|

JIANGXI COPPER(358)

Analysis:

The principal business of Jianxi Copper (358) covers gold and copper mining and dressing, smelting and processing, extraction and processing of the precious metals and scattered metals, sulphuric chemistry as well as finance and trading fields. It has established the complete industrial chain integrated with exploration, mining, ore dressing, smelting and processing in copper and related non-ferrous metal fields. The Group has 6 mines with production which it owns 100% stake. In the first half of 2019, the Group successfully achieved the production plan for all products and produced 749,300 tonnes of copper cathode, representing a year-on-year increase of 3.51%; 102,000 tonnes of copper concentrates, representing a year-on-year increase of 0.2%. (I do not hold the above stock)

Strategy:

Buy-in Price: $9.80, Target Price: $11.00, Cut Loss Price: $9.20

|

XIAOMI(1810)

Analysis:

Xiaomi Group announced the third quarter 2019 performance report, with total revenue of 53.7 billion in the third quarter, an increase of 5.5% year-on-year. Adjusted net profit was 3.5 billion yuan, a year-on-year increase of 20.3%. So far, Xiaomi achieved a net profit of 9.2 billion yuan in the first three quarters of 2019, exceeding total revenue of last year. Among them, the revenue of the smart phone segment reached 32.3 billion yuan, and smart phone sales reached 32.1 million. According to Canalys statistics, the company`s global smartphone shipments market share in the third quarter of 2019 was 9.2%, ranking fourth. Revenue from IoT and consumer products was 15.6 billion yuan, a year-on-year increase of 44.4%. Global shipments of smart TVs reached 3.1 million units in the third quarter, a year-on-year increase of 59.8%. Internet service revenue reached 5.3 billion yuan, a year-on-year increase of 12.3%. Advertising business revenue reached 2.9 billion yuan, a year-on-year decrease of 9.0%. Fintech business revenue reached 1 billion yuan, a year-on-year increase of 91.2%. In addition, Xiaomi`s overseas market revenue in the third quarter was 26.1 billion yuan, a year-on-year increase of 17.2%. Revenue from overseas markets accounted for 48.7% of Xiaomi`s total revenue. Xiaomi introduced the 5G mobile phone Redmi K30 with a retail price of 1,999 yuan (RMB) on December 10, and at least 10 5G mobile phones will be introduced next year.

Strategy:

Buy-in Price: $9.90, Target Price: $11.25, Cut Loss Price: $8.85

|

|

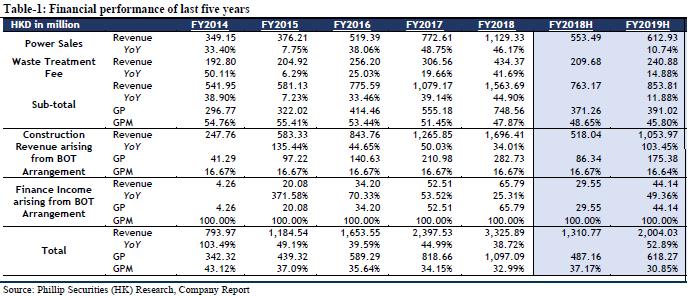

CANVEST ENV (1381.HK) - New processing capacity in line with expectations

Company UpdateFrom September 2019, the company has obtained the following waste incineration power generation projects: 1. On September 10, Canvest Kewei Environmental Investment (Guangdong) Company Limited, a wholly-owned subsidiary of the company, was awarded the concession right in relation to the waste-to-energy process plant concession project located in Wuchang City, Harbin City, Heilongjiang Province, the total daily solid waste processing capacity of the Wuchang WTE Plant shall be 600 tonnes. 2. On November 26, Kewei acquired the entire equity interest of Zhongshan Guangye at a total consideration of RMB340 million. Zhongshan Guangye owns the concession right to operate the Zhongshan WTE Plant in Zhongshan, Guangdong. The daily municipal solid waste processing capacity of the Zhongshan WTE Plant is 1,040 tonnes. In 2018, the revenue of Zhongshan Guangye was RMB 98.31 million, profit after income tax was RMB 5.9 million, net asset value as at 31 December 2018 was RMB 210 million. The company expects that the acquisition will help business development in the Guangdong-Hong Kong-Macao Greater Bay Area. 3. On December 6, Kewei was awarded the concession right in relation to the circular economy industrial park phase I of waste-to-energy process plant and kitchen waste treatment public-private-partnership (“PPP”) project located in Jingjiang City, Taizhou City, Jiangsu Province. The total daily municipal solid waste processing capacity of the Jingjiang WTE Plant shall be 1,200 tonnes. The Jingjiang WTE Plant shall be constructed in two phases, of which the Processing Capacity of phase I shall be 800 tonnes and phase II shall be 400 tonnes. As of 22 August 2019, the operating, secured, announced and under management agreement daily MSW processing capacity of 25 projects was 36,590 tonnes. When taking into account of the newly added waste incineration power generation projects since September 2019, the company's total processing capacity so far is about 39,430 tonnes, and the annual new processing capacity is about 10,390 tonnes, an increase of 35.8% YoY, which has completed the target of the company (more than 10,000 tonnes new capacity and 30% growth YoY). In addition, Johnson Holdings (1955.HK) was successfully listed on the Hong Kong Stock Exchange on October 16, 2019. Johnson Limited is a leading environmental health service provider that provides a wide range of environmental health services in Hong Kong. We are still optimistic about the possible cooperation between the company and Johnson in the Guangdong-Hong Kong-Macao Greater Bay Area on project level. Yangtze River Delta Regional Integration Development Plan Issued, Promising in Cooperation with SIICOn December 1, 2019, the Central Committee of the Communist Party of China and the State Council issued the "Outline of the Yangtze River Delta Regional Integration Development Plan", and the development of the Yangtze River Delta regional integration development has become a national strategy. The planning scope covers the whole area of Shanghai, Jiangsu Province, Zhejiang Province, and Anhui Province (with an area of 358,000 square kilometers). The planning period is up to year 2025, and the outlook period is up to year 2035. The Plan calls for accelerating the construction of infrastructure such as garbage and sewage collection and treatment covering urban and rural areas, promoting the centralized disposal of garbage and sewage, and basically establishing a coordinated ecological and environmental supervision system, and further improving the quality of the regional ecological environment. On the other hand, with the promotion of the waste separation and treatment policy, it will directly lead to the increased demand for sanitation equipment and services for front-end classified disposal, classified collection, and classified transportation. By the end of 2020, 46 key cities are expected to be basically completed domestic waste sorting and processing system. On August 21, 2019, Canvest Environmental Investment, an indirect wholly-owned subsidiary of the company, entered into a joint venture agreement with the shareholders of Shanghai Industrial Environmental Technology (a direct wholly-owned subsidiary of SIIC Environment) to set up a joint venture. The joint company will focus on the investment, construction and operation of waste incineration power projects in the Yangtze River Delta. We expect that with the establishment of a project company with SIIC, the company will further strengthen the search for cooperation opportunities in the Yangtze River Delta region, and with the issue of the Yangtze River Delta development plan and the new regulations for "the most stringent" waste sorting further promoted, though the amount of waste incineration might be reduced, but it is believed that it will also promote the company to continuously adjust its business model, further strengthen cost control, and actively seek the integration of the industrial chain, which is beneficial to the company's long-term development. Maintain “BUY” investment ratingWe maintain a TP of HKD 5.07, corresponding to FY19/FY20/FY21 14.21x/12.14x/10.26x PE with a +52.16% potential upside compared with CP of HKD 3.33 as of December 6, 2019, we maintain “BUY” investment rating.

RiskFail expectations of project progress; policy risk of electricity price allowance; fail expectations of acquisition of new projects Financials

Click Here for PDF format...

| Recommendation on 13-12-2019 | | Recommendation | BUY | | Price on Recommendation Date | $ 3.330 | | Suggested purchase price | N/A | | Target Price | $ 5.070 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|