Investment Summary

Actual Earnings in Q3 Jumped nearly 40% yoy, Excluding Depreciation of Ruble

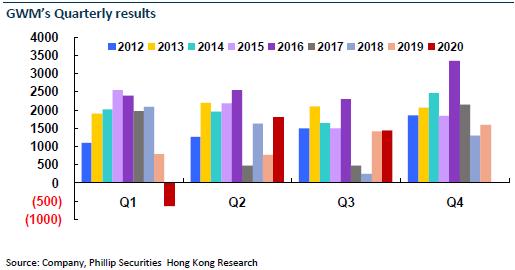

Great Wall Motors (GWM) issued the 2020 Third Quarterly Report. Its revenue amounted to RMB26,214 million, up by 23.64% yoy. The net profit attributable to the parent company reached RMB1,441 million, increasing by 2.93% yoy. Its exchange loss of RMB510 million was primarily attributable to the depreciation of the ruble. GWM's actual net profit would have been RMB1.95 billion with strong yoy growth of 39%, if the adverse factor was excluded. Additionally, Q3 sales expenses rose by RMB570 million QoQ, due to the delay of the Beijing Auto Expro 2020, which was one of the reasons for the fluctuations of result.

Sales Volume Remained High, Demands for Pickups and NEVs Surged

The Company's total sales in Q3 were 286,000 units, which climbed by 24% yoy, higher than the industry average, including 183,000 units of HAVAL with a yoy increase of 9%, 23,600 units of WEY (+3% yoy), 14,500 units of ORA (+180% yoy), and 64,500 units of GWM PICKUP (+93% yoy).

GWM's pickups met with no resistance regarding sales after launch, as they are leading the trend of mid-to-high end pickups as passenger vehicles. The monthly sales exceeded 10,000 units. Accordingly, the sales of pickup models surpassed 20,000 units for five consecutive months, dramatically up by 63% yoy. Currently, its domestic pickup market share reaches up to 50%.

Thanks to the launch of new version, 5,141 units of ORA Black Cat were sold in September, ranked third among models at the same level. Moreover, most of the buyers were individuals, which implied the comprehensive strength of the products.

The proportion of sales volume of HAVEL H6, the knockout HAVAL model, fell from 47% in 2017 to approximately 22%, indicating a more balanced distribution of sales volume of all models. 3-generation H6 pulled away the old model. The existing orders were more than 20,000 units. 11,000 units were sold in September. It is expected that the sales volume will jump to 20,000 units per month by the end of the year.

Business Indicators Continued to improve, Sales Structure Constantly Optimized

The gross margin increased by 1.5 ppts QoQ and 0.5% yoy to 19%, because of the constantly optimized sales structure and further strengthened business indicators. The actual ASP in Q3 grew QoQ, less the adverse influence of lags by the financial statistical standard. A net outflow occurred regarding the operational cash flow, as affected by the epidemic in Q1. It is estimated that the figure will turn positive in Q4. 3-generation H6 and BIGDOG are accumulating strengths after launch; WEY TANK 300 and ORA Good Cat will be introduced in Q4. Their sales volume contributions are promising in the future.

More new models (approximately ten models) equipped with new technologies and new power are also planned to be launched in 2021, including fuel vehicles, hybrid power vehicles and EV models. The year 2021 will be the start year of new products-cycle for GWM. With the opening of the new model cycle, we expect that new platforms and new models will facilitate the Company to further enhance its competitiveness. With the constant increase of platform-based products, the Company will shorten the model development cycle and weaken the generalization of parts in the future to increase the product competitiveness. As a result, its profitability is expected to continue to increase.

In terms of car intelligence, the Company has achieved mass production of Level 2 models since 2019. At present, its 45% of the models on sale have achieved L2 level autopilot and it is planned to launch L3 level models in 2021 and reach L4 level autopilot technology in 2022. We believe that GWM's investment and accumulation in automotive intelligence will build the company's long-term competitive strength.

Investment Thesis

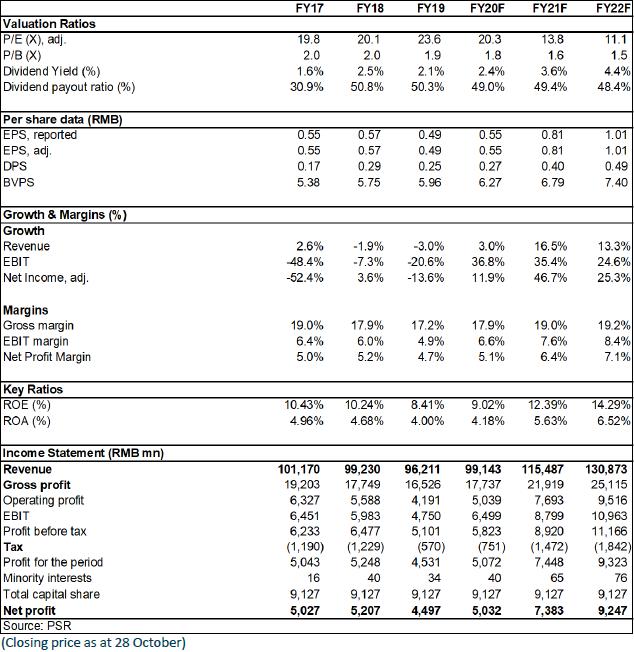

In terms of valuation, we adjust our target price to HK$15.2, equivalent to 24/16/13x P/E and 2.1/1.9/1.8x P/B ratio in 2020/2021/2022. We reaffirm the rating of “Accumulate”. (Closing price as at 28 October)

Risk

New vehicle sales fall short of expectations

The SUV market dramatically worsens

The progress of new energy vehicle/Pickup is poorer than expectations

Financials

Click Here for PDF format...