Investment Summary

2020 interim result overview

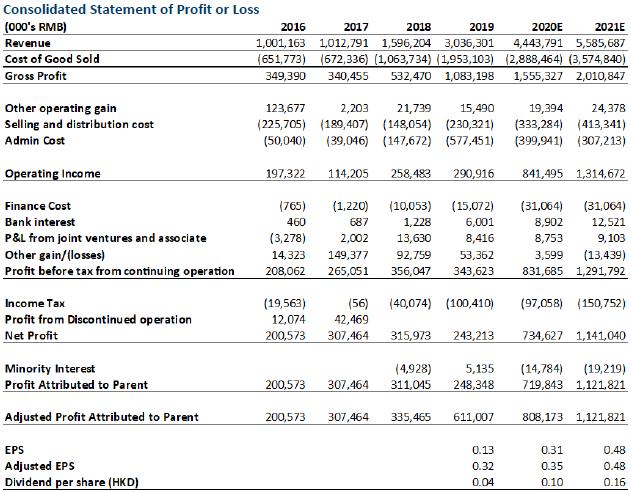

The 1H20 revenue of CMGE was RMB 1.714 billion (+12.1% yoy). The 1H20 GP was RMB 531 million (+0.5% yoy). The NP/Adjusted NP were RMB 288/341 million respectively, (+10.5% yoy /+27.6% yoy). In terms of the company's different revenue stream, the revenue of game publishing/game development/IP licensing were RMB 1,489/221/4 million respectively (+13.9% yoy/+1.1% yoy/+15.0% yoy). The interim result is in line with our prediction, that the company's 1H20 growth would be slow since all the big games that are expected to be published this year are all going to be published in 2H20. We expect there will be a huge earnings boost in 2H20 and 2021.

The company will publish a variety of popular games with huge anticipation in 2H20

The company has only published a few new games in 1H20 such as Xuan Yuan Sword – the Origin (軒轅劍–劍之源), Reborn! (家庭教師) and Demon Rebirth (魔域覺醒). Xuan Yuan Sword – the Origin (軒轅劍–劍之源) and Reborn! (家庭教師) have both achieved impressive results in 1H20. They both ranked second on the free list of Apple Store in the first month of their launch. At the same time, Demon Rebirth (魔域覺醒) also ranked first in terms of new game recommendation on the wan.360.cn game platform.

We truly believe that the upcoming year will be one of the most important year to the company since its establishment. Many highly anticipated games will be launched in 2H20 and 2021. First of all, the company will publish a number of new games, including The New Legend Of The Condor Heroes: Iron Blood and Loyal Heart (新射雕群俠傳之鐵血丹心), Life and Death Sniper: Zombie Frontier (生死狙擊之殭屍前線), A Record of a Mortal's Journey to Immortality (凡人修仙傳), Hua Jiang Hu: Bei Mo Ting (畫江湖之杯莫停), Soul Land: God of Battle Arise (斗羅大陸: 鬥神再臨), Legend of Immortal: Sharing the Sky (星辰變:共攬蒼穹). The New Legend Of The Condor Heroes: Iron Blood and Loyal Heart (新射雕群俠傳之鐵血丹心) was published on Apple IOS platform on the 20th of August. By leveraging on the excellent quality of the game and excellent advertising strategy (including advertising in multiple channels and celebrities` collaborations), the game has been ranked 1st on the App Store free list for 6 days consecutively after it was launched, and has been consistently ranked Top 10 on the bestselling list. According to the company's management, the operating indicators (user retention rate, DAUs etc.) of the game have all beaten their expectation prior launching. Comparing to previous similar games, this game is the first to obtained the complete authorization of the trilogy of The Legend Of The Condor Heroes and has also added new game modes. This game will give the IP fans a refreshing gaming experience. We truly believe that this game will be one of the hottest games this year.

On the other hand, the company is expected to published a variety of new self-developed games in 2H20, including Legend of Dragon City (龍城傳奇), Code: Dragon (代號:聖龍) as well as two Legend of Sword and Fairy (仙劍奇俠傳) games. Legend of Dragon City (龍城傳奇) and Code: Dragon (代號:聖龍) are both “Legend type games” and the company has absolute advantages in the “Legend type games” markets. The company's subsidiary Wenmai Hudong possess strong “legend games” R&D capabilities and the ability to deeply explore the differences with peer games. Legend of Dragon City (龍城傳奇) was developed based on The World of Legend – Thunder Empire (傳奇世界之雷霆霸業) by the same development team of The World of Legend – Thunder Empire (傳奇世界之雷霆霸業). The World of Legend – Thunder Empire (傳奇世界之雷霆霸業) was published in 2018 and has contributed the most revenue to the company among all other games in 2019. The team has enhanced the art performance of the game and has added new game mode to the game with the aim to improve user experience. Code: Dragon (代號:聖龍) is a next generation web game developed based on War Song – the Creation (熱血戰歌之創世) and by the same developed team of War Song – the Creation (熱血戰歌之創世). War Song – the Creation (熱血戰歌之創世) was one of the most popular web game in 2019 with over 2 million MAUs in 2019. We believe Legend of Dragon City (龍城傳奇) and Code: Dragon (代號:聖龍) will be able to continue the legacy and impressive performance of World of Legend – Thunder Empire (傳奇世界之雷霆霸業) and War Song – the Creation (熱血戰歌之創世).

In addition, the company will partner up with the internet giants (Tencent and ByteDance) and publish a total of 4 games, including One Piece: The Voyage (航海王熱血航線), The King of Fighters: All Stars (全明星激鬥), Dynasty Warriors: Hegemony (真三國無雙霸) and Monster List: Past and Present Lives (妖怪名單之前世今生). The ARPG market around the globe is huge but there isn`t a single ARPG game or game developer taking over the market. Dynasty Warriors: Hegemony (真三國無雙霸) is an ARPG game with huge market anticipation, we expect it will have a great performance after launching. The game is exclusively distributed by Tencent in China and the company will be responsible for the global distribution. In conclusion, we believe the collaboration with internet giants can on one hand fully demonstrate the high recognition of the company's capabilities from the industry leaders, and on the other hand help the company's games to reach for a more diverse user group.

The company's active industry chain investment and cooperation will continue to provide the company with high-quality games

The company has invested in three mobile game developers in 1H20, including Love games (樂府互娛), EZfun Technology (易帆互動) and Huanyu Jiuzhou (寰宇九州). Love games (樂府互娛) is one of the top Chinese game developer in card game categories. The founder of Love games, Cheng Liangqi (程良奇), is the chief producer of some well-regarded card game series such as the Youth Three Kingdoms (少年三國志) and Junior Monkey King (少年西遊記). In addition, EZfun Technology (易帆互動) has intensive experience in ARPG game development. It is also the game developer of Dynasty Warriors: Hegemony (真三國無雙霸), which is expected to be published by Tencent and CMGE in 2H20. Further, Huanyu Jiuzhou (寰宇九州) is specialized in tower defense and simulation games development. It is also the game developer of Monster List: Past and Present Lives (妖怪名單之前世今生), which is also expected to be published by Tencent and CMGE in 2H20. CMGE has entered into a long term cooperation with the above game developers. CMGE will continue to combine its advantages in IP resources with the strong R&D capabilities of its invested game developers. We strongly believe this will help the company to build its competitive advantages in different game types (card type, ARPG, tower defense).

The oversea markets are expected to be the new growth engine for the company in the future.

It is the general trend for Chinese game companies to expand business overseas. Although the company has begun to deploy its overseas business many years ago, but compared with its industry peers, the company's current revenue from overseas businesses is still very low. The company's revenue from overseas businesses only accounted for 0.43% of its total revenue in 2019. The management of the company stated that the company currently has a large reserve and supply of high-quality game, hence, they will focus on their overseas business in 2H20, especially in regions like Hong Kong, Macao, Taiwan, Japan, South Korea, Europe and the US. It is expected that the company's revenue from oversea markets will start growing rapidly next year and overseas businesses will be an indispensable business segments for the company in the future. The company has launched its self-developed game, Reborn! (家庭教師), in Hong Kong, Taiwan and Macau region on the 18th of August and ranked 1st on the Appstore free list on the first day of its launch. The company is expected to publish a multiple of games overseas in 2H20 and 2021, including The New Legend Of The Condor Heroes: Iron Blood and Loyal Heart (新射雕群俠傳之鐵血丹心) and Dynasty Warriors: Hegemony (真三國無雙霸). The regions where different games are promoted and distributed will be determined according to the advantages of the game's IP. Considering that games such as The New Legend Of The Condor Heroes: Iron Blood and Loyal Heart (新射雕群俠傳之鐵血丹心) and Dynasty Warriors: Hegemony (真三國無雙霸) are all Asian IP games, the company expects that such games will only conduct intense localized promotion in Asia region (including Japan, South Korea, Hong Kong, Macau, Taiwan, and Southeast Asia), in order to achieve the highest ROI.

Valuation

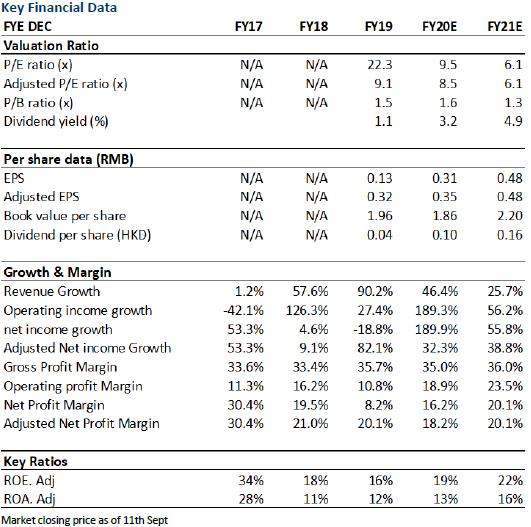

Overall, the company's interim result meets our expectation, but the GPM for the interim was slightly lower than our expectation. The company's GPM in 1H20 was 31%. With the launch of high margin games in 2H20, we expect the 2020 GPM will increase to 35%, but still lower than our previous forecast. We slightly lower the company's adjusted EPS for 2020 and 2021 to RMB 0.35/RMB 0.48. We raise the company's 2020 target P/E ratio to 12.2x (the average P/E of mid-tier companies in the industry). We raise our target price to HKD 4.70, which corresponds to a 2020/2021 adjusted P/E of 12.2x/8.8x. We maintain “Buy” rating. (Market closing price as of 11th Sept) (exchange rate: RMB 0.9/HKD)

Risks

The risks to our target price are 1) failure in licensing IPs and games 2) failure in developing games in-house 3) failure to obtain or maintain all applicable permits and approvals 4) loss or deterioration of our relationship with game developers and publishing channel 5) The revenue generated from games are below expected.

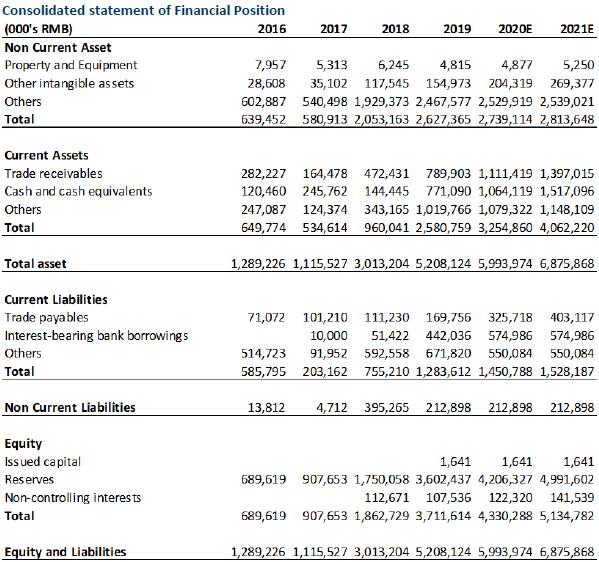

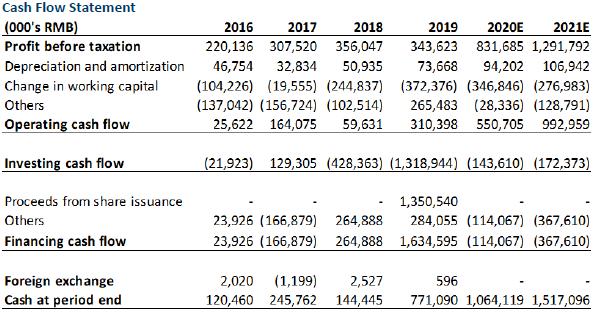

Financial Statements

Click Here for PDF format...