Investment Summary

The 2020 result is in line with expectation

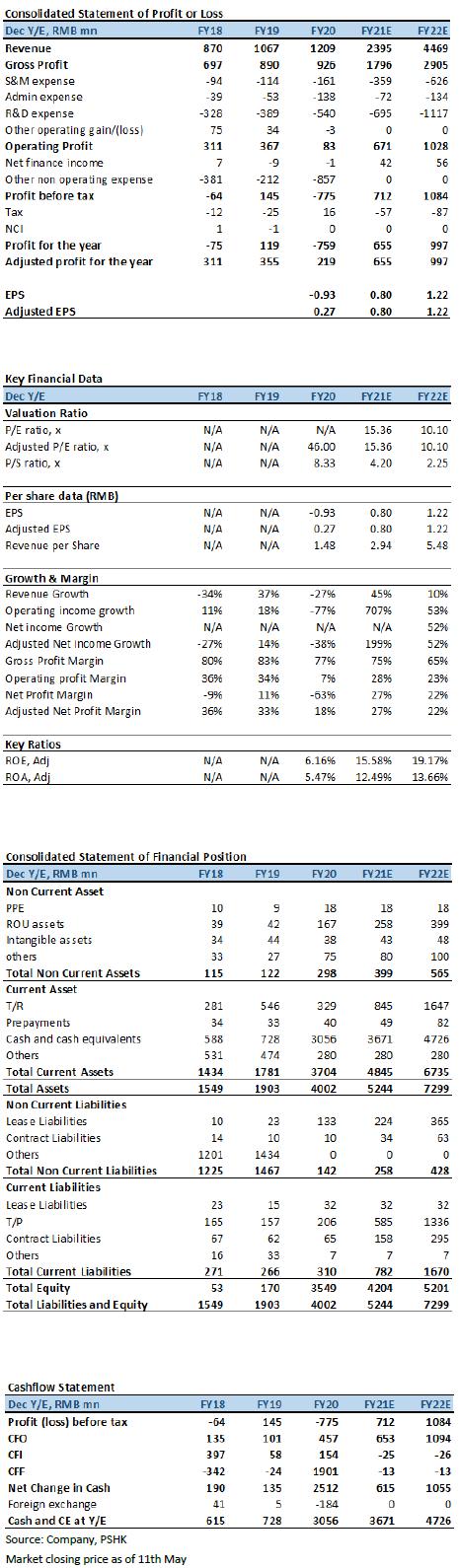

The company's revenue was RMB 1.21 billion (+13.3% YoY) in 2020. Within it, the revenue of the developing and licensing sector /the integrated game publishing and operation sector were RMB 597.3/611.5 million (-27.3% YoY/+148.9% YoY), respectively. In terms of the geographical breakdown, the company's revenue from overseas region in 2020 was RMB 788.3 million (+129.1% YoY), with a revenue proportion of 65.2% (+33.1ppts YoY). The high growth in revenue from overseas region was mainly attributable to the impressive performance of Dragon Raja (龍族幻想). On the other hand, the revenue from domestic region in 2020 was RMB 420.5 million (-41.8% YoY), with a revenue proportion of 34.8% (-33.0ppts YoY). The steep decline in domestic revenue was primarily due to the delay of the launching of the Under the Firmament(鴻圖之下)and The New World(夢想新大陸)in 2020.

The company's GP in 2020 was RMB 925.9 million (+4.1% YoY), with respective GPM at 76.6%(-6.8ppts YoY). The YoY drop in GPM was mainly due to the fact that the revenue proportion of the integrated game publishing and operation sector rose in 2020 and the GPM of the sector is lower in general comparing to the developing and licensing sector, hence dragging down the company's overall GPM (the integrated game publishing and operation sector recognized the full gross billing as revenue, while gross billings` share to payment channels and distribution channels are recognized in the CoGS, hence lower GPM).

In terms of the expenses, the company's R&D expense / selling expense in 2020 were RMB 540.4 million (+38.8% YoY)/RMB 161.0 million (+40.6% YoY), with respective expense ratios of 44.7% (+8.2ppts YoY)/13.3% (+2.6ppts YoY). The increase in both R&D expense and selling expense ratios was mainly attributable to the mismatch in return vs investments (the delays in the launching of games caused a drop in the revenue growth, while the growth rates of expenses were quicker than that of the revenue). The admin expense of the company in 2020 was RMB 138.3 million (+160.9% YoY), with corresponding expense ratio of 11.6% (+6.2ppts YoY). The rose in the admin expense ratio was mainly due to the one-off listing expense recorded in 2020. The adjusted NP of the company in 2020 was RMB 218.8 million (-38.3% YoY), which is in line with our previous forecast.

Maintaining competitive advantages in MMORPG while expanding territory to other game genres

Following the successful launch of Dragon Raja (龍族幻想) in China, the company had successfully launched four new regional versions of Dragon Raja (龍族幻想) in Europe and the Americas, Japan, Southeast Asia and Vietnam with outstanding results. In specific, the Japanese version of Dragon Raja (龍族幻想) became the first Chinese mobile MMORPG to top the Top Free Games Charts of both iOS App Store and Google Play in Japan, once again demonstrating the company's leading R&D and distributing capabilities in MMORPG game genre. On the other hand, the company will continue to expand the game genres in its game portfolio, including SLG and female-oriented game genres. In particular, Under the Firmament (鴻圖之下) launched in October 2020 is the company's first try in SLG and the gross billing of the game exceeded the RMB 100 million mark in the first month since launching.

Continuous improvement in R&D capabilities to build a solid foundation for future products development

Even in the backdrop of Covid-19 and delay of the game launchings in 2020, the company was still actively improving its R&D capabilities. Among the 458 new employees employed in 2020, roughly 855 of them are R&D personnel. In 2021, the company will continue to increase investment in R&D personnel, including providing competitive salary and incentive plans to attract and retain R&D talents. On the other hand, the company has reached a more long-term and in-depth partnership agreement with the game engine developer Epic Games on the issue of Unreal Engine 5 (UE5) authorization, which makes the company one of the earliest game developers allowed to develop games using the UE5. Based on the intensive experiences of the company on Unreal Engines, we believe the company is capable to continuously develop hit-games using UE5 in the future.

We expect 2021-2022 will be the harvest period for the company

It is expected that the company will launch 3 titles in 2021, including The New World (夢想新大陸) which was already launched in January 2021 and 2 other games, namely Noah's Heart (諾亞之心) and Project C. Noah's Heart (諾亞之心) is an open world MMORPG game with a “Seamless Sphere-Shaped Map” and is expected to be launched in year mid, while project C is a SLG game and is expected to be launched before the end of the year. On the other hand, the company has 4 other games on its pipeline, including Project A (female oriented), Project B (MMORPG), Sango Heroes (三國群英傳) (MMORPG) and Project D (MMORPG). All 4 of the games are expected to be launched in 2022. Further the company is expected to launch Under the Firmament (鴻圖之下) in different oversea regions in 2021, including Japan, South-East Asia, HK-Macua-Taiwan and etc.

Valuation and investment thesis

We continue to be optimistic about the company's strong R&D capabilities and high probability of hit game output. In addition, Tencent has further accumulated the company's share, increasing its shareholdings to 16.88% from 12.88%, fully demonstrated Tencent's high recognition of the company's R&D capabilities. Since the game launchings are further delayed, we lowered the company's adjusted net profit for 2021/2022 to RMB 655/997 million from RMB 741/1043 million. We lower our TP to HKD 25.88, with corresponding 2021/2022 adjusted PE at 27.4x/18.0x. We maintain Buy rating. (Market closing price as of 11th May) (exchange rate: RMB 0.85/HKD)

Risk

1) The tightening on Game regulations 2) The Games underperform comparing to expectation 3) Games launching are delayed due to unexpected reasons

Financial Statements

Click Here for PDF format...