Investment Summary

FY2020 Results Grew Strongly, with Revenue Up by Nearly 50%, beat expectations Again

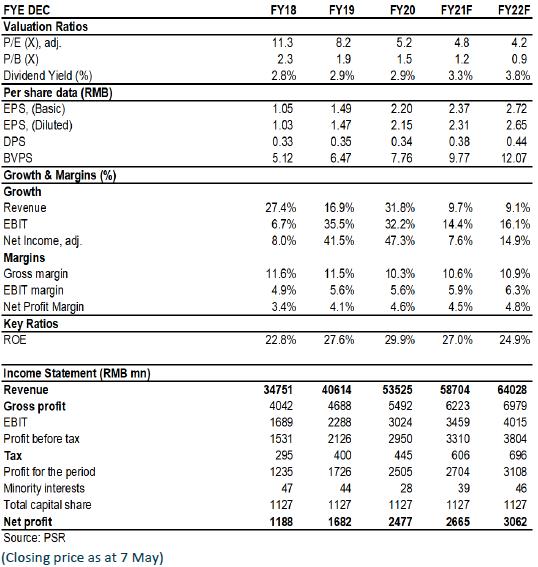

Tianneng Power reported a sales revenue of RMB53.5 billion in 2020, a year-on-year increase of 32%; the profit attributable to shareholders stood at RMB2.5 billion, a year-on-year increase of 47%. Basic earnings per share were RMB2.20. The proposed final dividend was HK$0.4 per share. The dividend payout ratio reached approximately 15%.

Gross Margin in Manufacturing Industry Increased and Expenses Were Well Controlled

The gross profit was RMB5,492 million with a gross margin of 10.26% during the reporting period. There was an increase of 17% and a fall of 1.3 ppts Y-o-Y, respectively. Due to the higher proportion of the trading business with lower gross margin, the overall gross margin has declined compared with 2019. Excluding the trading business, the gross margin of the manufacturing industry increased by 1.7 ppts to 17.1%. The overall battery business witnessed an increase in the gross margin, mainly due to the scale effect brought about by sales increase and the decrease in raw material prices.

The period expense ratio (sales + administration + R&D) decreased by approximately 1 ppt to 5.6%. This was mainly because the expenses were diluted due to rapid revenue growth. At the end of the reporting period, the asset-liability ratio fell by 2.93 ppts, and the ROE increased by 2.7 ppts to 29.9%.

Lead-acid Battery Business Remained Robust, and Lithium Battery and Recycled Lead Businesses Increased Rapidly

The 2020 pandemic has brought changes and opportunities to the economic model. The explosion of demand for private travel and food delivery services has promoted the prosperity of the light electric vehicle industry. In this context, the light electric vehicle battery industry has maintained steady growth. As the leader in the lead-acid battery industry, Tianneng Power's lead-acid battery sales increased by 16.3% from the previous year to 83,972,200 kVAh. Meanwhile, due to the increase in the penetration rate of lithium batteries and the substantial increase in the Company's sales to OEMs, the sales volume of lithium batteries reached 1.69 GWh, up by 120.6% Y-o-Y.

Specifically, due to the lower unit price, the total sales revenue of lead-acid batteries for light electric vehicles was approximately RMB29.65 billion, a slight decrease of 0.6% Y-o-Y. However, due to the faster decline in costs, the segment's gross margin recorded a significant increase Y-o-Y.

In terms of lithium battery and recycled lead businesses, their revenues increased by 69% and 28% Y-o-Y to approximately RMB1.1 billion and RMB1.2 billion, respectively. The Company has continuously released the lithium battery production capacity. The scale effect has appeared. The unit cost of the product has fallen, and the gross margin has increased. The Company had a clear plan for lithium battery capacity expansion. Facilitated by the A-share IPO fundraising, the lithium battery production capacity will be expanded to 4 GWh, including 0.5 GWh of soft pack batteries, 1 GWh of square aluminum shell batteries, and 2.5 GWh of 18650 cylindrical batteries.

In terms of recycled lead business, in addition to the 700,000 tons of lead-acid battery disposal capacity, the Company has added 7,000 tons of lithium battery recycling capacity. Lithium battery recycling will be the Company's key development segment in the future. It may become the momentum for next stage of growth.

Investment Thesis

As environmental protection standards become stricter in China, the concentration of the lead-acid battery industry will continue to improve. With the rapid development of lithium batteries for light electric vehicles and new renewable materials, Tianneng Power is opening up the space for future growth.

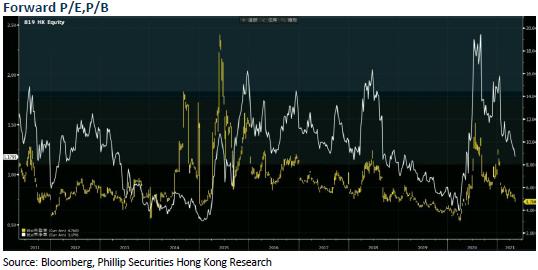

As for valuation, we expect the company's EPS for 2021/2022 to reach 2.37/2.72 yuan and the target price of HK$18, corresponding to 2021/2022 6.4/5.6x P/E and 1.6/1.3x P/B. We maintain a Buy rating. (Closing price as at 7 May)

Financials

Click Here for PDF format...