Investment Summary

Kingsoft's overall performance in 2019Q3 was better than expected. The online game business meets expectations; the increase in corporate cloud revenue drives the rapid growth of cloud services business; the enhanced user engagement and increased paid users promotes the strong growth from value-added services revunue of WPS Office personal edition.

Result update

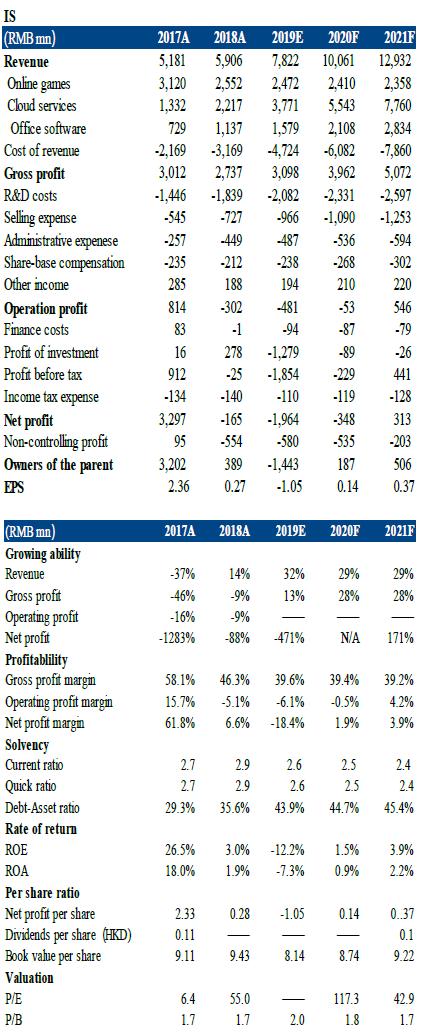

Kingsoft announced its 2019Q3 results on November 13th: revenue for the third quarter of 2019 increased 32% year-on-year and 8% quarter-on-quarter to RMB2,022.9 million (RMB, the same below). Gross profit increased 18% year-on-year and 15% quarter-on-quarter to RMB822.9 million. Gross profit margin decreased by four percentage points year-onyear and increased by three percentage points quarter-on-quarter to 41%. The year-on-year decrease of the gross profit margin was largely due to our change in sales mix. The quarter-on-quarter increase of gross profit margin mainly reflected improved operating efficiency of cloud business. Profit attributable to owners of the parent was RMB36.1 million for the three months ended 30 September 2019.

Online games:New games launch next year, performance is expected to recover

Revenue from Online games for Q3 was 664 million yuan, a year-on-year decrease of 2%. The year-on-year decrease in revenue was mainly reflected decreased revenue from existing games, partially offset by the revenue contribution from newly released mobile games this year. JX Online III PC game will be updated at the end of the year. A new mobile game Double Life World (雙生視界) was launched in Japan and the domestic version of the game will be released in the near future. In addition, the company also has three new mobile games in stock and is expected to go online in 2020. With the update of old games and the promotion of mobile game diversified product strategies, the game business is expected to recover in 2020.

Cloud services: maintain rapid growth, Q3 gross margin turned positive

Revenue from the cloud services for the third quarter of 2019 increased 62% year-on-year and 6% quarter-on-quarter to RMB976.3 million. The rapid year-on-year increase was mainly driven by an increase of customer usage from mobile video sector and increased revenue from enterprise cloud. Meanwhile, Q3 cloud business gross margin turned positive. At present, cloud services continues to expand its field of game cloud, government cloud, financial cloud and others. It is believed that the cloud business can still maintain rapid growth, and it is not difficult to meet management's 70% growth guidance for the whole year. The company issued an announcement on November 14 that the company is considering a possible spin-off and separate listing of Kingsoft Cloud Holdings Limited , but did not announce any further information.

Office software: Strong growth of member value-added services and has been listed on Sci-Tech board

Revenue from the office software and services and others for the third quarter of 2019 increased 50% year-on-year and decreased 1% quarter-on-quarter to RMB383.1 million. The year-on-year increase was mainly due to strong growth from value-added services of WPS Office personal edition. WPS` user engagement and the paid users continue to rise. The number of paid users for Q3 increased by 120% year-on-year, and it is expected to record a growth of 40% for the whole year. WPS has also officially released an international version for overseas markets. In addition, Office software further explored the government and enterprise user market, and the domestic licensed software business is expected to record a strong improvement.

Office software was officially listed on the Sci-Tech board on November 18. Kingsoft held 52.71% share of Office software after the listing.

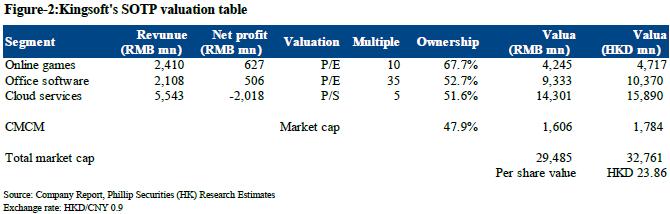

Valuation

We forecast the company's revenue for 2019/2020 to be 7.82 billion yuan / 1.06 billion yuan and adjusted net profit to be -1.44 billion yuan / 1.887 billion yuan. We adopted sum of the parts valuation by dividing the business into three parts: 1) Online games (P/E), 2) Cloud business (P/S), and 3) Office software (P/E). Due to the weak performance of the online game business, it is given a P / E ratio of 10x; the prospect of WPS is optimistic, given a P / E ratio of 35 times; and the cloud business is given a 5 times price-to-sales ratio. The SOTP target price is HKD 23.86, 35.6% higher than the current price. We remain “Buy” rating. (Current price as of December 4, 2019)

Risk

1. Tighter regulation

2. Respond of new mobile games less than expected

3. Fierce competition in cloud business

Financials

Click Here for PDF format...