Investment Summary

Results in 2020 Were Affected by COVID-19 Pandemic

In 2020, Wanfeng reported sales revenue of RMB10,699 million, down by 15.3% Y-o-Y after retroactive adjustment; profits attributable to shareholders were RMB566 million, down by 36.83% Y-o-Y after retroactive adjustment. Basic earnings per share was RMB0.273. The proposed final dividend was RMB0.1 per share. The interim dividend was RMB0.2. The annual dividend payout ratio was approximately 110%. In April 2020, the Company acquired 55% equity interests in Wanfeng Aircraft Industry Co., Ltd., developing a "dual engine" pattern for the lightweight metal materials in auto parts industry and the general aviation aircraft manufacturing industry. Meanwhile, the historical statements were retroactively adjusted.

The reason for the decline in results was that the main business, the lightweight metal materials in auto parts industry, was negatively affected by the COVID-19 pandemic and the external environment of China-US trade friction. According to calculations, the gross profit of such segment decreased by approximately 23% Y-o-Y; while the other main business, the general aviation aircraft manufacturing industry, has also been affected by the COVID-19 pandemic to a certain extent, which is mainly reflected in the delays in the acceptance inspection and delivery of foreign aircraft orders and revenue recognition. According to the pandemic situation, the Company adjusted its production capacity, accelerated the authorisation transfer process, and mass-produced and sold in domestic aircraft manufacturing plants, to reduce the negative impact of foreign delivery delays. In addition, due to product mix optimization, cost control and other factors, the Company recorded RMB340 million net profit in the aircraft manufacturing industry, up by 48% Y-o-Y, exceeding the commitment for the first-year results by approximately 14%.

The sales expense ratio fell to 1.9%, down by 0.68 ppts Y-o-Y, because the transportation expenses that were originally included in selling expenses were adjusted to performance costs under the new accounting standards; due to an increase of RMB35 million in exchange losses, increase in interest expense and decrease in interest income, the financial expense ratio increased to 2.52%, up by 0.79 ppts. In addition, the decline in revenue caused by the work stoppage due to the pandemic led to an increase in the amortised cost expense ratio. The final net profit margin was approximately 7.15%, hitting a new low since the 2008 financial crisis..

FY21Q1 Profit Increased by Nearly 40% Y-o-Y, But Rising Raw Material Prices Remain a Short-term Concern

In the first quarter of 2021, Wanfeng recorded sales revenue of RMB2,756 million, up by 15.6% Y-o-Y. The net profit attributable to shareholders was RMB168 million, significantly increased by 37.24% Y-o-Y. However, benefiting from share repurchases, in the first quarter, the Company's ROE basically returned to the level of the same period in 2019, up by 1.58 ppts Y-o-Y and up by 0.17 ppts Q-o-Q.

The gross margin in the first quarter was 19.35%, down by 3.15 ppts Y-o-Y. In addition to the changes in accounting standards, we expect that that part of the reason was the rising raw material prices in the first quarter. In the first quarter, the price of aluminum ingots rose by 6.5% from the end of last year, up by over 50% Y-o-Y. As at May 31, the price of aluminum ingots climbed by approximately 15% from the end of last year. By signing a price linkage mechanism with customers, the Company has voluntarily passed on more than 90% of the rising cost of raw materials. However, the rapid increase in aluminum prices in the short term will still have a certain negative impact on the gross margin of the Company's products. The period expenses were well controlled. The period expense ratio decreased by 4.7 ppts Y-o-Y. The net profit margin rose to 7.47%.

Magnesium Alloy Business and General Aviation Aircraft Business Are the Main Spotlight in the Future

The gradually strict environmental protection policies and energy consumption regulations have made it inevitable for auto companies to increase the proportion of lightweight components. In October 2020, the Ministry of Industry and Information Technology issued the Energy-saving and New Energy Vehicle Technology Roadmap 2.0, which further confirmed the development direction of the global automotive technology "low-carbonization, informatization, and intelligence", and proposed the development objectives for China's automotive industry in 2035. After more than 20 years of accumulation of lightweight technologies, Wanfeng has had mature lightweight solutions for automotive metal materials of "magnesium alloy - aluminum alloy - high-strength steel". It is empowering more and more traditional auto companies and new energy auto companies. The Company has already cooperated with auto companies such as Tesla, NIO, Xpeng, and BYD. In the future, it is expected to continue to scale up supporting products and further enhance the matching value of single vehicle.

Regarding general aviation, the domestic general aviation market is in the early stage of development, with a broad market space. In 2020, its subsidiary, Wanfeng Aircraft Industry Co., Ltd., achieved mass production and sales in the first year for the domestic trainer business. Its main customers included well-known aviation schools such as CAFUC (Guanghan), Civil Aviation University of China, FIAA, Longhao Flight Driving Training Co., Ltd., China Flying Dragon General Aviation Co., Ltd., and Chinese Wings. In 2021, the orders in hand have exceeded the workload. The orders are scheduled to 2022. The market share is nearly 70%. Meanwhile, in the previous period, Wanfeng Aircraft Industry Co., Ltd. introduced a state-owned enterprise, Qingdao Wansheng Chengfeng Equity Investment, as a strategic investor, helping accelerate the development of the domestic market.

Investment Thesis

The Company has abundant accumulation in its main business, aluminum alloy wheels. With significant technical advantages, it is expected to continue to consolidate its leading position; there is a vast space for magnesium alloy business and general aviation aircraft business. Product upgrades and multi-category arrangement bring greater flexibility, facilitating long-term stable and high growth. We expect that the Company's wheel business will maintain steady growth. We are optimistic that the Company's magnesium alloy business and general aviation aircraft industry will open up new growth space for the Company.

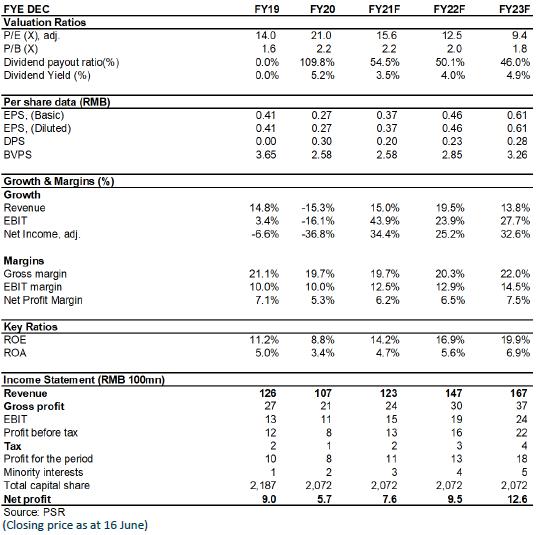

We forecasted the company's EPS in 2021/2022/2023 will reach RMB 0.37/0.46/0.61 yuan, respectively. We give the Company's target price to RMB 7, respectively 19.1/15.2/11.5 x P/E, for 2021/2022/2023, a "BUY" rating. (Closing price as at 16 June)

Risk

Price war among peers

Raw material price increase

New business risk

Financials

Click Here for PDF format...