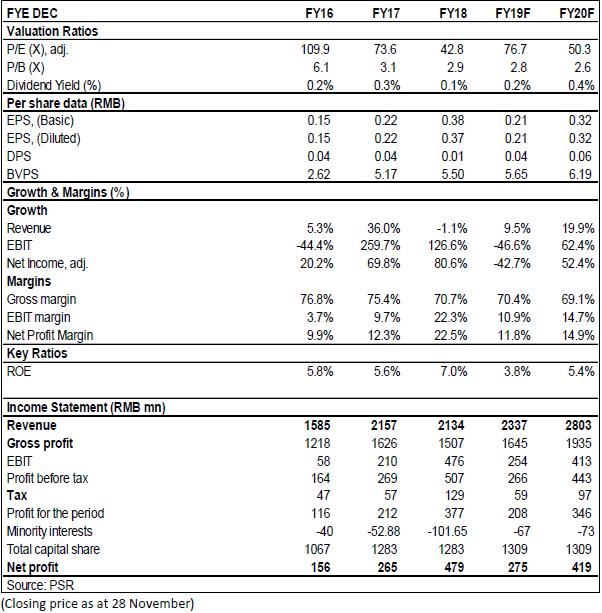

Although the profit of NavInfo would be affected by no expansion of new products and slowing domestic vehicle market of traditional navigation map and chip business, we believe that the Company is expected to welcome the turning point of result with the rapid advance of Self-Driving, and the growth space would be broad in the future. As analyzed above, we expected diluted EPS of the Company to RMB 0.21 and 0.32 of 2019/2020. And we accordingly gave the target price to 20. "Buy" rating. (Closing price as at 28 November)

Financials

Click Here for PDF format...