Investment Summary

Aoyuan Health Life's revenue grew rapidly in 1H20. It recorded approximately RMB 547 million, an increase of 39.5% from approximately RMB 392 million in the same period last year, of which approximately 75.4% came from revenue from the property management service segment, an increase of 43.4% YoY, and another 24.6% of revenue came from the business management services segment, an increase of 28.8% YoY. The company's current total construction area under management is approximately 16.1 million square meters, an increase of approximately 1 million square meters from the end of last year. In addition to the two acquisitions in the first half of the year, EASY LIFE SMART COMMUNITY SERVICES GROUP CO. (樂生活) and Ningbo Hongjian, the GFA under management is expected to reach 45 million square meters. The data for the 1H shows the company's revenue before consolidation which new acquisitions are not included. Revenue growth reflects the continued good rate of company's organic growth.

Changes in the company's revenue structure and increased business GPM

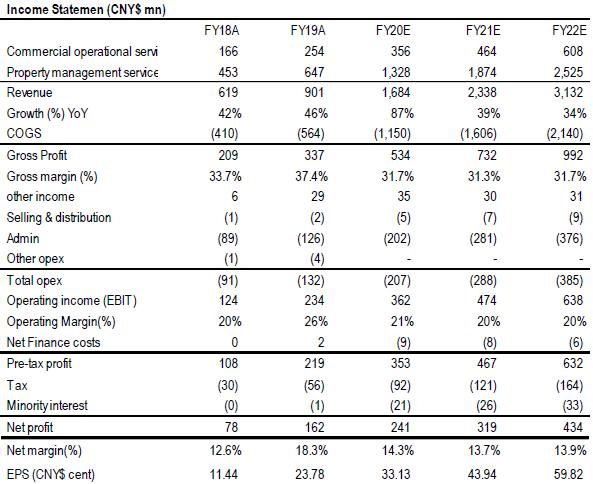

The company's GPM in 1H further improved compared with the same period last year, and the overall GPM reached 40.1%, an increase of 0.5 percentage points from 39.6% in the same period last year. In terms of segments, the property management service segment and the commercial management property segment accounted for 75.4% and 24.6% of revenue, respectively. Compared with the same period last year, the revenue share of the property management segment increased. Look more detail to the business segment, the GPM of the property management segment improved significantly compared with last year, reaching 39.7%, mainly due to the significant increase in revenue from Major owners value-added services (formerly known as sales assistance services), which increased by approximately 55.27%, accounting for approximately 22.1% of the company's total revenue in 1H. The GPM of this business is higher in the residential property management sector. But on the other hand, the company's commercial management services segment's GPM has declined, from 46.1% in the same period last year, down 4.6% to 41.5%, mainly due to the decrease in revenue from Market positioning and business tenant sourcing services.

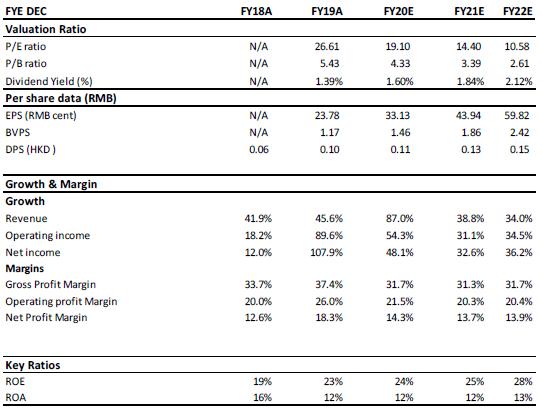

The NPM during the period was 20.4%, a decrease of 2.6% YoY. This was mainly due to the decrease in additional interest expenses and net foreign exchange income incurred by the increase of bank loans by approximately RMB 100 million during the period. The management further explained that the company did not intend to conduct equity financing in 2H, and the new loans are used as reserves for potential M&A activities.The company's two acquisitions in the past six months have effectively expanded the company's residential management services. If the company can effectively carry out management, gross profit will be further improved in the future. We expect the company's 2020 and 2021 earnings per share to be CNY 33.07 cent and CNY 43.06 cent, giving a target price of HK$9.60 corresponding to the expected P/E ratio of 26.1x/20.1x in 2020 and 2021.

The acquisition is expected to be completed within a month

The company's acquisition of an 80% interest in Easy Life is expected to be completed within August, and the management is also expected to complete the consolidation in August. As Easy Life is listed on the Beijing New OTC(Over the Counter) Market (新三板), the acquisition process is relatively complicated. The job of 2H is how to properly carry out post-investment work. Easy Life has a large gap with the company in terms of profitability. According to Easy Life's FY19 annual report, its GPM is 17.10%. The company stated that the acquisition of Easy Life mainly values the company's business model, and at the same time value the expansion capabilities of it to deploy national and global services.

COVID-19 provided opportunities for the company. During the period, the company is committed to developing home-based services to meet customers` new consumption patterns and provide different value-added services, such as household daily necessities distribution, housekeeping cleaning, laundry services, and disinfection. The epidemic provides a good entry point for community value-added services. At the same time, the company can increase customer stickiness and enhance the sustainability of community value-added services by improving customer satisfaction.

Six new malls are expected to open in the second half of the year

In the commercial operation segment, the growth rate slowed down in 1H, with an overall increase of approximately 28.8%. The revenue from commercial operations and management services increased by 44.6% compared with last year, while the revenue from Market positioning and business tenant sourcing services decreased by approximately 12.1%. The epidemic has delayed malls that were originally scheduled to open in the 1H to the end of the year. The company expects that six new malls will open in the 2H. Nearly 80% of the company's malls have resumed, and some of them have returned to pre-epidemic levels.

Partner with leading companies to develop medical beauty business

In the first half of the year, the company continued to co-brand with the well-known Korean cosmetics company "Cosmax" to develop cosmetics and cosmetic product packages. In addition, in the first half of March, it completed the acquisition of 5% equity in Luxeme as a strategic investment in the company's medical beauty business. Luxeme is the largest medical beauty chain group in Zhejiang Province, headquartered in Hangzhou. The main purpose of this acquisition is to enhance the quality and brand influence of the company's medical beauty business through cooperation with domestic professional medical beauty groups. During the period, the company's self-operated medical beauty business incurred losses in the past, which had little impact on the company as a whole. The losses are expected to gradually narrow in 2H. At present, the main purpose of self-operated stores is talent training center, which cultivates a good medical beauty management team and prepares for future business expansion to achieve rapid development and performance contribution.

Implement health care business pilot

In terms of health care services, the company develops in the form of ŕ+3" model and ŕ+1+N" health care system layout. The ŕ+3" model refers to the use of community elderly care as the entrance to comprehensively promote home care, institutional care and residential care services. ŕ+1+N" refers to building an online smart health platform, connecting offline health cards, and providing health care. There are more than 70 comprehensive health care services in 3 categories, “healthy aging, happy aging, and learning while aging” for elderly people with different health conditions. In 1H20, the company's "property services + elderly care services" community health care brand "Aoyue Home" was officially launched for trial in the three communities under management—Guangzhou Panyu Jinye Villa Garden (廣州番禺金業別墅花園), Guangzhou Luogang Aoyuan Plaza (廣州蘿崗奧園廣場) and Zhongshan Aegean (中山愛琴海). Owners can enjoy high-quality old-age care services at their doorsteps, including TCM healthcare, health management, recuperation therapy, senior university, adapt to aging and the use of auxiliary equipment for the senior.

The integration of the three major business sectors is the focus of 2H

One of the company's key tasks in the 2H20 is the integration of the three sectors, and how to make it more synergistic. At present, it has begun to experiment in property and commercial management, property and general health, and it has also achieved initial results. In addition, it will focus on cooperation with real estate, and obtain support by providing services to real estate. Value-added services are also the company's main development direction in the second half of the year.

Investment Thesis

The company's performance in the first half of the year was in line with our expectations. In the past six months, the company's two acquisitions have effectively expanded the company's residential management services. After Easy Life's consolidation, the company's revenue will rise. However, considering Easy Life's profitability is far lower than Aoyuan Healthy. It is expected that the company's GPM will decline in 2020, and the company will focus on post-investment management. In the future, gross profit and gross profit margin will further increase.

Due to changes in the company's financial strategy, we adjusted our previous forecasts. We expect the company's FY20/FY21 EPS to be RMB 33.13 cent/RMB 43.94 cent, giving a target price of HK$9.60 corresponding to 26.1x/19.7x P/E ratios for FY20E and FY21E, Upgrade the rating to buy.

(Current price as of August 28)

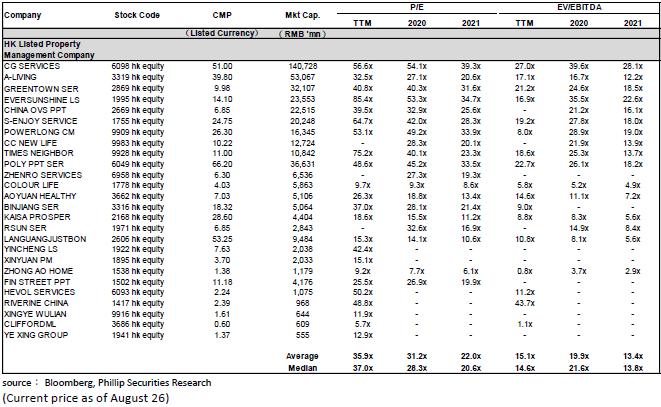

Peer Comparison

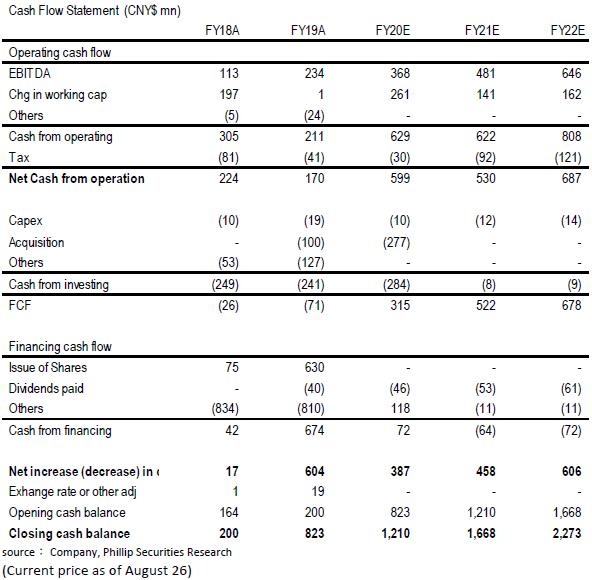

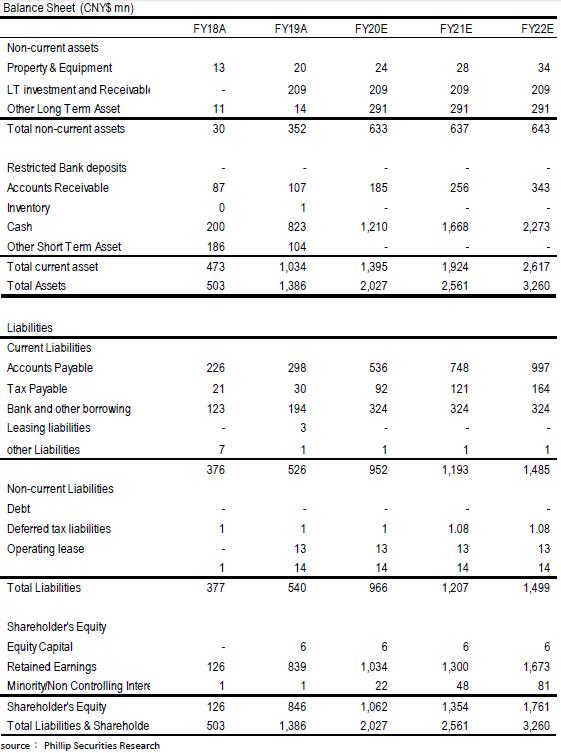

Financials

Click Here for PDF format...