Investment Summary

The company has made adjustments on its revenue breakdown structure and classified the net method part of the targeted marketing business as merchant solution within the digital commerce segment

In the 2020 annual report, the company has made adjustment on the revenue breakdown structure. The main segments are now renamed as digital commerce segment and digital media segment (previously named as the SaaS business and the targeted marketing business). More specifically, the original SaaS business has now been classified as the subscription solution sub-segment within the digital commerce segment, while the targeted marketing part with revenue recognized by net method is now classified as the merchant solution sub-segment within the digital commerce segment. On the other hand, the targeted marketing part with revenue recognized by gross method is now classified as the digital media segment. After the adjustment, a major part of the targeted marketing business is expressed as the value-adding services of the SaaS business, so as to better show the synergy between these two major businesses.

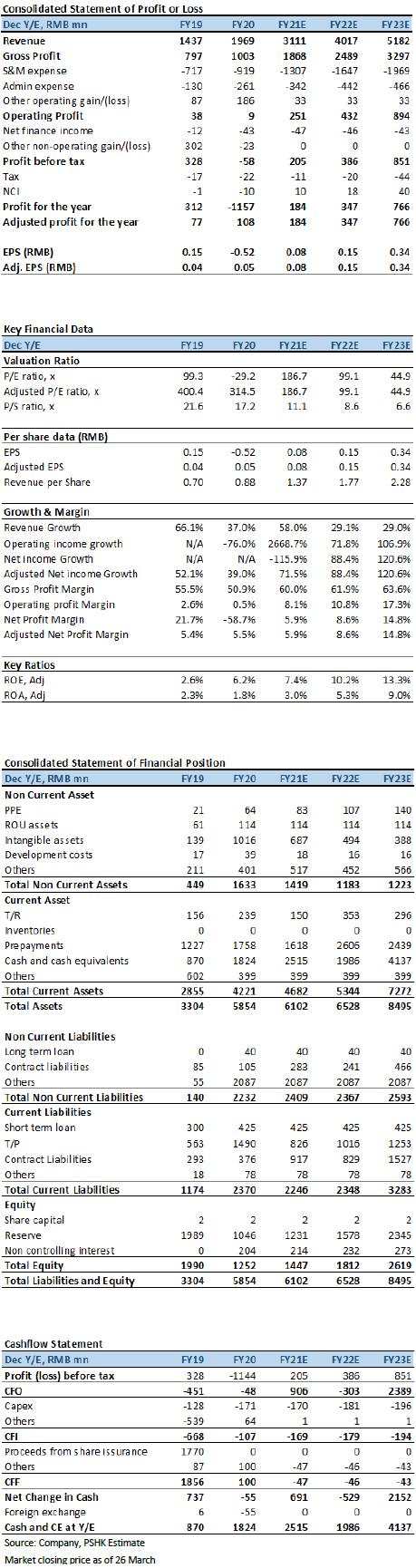

The 2020 adjusted revenue of subscription solution and the 2020 gross revenue of targeted marketing business beat our expectation, but the GPM is slightly below our previous forecast

The company's 2020 revenue was RMB 1.97 billion (+37.0% yoy), of which the revenue of the subscription solution was RMB 622 million (+22.8% yoy) and the adjusted revenue of the subscription solution (excluding the impact of the SaaS sabotage event) was RMB 718 million. The adjusted revenue beat our previous expectation. On the other hand, the 2020 revenue of the targeted marketing business (merchant solution + digital media) was RMB 1.35 billion (+44.8% yoy), which was slightly lower than our previous forecast. However, we believe that compared with the revenue, the gross revenue can more reflect the growth of the targeted marketing business. The 2020 gross revenue of targeted marketing business was RMB 10.68 billion (+102.2% yoy), which beat our previous forecast.

In terms of the GPM, the 2020 adjusted GPM/ GPM of subscription solutions was 74.5%/70.6% (-6.0ppts yoy / -9.9ppts yoy), both of which were lower than our previous expectation. The divergence between the actual GPM and our forecasted one was mainly due to the fact that the higher-than expected R&D investment caused higher amortization of intangible assets, which was recorded in the COGS. On the other hand, the 2020 GPM (comparing to the gross revenue) of the targeted marketing was 5.3% (-2.1ppts yoy), which is also lower than our previous expectation, since the lower rebate from the KAs (key accounts) customer has a greater downward impact to the GPM (comparing to the gross revenue) than we previously thought.

In terms of the operating expenses, the company's 2020 S&M expenses / admin expenses was RMB 919 million/RMB 261 million (+28.2% yoy / +100.7% yoy), respectively. The 2020 net loss attributable to parent was RMB 1.16 billion (RMB 311 million in 2019), and the 2020 adjusted net profit was RMB 108 million (+39.0% yoy).

The growth momentum of the subscription solution was strong while the moving-up market strategy of the company is gradually paying off

The 2020 adjusted revenue of subscription solution was RMB 718 million (+41.6% yoy). As of the end of 2020, the number of paying merchants was 98,002 (+23.2% yoy) and the ARPU was RMB 7,326 (+15.0% yoy). Both of which figures beat our expectation. On the other hand, the customer churn rate for subscription solution in 2020 was 26.1% (+3.9ppts yoy). The yoy increase in churn rate was mainly due to 1) The 2020 pandemic was a huge blow to the SME merchants, which directly affect their paying willingness and ability 2) the SaaS sabotage event in early 2020 directly led to loss in merchants. In terms of the breakdown in subscription solution, the smart retail sub-segment showed the strongest growth momentum. The 2020 revenue of the smart retail sub-segment was RMB 145 million (+224.5% yoy) and accounted for 20.2% (+11.4ppts yoy) of the total revenue from subscription solution. As of the end of 2020, the number of smart retail merchants was 3,682 (+234% yoy) and the number of brand merchants was 618 (+185% yoy). The brand merchants ACV was RMB 282 thousand (+31.2% yoy). On the other hand, the revenue of smart dining in 2020 was RMB 44.82 million (+13.0% yoy). The growth of smart dining was slower than that of smart retail as the 2020 pandemic had a greater impact to the food and beverage sector in China and the recovery momentum of it was also slower. As of the end of 2020, the number of smart dining merchant was 6,996 (+52.0% yoy) and the ACV was RMB 19 thousand (+46.2 % yoy).

The company will continue to implement its 3 core strategies, namely the moving-up market strategy, globalization strategy and the ecosystem build-up strategy

1) Moving up–market strategy - In the past, the company had a leading position in the fashion industry and household industry. It will continue to explore the KAs in these industries to further consolidate its leading position in these industries. On the other hand, in view of the company's acquisition of Heading Information in 2020, the company will explore vertical industries such as shopping malls and supermarket convenience through continuous integration with Heading Information to further explore the KAs in these sectors. In addition, the KAs in vertical industries like maternal and child chain, food and beverage, medical and health care are also the future acquisition target of the company. The company's management expects that in the smart retail sub-segment, the revenue proportion of the KAs will reach 30% by the end of 2021 and 50% by the end of 2025.

2) Ecosystem build-up strategy - The company will continue to expand its traffic ecosystem, developer ecosystem and investment ecosystem in the future. In terms of the traffic ecosystem, the company's products will be connected to traffic platforms other than the ones within Tencent's ecosystem to assist merchants in omni-channel smart operation. At present, the company's products have already been connected to non-Tencent ecosystem such as Tiktok, Kuaishou, Baidu, and Alipay, as well as many offline long-tail traffic. In the future, it is expected that the company's products will be connected to more diversified traffic and platforms. Regarding the developer ecosystem, Weimob Cloud PaaS 2.0 is expected to be launched in 2021-year mid. Through Weimob Cloud PaaS 2.0, the company and third party developers will work together to serve the company's merchants and provide merchants with a series of personalized, industrial and customized solution. The company is currently working with developers such as Baison to develop solutions for different vertical industries. In terms of the investment ecosystem, the company will continue to invest through mergers and acquisitions, direct investment and industrial funds in the future to expand the company's territory in different vertical industries.

3) Globalization strategy - The primary goal of the company's globalization strategy is to assist the Chinese merchants to operate in overseas market by providing overseas independent e-commerce SaaS tools and advertising services. After completing the primary goal, the company will select 1-2 overseas regions and to provide SaaS tools and advertising services to local merchants in these regions. Up to now, the company has begun the negotiation of advertisement agencies with leading overseas advertisers (such as Google, Facebook, Tiktok).

Valuation

We continue to be optimistic about the company's 1) the KA customer expansion in various vertical industries 2) three core strategies, 3) TSO (Traffic + SaaS + Operation) operation model. We believe that the TSO model is expected to further increase the ARPU of the KA customers, thereby uplifting the ceiling of the company's future growth.

After considering that 1) the growth of the gross revenue of targeted marketing is higher than expected 2) The lower advertising rebate from the KAs and Tiktok platform have greater impact to the GPM (comparing to gross revenue) of targeted marketing segment, we lift our 2021/2022 targeted marketing gross revenue to RMB 15.15/19.86 billion and introduce our 2023 targeted marketing gross revenue forecast of RMB 25.67 billion. We maintain our previous 2021/2022 revenue forecast of subscription solution and introduce our 2023 subscription solution revenue forecast of RMB 2.36 billion. We lower our 2021/2022 adjusted NP to RMB 184/347 million from RMB 274/404 million and introduce 2023 adjusted NP of RMB 766 million. We maintain our 2022 subscription solution target PS of 23x and 2022 targeted marketing target PE of 18x, we cut our TP to HKD 26.70 (-5.3%) and upgrade the rating to Buy. (Market closing price as of 26 March) (exchange rate: RMB 0.85/HKD)

Risk

1) The expansion of SaaS customers is worse than expected 2) The increased industry competition 3) Advertising demand is less than expected 4) Targeted marketing business mainly relies on the cooperation with Tencent 5) Valuation of the SaaS sector drops�

Financial Statements

Click Here for PDF format...