Investment Summary

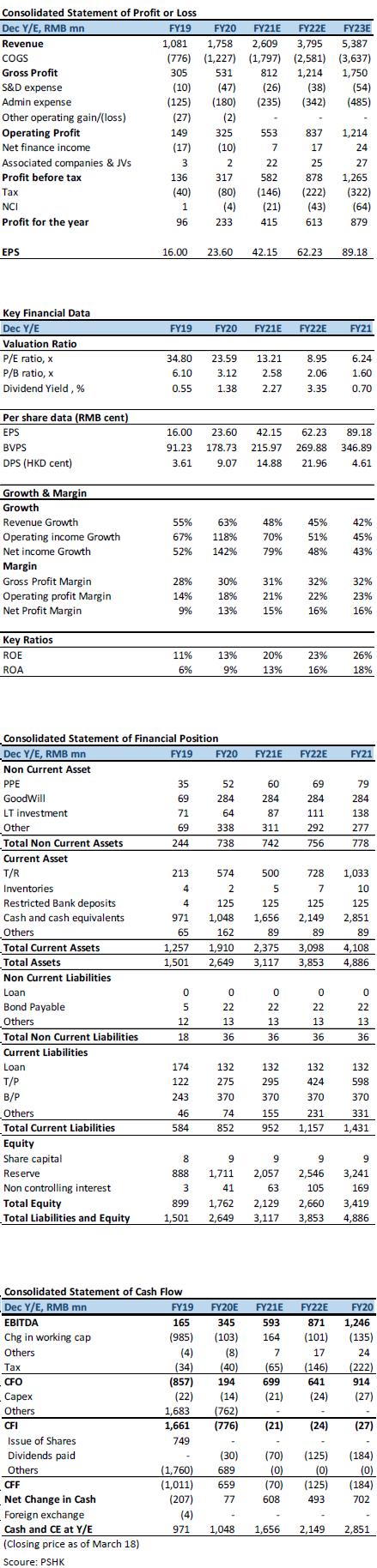

On March 10, 2021, the company announced its annual results for the year ended December 31, 2020. The company's 2020 revenue was RMB 1.76 billion, an increase of 63% year-on-year, which was lower than our previous expectations. Revenue from Property management services/VAS to non-property owners/Community VAS/Professional services increased year-on-year by 48.9%/53.3%/135.2%/187.3% respectively, and core net profit attributable to owners of the parent was RMB 233 million, an increase of 93.7% year-on-year , beat our previous expectations, mainly due to the company's cost control and property management services GPM increase during the period, the core net profit attributable to owners of the parent margin increased from 11.1% in 19 years to 13.2% in 20 years, an increase of 2.1 ppts.

Regarding the revenue structure, the company's revenue from Property management services/VAS to non-property owners/Community VAS/Professional services was 1.01 billion/420 million/190 million/140 million, respectively, accounting for 57.4%/24.0% /10.6% /8.0% of the total revenue, among which Community VAS and Professional services accounted for a year-on-year increase of 3.3/3.5 ppts respectively. In terms of GPM, the company's overall GPM increased by 2.0ppts from 28.2% in 2019 to 30.2% in 20 years, and Property management services/VAS to non-property owners/Community VAS/Professional services were 28.2%/29.8%/51.0%/18.2% respectively. Among them, the GPM of Property management services and VAS to non-property owners has increased, mainly due to the increase in the average unit price of the company's residential management projects during the year, the use of technology and automation systems to replace labor and starting housing agency services. The company's cost management during the year was proper. With the expansion of the company's management scale, it became more effective in terms of cost and expenditure. Coupled with the company's digital transformation during the year, the administrative expense ratio dropped from 11.6% in 2019 to 10.2% in 20 years. The core net profit margin for the year was 13.2%.

Projects under management included different business format

In terms of operations, for the year ended December 31, 2020, the company had a total of 527 projects under management, with approximately 111.6 million square meters of contracted GFA (of which approximately 29.9 million square meters were urban public service projects), and contracted GFA increased by 92.4% from the year ended December 31, 2019. As of December 31, 2020, the company's property management services under management have covered 53 cities, and the GFA under management in property management service is approximately 68.8 million square meters. A total of 67 contracted property management projects have not yet been delivered, and the reserved GFA is approximately 12.9 million square meters. In terms of business format, the company's non-residential area ratio was 67.6%, an increase of 4.9 ppts year-on-year. The collection rate of management fees rose from 90% in 2019 to 93% in 2020.

Adhere to the 4321 core strategy and increase the development of community VAS

At the conference, the company put forward the core strategy of ", while taking into account horizontal and vertical development, and intensively cultivated the 4 core urban agglomerations (Greater Bay Area, urban agglomerations in Yangtze River Delta, Chengdu-Chongqing region and Central China), deploy 3 core business formats (residential, industrial and government public construction), take property management services and value-added services as the 2 core growth points, and establish 1 full life cycle "technology + service" core platform. The company also put forward clear goals for scale expansion and growth quality, 1) 2020-2023 attributable to core net profit growth CAGR of more than 50%; 2) 2021/2022 new third-party contracted area target is 38 mn/46mn square meters, 3) The proportion of external expansion will also be increased. Among the newly added third-party contract area, the proportion of area from investment and expansion of target projects in 2021/2022 will be 50%/60%, further reducing the reliance on mergers and acquisitions. 4) The proportion of Community VAS in revenue has increased to more than 25% in 2024 years.

Valuation model update

The company's FY20 results were lower than our expectations in terms of revenue, mainly due to lower revenue from the company's Property management services and VAS to non-property owners than we expected, but revenue from Community VAS and Professional services increased more than we expected. The overall revenue is slightly lower than our expectations (compared to expectations: -3%). In terms of profitability, the company has introduced digital management in its property management business to effectively reduce service costs and increase GPM. The increase is higher than we expected. It is expected that the company's property management services GPM will further improve in the next two years and become stable from 2022. The overall GPM is 2 ppts higher than our expectation. On the whole, the company's actual net profit for 2020 is CNY 233 million, which is higher than our expectation (expected: CNY 227 million, +2.64%).

According to the previous mentioned, we have made some adjustments to the valuation model, reducing the company's revenue growth from property management services and non-owner value-added services, and improving the gross profit forecast of the property management segment in 2021 and 2022. Lower the company's profit forecasts for 2021 and 2022 to 417 million and 612 million yuan (previously CNY 426 million and 621 million).

Valuation and investment advice

In 2020, the company made four acquisitions, intervened in the development of other regions and business types, and entered subdivisions such as power supply systems and industrial logistics facilities. The company still has sufficient cash for mergers and acquisitions to provide potential growth space in the future. During the year, the company also introduced digital management to further improve cost control and strengthen profitability. At the conference, the management also gave specific development goals to reduce reliance on mergers and acquisitions in the future, strengthen its own outward expansion capabilities, and increase efforts to develop community value-added services. We expect the company's EPS in 2021 and 2022 to be 42.15 cent and 62.23 cent. Taking into account the current increase in the choices of property management stocks on the Hong Kong stock market and the rise in market interest rates, we lower our target price to HKD 10.91 (previously: HKD 14.91), corresponds to 22.00x/14.90x expected P/E ratio in 2021 and 2022. Maintain the buy rating.

(Closing price as of March 18)

risk

1) Post-investment management after M&A is not as ideal

2) Interest rates continue to rise

Financial

Click Here for PDF format...