Investment Summary

Affected by the Epidemic, the Net Profit in H1 was -36% yoy

Fuyao Glass released its 2020 semi-annual report: during the reporting period, the Company recorded revenue of RMB8.12 billion, down 21.1% yoy; net profit attributable to the parent company of RMB960 million, down 36% yoy; net profit attributable to the parent company excluding non-recurring items of RMB790 million, down 40.9% yoy; a revenue of RMB3.95 billion in Q2 only, down 26.2% yoy; net profit attributable to the parent company of RMB500 million, down 44% yoy; net profit attributable to the parent company excluding non-recurring items of RMB410 million, down 50% yoy.

The main reasons for the negative results: (1) German FYSAM auto decorative project was in the integration period and suffered a loss of EUR26.17 million due to the impact of the epidemic; (2) Fuyao Glass American Factory suffered a loss of USD17.378 million due to the epidemic. Some of the headwinds were offset by (3) exchange gains of RMB128 million (RMB31 million in the same period of last year).

Excluding the above factors, the total profit decreased by 16.19% yoy.

Capacity Utilization Declined, Depreciation and Amortization Increased, Dragging down the Gross Margin by 1.8 ppts

In H1, the Company's gross margin was 35.74%, down 1.79 ppts yoy, of which the gross margin of the automotive glass segment was 32.58%, down 1.9% yoy. Its main reasons include: Due to the impact of the epidemic, the production and sales volume of the automobile industry decreased yoy, the demand for orders from downstream customers decreased, resulting in insufficient capacity utilization. Meanwhile, the depreciation and amortization increased in proportion to the revenue, affecting the gross margin by 2.54 ppts. The gross margin of float glass segment was 36.3%, up 1.7 ppts yoy, mainly due to the price rise in the second quarter of float glass industry.

In terms of expenses, the ratio of sales expenses increased by 0.8 ppts to 7.5% yoy due to the decline in revenue; due to the increase in depreciation and amortization and the rigidity of R&D expenses, the administration expense ratio increased by 2.7 ppts to 16.3% yoy.

However, we also noted that the Company's Q2 gross margin increased by 1 ppts and 2.7 ppts, respectively yoy and qoq. The main driving factor is the Company's domestic business capacity utilization began to improve, and the proportion of high value-added products increased significantly.

It is Expected to Resume Growth in H2 with a Clear Product Upgrade Path

In H2, the overseas market will gradually resume production in the third quarter. The Q3 resumption rate of Fuyao American Factory has reached 60%, and is expected to contribute to profit and help the Company resume growth in H2. Germany FYSAM is expected to start turning a profit next year as a year and a half of integration is gradually completed. The Company's earnings are flexible for next year.

At present, the automobile market has entered a new stage of development of diversification and upgrading. The automobile is developing towards the trend of "electric, network, intelligent and sharing". More and more new technologies are also integrated into automobile glass, and the added value of products is constantly improving. In the meantime, it also provides new opportunities for the development of automobile glass industry.

In H1, Fuyao Glass continued to promote the value-added of automobile glass products and accelerate R&D innovation. The Company's heat insulation, sound insulation, head-up display, solar energy, hemming modularization and other high value-added products shipments continued to increase, accounting for an increase of 2.46 ppts, which highlighted the Company's leading role in the industry. In H1, the Company and BOE carried out strategic cooperation in the fields of automobile intelligent dimming glass and window display, and signed a strategic cooperation agreement with Beijing BDStar Navigation, to jointly commit to the integration of high-precision positioning and communication multi-mode smart antenna and automobile glass, and to help improve the innovation and competitiveness of the Company's products.

Investment Thesis

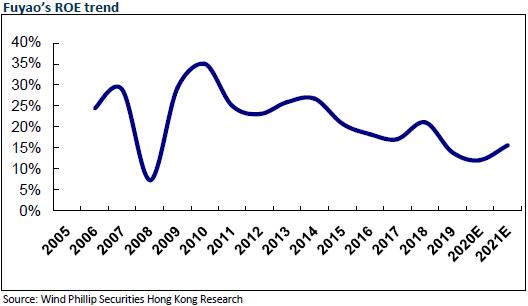

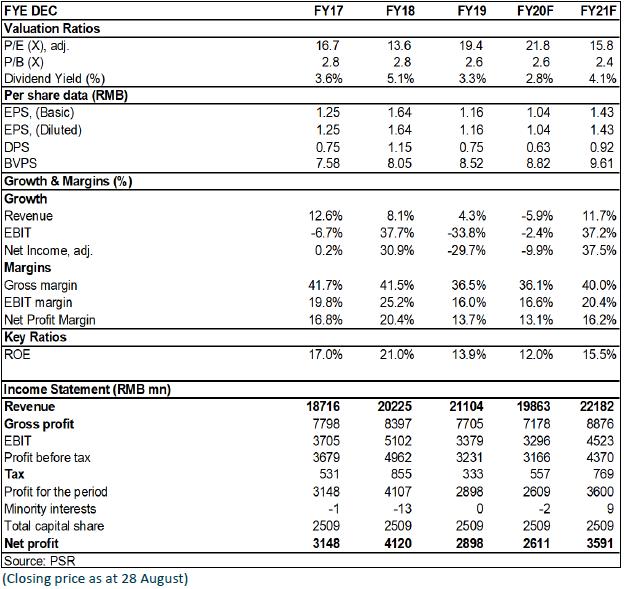

Overall, considering the steady leading position, continuous optimization of the product structure and a high dividend rate provide a greater margin of safety for the Company. We give the "Accumulate" rating,with target price to be HK$29, equivalent to 25/18x P/E for 2020/2021E. (Closing price as at 28 August)

Risks

Demand for automobiles keeps sluggish; cost of raw materials increases; RMB appreciates

Catalyst

Success market development of overseas automobile market; rebound of domestic demand for automobile; depreciation of RMB

Financials

Click Here for PDF format...