Investment Summary

Archosaur Games was included in the stock connect on 7th of December

The Hang Seng Index Co., Ltd. announced on November 13, 2020 that Archosaur Games will be added to the Hang Seng Technology Index on December 7. On the same day, the Hong Kong Stock Exchange announced that the company will be included in the Hang Seng Stock Connect Hong Kong Index, Hang Seng Stock Connect Hong Kong MidCap & SmallCap Index, and Hang Seng SCHK Mainland China Companies Index. On December 7, the company was officially included in the stock connect, we believe this may have a boost to the liquidity of the company's stocks. Further, this is likely to introduce mainland investors to contribute the company's revaluation as well as increasing the market's awareness of the company's investment thesis. We believe the inclusion in stock connect will benefit the trend of the company's stock price in future.

Solid performance of Under the Firmament (鴻圖之下)

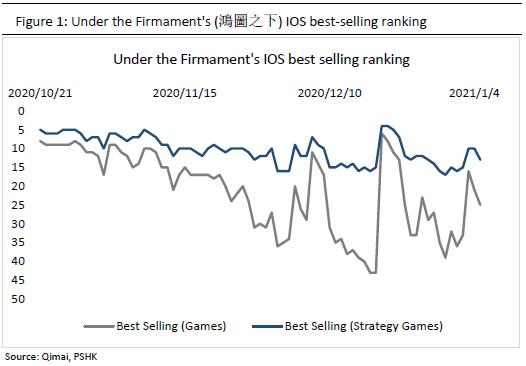

Under the Firmament (鴻圖之下) was launched on the 21th of October. Under the Firmament (鴻圖之下) is the first mobile SLG game powered by the Unreal Engine 4. Unreal Engine 4 technology has broken through the gorgeous visual effects that many SLG games could not display before and has created a real and magnificent Three Kingdoms War setting for users. At the beginning of the launch, the game has maintained the top 10 in the IOS strategy game best-selling rankings, and currently maintains stably in the top 40 and top 15 on the IOS game best-selling rankings and the IOS strategy games best-selling rankings, respectively. In addition, according to gamma data, the game's first month gross billing exceeded RMB 300 million, and becomes the company's sixth game with gross billing over the RMB 100 million mark in the first month of launching. Currently, the game's TapTap score is 7.4, with over 360k followers on TapTap platform. The overall performance of Under the Firmament (鴻圖之下) is in line with our previous expectation. As the company's 1st ever self-developed SLG game, the solid performance it has achieved can fully demonstrate the company's strong R&D capabilities as well as the outstanding distribution strategy implemented by Tencent, the sole distributor of the game in China region. Even though SLG games` gross billing tend to lack the explosion in the early stage, but SLG games tend to have longer life cycles and stable gross-billings in long term, coupled up with the company's new upgraded version of the game launched in December, we expect Under the Firmament (鴻圖之下) can still contribute significant gross-billings for the company in 2021.

The company's rich and diverse game reserves are expected to promote high growth in the coming years

Up to now, the company has a total of 7 games in reserve, including 4 MMORPGs, 2 SLGs and a female-oriented game. In terms of the scheduled timeline, three games will be launched in 2021, including The New World (夢想新大陸), Noah's Heart (諾亞之心) and Sango Heros (三國群英傳). The New World (夢想新大陸) was initially scheduled to be launched in 20Q4, however the timeline has been delayed as a result of the later-than-expected game approval (版號) received. Now the launching of the game has been delayed to 21Q1. The New World (夢想新大陸) is the company's first turn-based game based on Unreal Engine 4. It has achieved fine details in character modeling, map scenes and other fine arts, bringing players a refreshing gaming experience. According to market news, due to the characteristics of Unreal Engine 4, this game is very likely to be one of the most expensive turn-based MMORPG games currently known. The game's File-deleting public beta has begun on 19th of November. Up to now, the game has a score of 8.8 on the TapTap platform, and the number of reservations exceeds 80,000. Taking into account the company's rich game reserves and the unique graphic characteristics of the reserved games, the company's future growth is looking promising.

Valuation and investment thesis

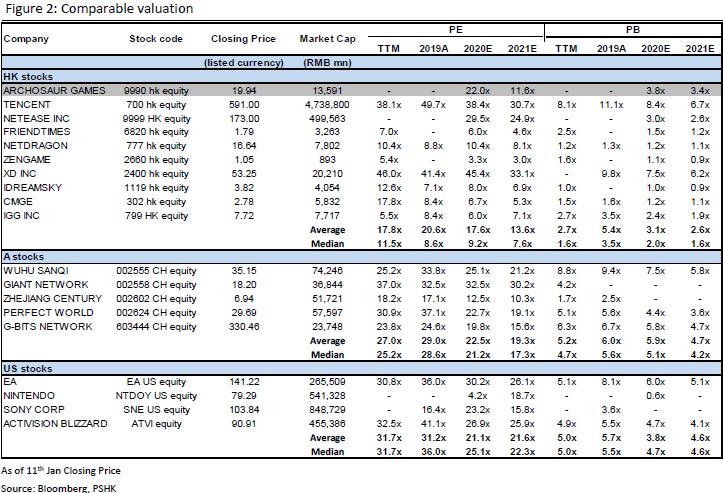

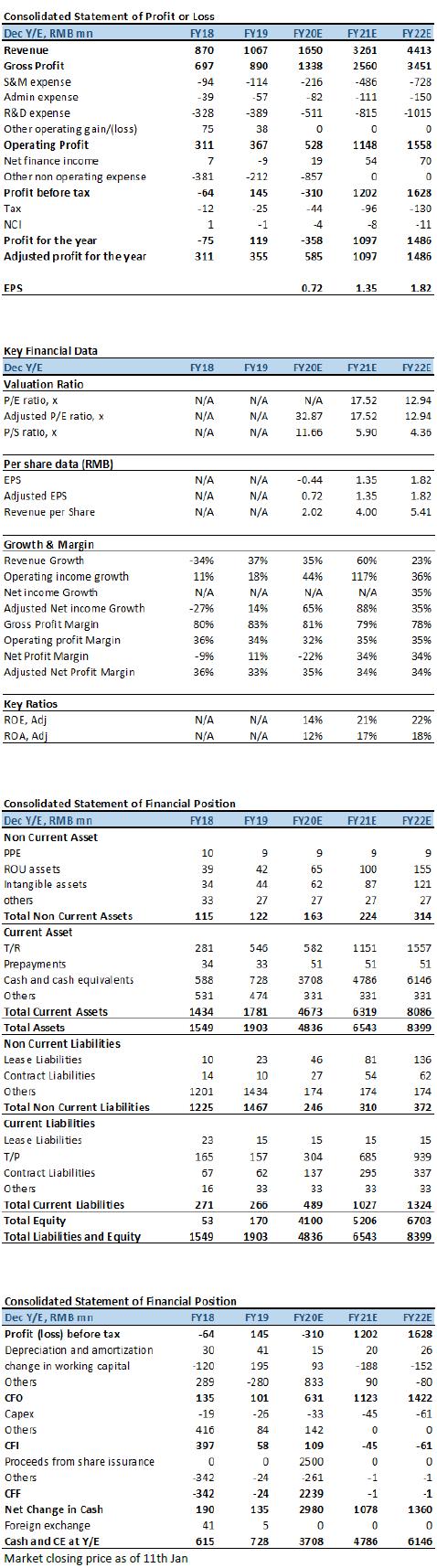

We continue to be optimistic about the company's strong R&D capabilities and its long-term and in-depth partnership with Tencent. However, due to the delayed launch of Under the Firmament (鴻圖之下) and The New World (夢想新大陸), we have lowered the company's 2020 forecast revenue to RMB 1.65 billion, adjusted NP to RMB 585 million and adjusted EPS to RMB 0.72, while maintaining the previous forecast on 2021 and 2022. Taking into account the downgrade in valuation of the sector (especially the mid-tier game companies), we have lowered the company's 2021 targeted PE to 20x, TP at HKD 30.60 (-8.9%), with 2020/2021/2022 adjusted PE at 37.5x/20.0x/14.8x. We maintain “BUY” rating. (Market closing price as of 11th Jan) (exchange rate: RMB 0.88/HKD)

Risk

1) The tightening on Game regulations 2) The Games underperform comparing to expectation 3) Games launching are delayed due to unexpected reasons

�Financial Statements

Click Here for PDF format...