|

BAIRONG(6608)

Analysis:

Bairong (6608) is a leading independent AI-powered technology platform in China serving the financial services industry. It provides services and facilitate transactions through its big data and AI technologies. Its services support the needs of FSPs in pre-lending risk management, post-lending monitoring, NPL management and insurance risk management, enabling them to reduce exposure to fraud and improve their underwriting and risk management effectiveness. It also provides big data marketing and distribution services that enable its FSP clients to reach and serve their target customers more effectively. In the first quarter of 2021, the Group recorded revenue of RMB409 million, representing a y-o-y increase of 92%. Among which, the revenue from precision marketing services jumped 293%. (I do not hold the above stock)

Strategy:

Buy-in Price: $24.00, Target Price: $26.50, Cut Loss Price: $22.50

|

NEW WORLD DEV(17)

Analysis:

New World Development (17.HK) is a large-scale integrated property developer. Its core business is property development and property investment in Hong Kong and Mainland China. It also has infrastructure and services, retail, hotel and serviced residences, department store operations, and insurance businesses, focusing on creating an ecosystem, and constantly improving the strategic layout and content construction. The company's FY6/20 revenue was HK$59 billion, a decrease of approximately 23.1% from FY6/19, mainly due to a decrease of approximately HK$19.3 billion in revenue from the property development segment. During the period, the company's property investment income in Hong Kong rose instead of falling, recording HK$1,440.0 million, an increase of 7.1%. During the period, the sales amount of the store located in K11 Art Mall and K11 MUSEA Hong Kong increased by 56%, far surpassing the overall performance of Hong Kong retail sales.

Strategy:

Buy-in Price: $42.00, Target Price: $46.30, Cut Loss Price: $39.85

|

|

LI NING (2331.HK) - 2020 performance is in line with expectations, operating efficiency continues to improve

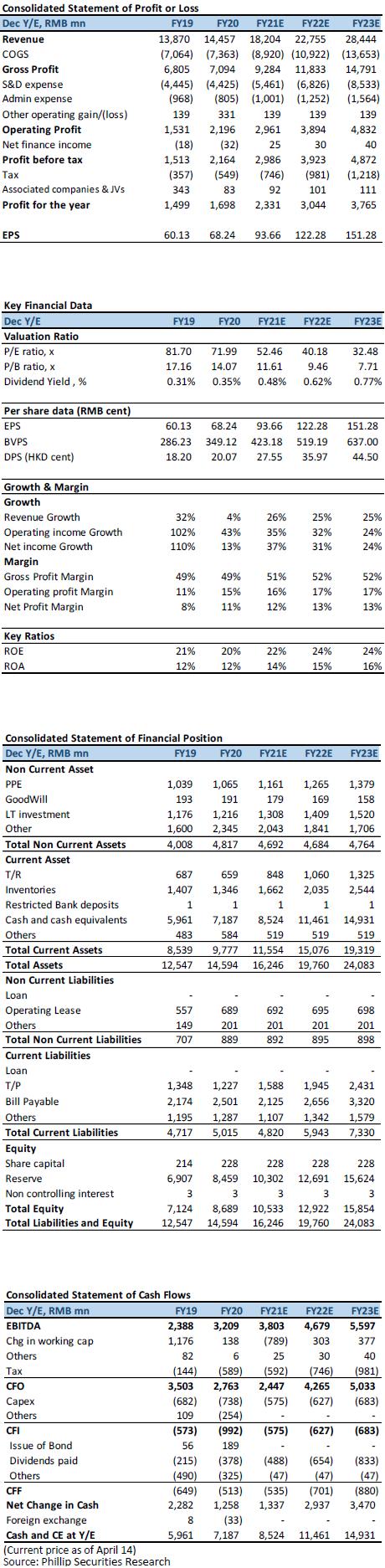

Investment SummaryLi Ning announced on March 19 the company's annual results for the year ended December 31, 2020. The company's 2020 revenue was RMB 14.46 billion, an increase of 4.2% year-on-year, which was in line with our previous expectations (previous expectations: RMB 14.56 billion) , the annual net profit was 1.70 billion yuan, slightly better than our expectation (previously expected: 1.66 billion yuan), an increase of 13.3% year-on-year (including one-off non-operating gains of CNY 234 million in 2019). If the relevant items are excluded, the company Core attributable net profit increased by 34.2% year-on-year. NPM increased from 10.8% to 11.7%, an increase of 0.9 ppts year-on-year, mainly due to the company's proper control of operating costs. The company declared a final dividend of CNY 20.46 cent per share, with a full-year dividend payout ratio of approximately 29.6%. The annual revenue growth MSD, and cost control offsets the impact of the epidemic Li Ning's annual revenue was RMB 14.46 billion, an increase of 4.2% year-on-year. In terms of distribution channels, the company's revenue from retail/wholesale/e-commerce changed by 0.9%/-9.7%/29.9% year-on-year, accounting for 48%/23%/29%, respectively, and the proportion of revenue from e-commerce increased by 5 ppts to 29%. From the perspective of core categories, in terms of retail sell-through, the overall increase was 1% year-on-year compared to last year, but only sports casual recorded a positive growth, an increase of 23% year-on-year, accounting for 39%, and an increase of 7 ppts. Other core categories such as running/training/basketball/non-core are reduced by 9%/16%/4%/9% respectively, and the proportion of retail turnover is 17%/16%/26%/2%. The company's net profit for the year was CNY 1.70 billion, a year-on-year increase of 34.2% based on core net profit, and a NPM of 11.7%, an increase of 0.9 ppts. The GPM was the same as last year, at 49.1%, mainly due to the company's adjustment of the wholesale business price increase during the year, which increased the GPM and offset the negative impact of increased discounts on the GPM due to the epidemic. During the year, the company controlled expenses appropriately, research expenses, advertising and market promotion expenses, and staff costs, accounting for 2.2%, 8.9%, and 9.1% of revenue, respectively, representing a year-on-year decrease of 0.4/0.7/ 1.8 ppts. From the perspective of operating, the company's inventory turnover days were 68 days, same as FY19, reflecting that the inventory of channels affected by the epidemic during the year has also been digested. During the year, the company also adjusted its channels and reduced its low-efficiency offline franchise stores. The total number of stores decreased by 617 year-on-year to 6,933 as of December 31, 2020. Good performance in the 1Q21, conservative revenue guidance For the FY21, the company expects sales growth of 20%-25%, while retail sell-through in various channels will increase by 18%-23%. On the profit side, the company expects to increase its NPM by 1 ppts in 2021. We believe that the company's guidance is relatively conservative. The company's offline retail sales from January to mid-March increased by about 70% year-on-year, compared to a 30% increase in 2019, and the recovery of offline channels is progressing well. As the brand image improves, the room for price increases on products will also be further expanded in the future. Valuation and investment adviceThe company's revenue and profit in FY20 were in line with our expectations. Under the epidemic, revenue still recorded a single-digit positive growth. In addition, cost control and price adjustments also offset the negative impact of discount promotions. With the improvement of operating capacity and the rise of the national trend, we maintain our previous expectation that the company's revenue growth in the next three years will be 25%. With the increase in the company's direct sales ratio and the establishment of brand image, the company's GPM is expected to increase year-on-year. The GPM in FY21/FY22 is expected to be 51%/52%. The company's earnings ratio is at a relatively high level in the industry, mainly because the market has higher expectations for the company's future growth, and the brand image also provides a premium for it, benchmarking against international sports brands. Considering that the company's brand has huge growth potential, profitability will be further improved in the future, and the future earnings growth potential is huge. We have raised the company's FY21/FY22 earnings per share to CNY 93.66/122.28 cents (previously: CNY 82.54/107.58 cents). Based on the company's future revenue growth higher than our previous expectations, we raise our target P/E to FY21 60x. Raise the target price to HKD 66.11, corresponding to 60.00/45.95 times expected earnings ratio in 2021/2022, corresponding to the current price, and maintain the Accumulate rating. (Current price as of April 14) Financials

Click Here for PDF format...

| Recommendation on 16-4-2021 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 57.800 | | Suggested purchase price | N/A | | Target Price | $ 66.110 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2021 Phillip Securities (HK) Ltd. All Rights Reserved.

|