Investment Summary

Yuyao Country Second Optical Instruments Factory, the predecessor of SUNNY OPTICAL was found in 1984 and was listed on the main board of the Hong Kong Stock exchange in June 2007. The company is principally engaged in the design, research and development, manufacture, and sales of optical and optical-related products. At present, the company has formed eight business sectors: mobile phone business, automobile business, security business, microscopes business, robot business, AR/VR business, industrial detection business and medical detection business. Among them, the market share of handset lens sets (HLS) ranks No. 1 in the world in 2020, the market share of vehicle lens sets (VLS) ranks No.1 in the world for many years, and the headset camera modules (HCM) ranks Top 2 in the world.

HLS strives to be the no. 1

In 2020, the company successfully reached the top in the HLS industry, becoming the highest shipment volume in the world, surpassing its largest competitor in the optical segment business, Taiwan Largan. The company remains optimistic about its HLS shipment volume in 2021 and has given a 15%-20% growth guidance. The company aims to gain more market share in 2021 to consolidate its current position in terms of shipment volume. The company aims to optimize the production line and expand the production capacity of HLS from 160kk per month to 180kk per month to correspond to the guidance on shipment growth.

VLS is expected to become a strong revenue growth segment

The VLS is currently in a stage of upgrading and development. The company entered the VLS field in 2004 and now ranks no. 1 in the world in terms of shipments, with a global market share of 34%, significantly leading other competitors in the industry. In 2021, the growth shipment volume guidance of VLS is 20-25%. In terms of production capacity, it is expected to increase from 6kk to 7kk per month. The company's current global market share in ADAS has more than 50%. With the development of electric vehicles and unmanned driving systems in the future, the company can rely on its relatively high industry technology and experience to maintain its position as the top company in the market.

Goal to become the world's Top 1 in HCM

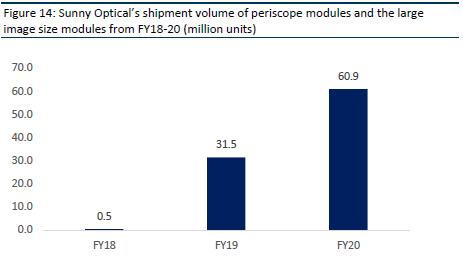

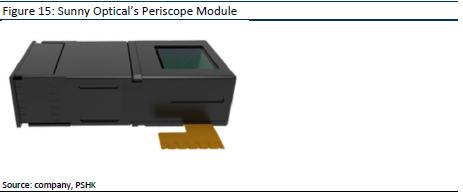

HCM are the main optoelectronic products for the company, including fixed focus modules and autofocus modules. It currently ranks second in the market share, with a market share of approximately 14% and its growth space is broader than other businesses. The company aims to have the highest shipment volume this year, 2021. The shipment volume guidance is increased by 20%-25% yoy. The production capacity is expected to increase from 75kk to 100kk every month. Among them, the periscope modules, and the large image size modules accounted for approximately 10.3% of the shipments (+93.7% yoy), which was higher than the industrial average.

Company valuation

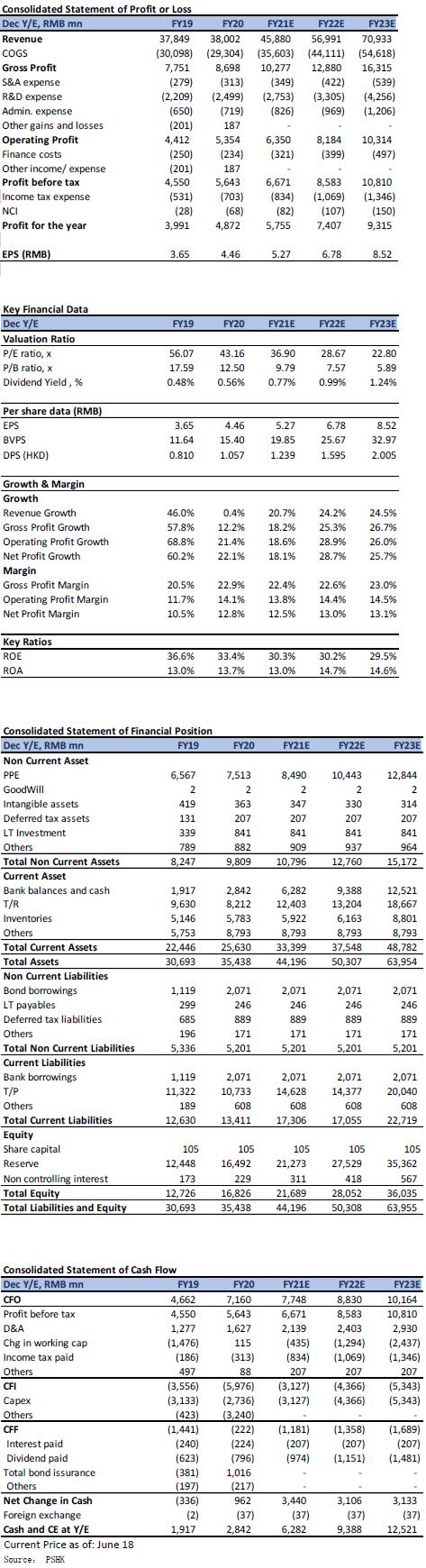

We believe that the company has sound fundamentals and steady growth in various businesses, the volume of the shipment is expected to continue to rise, but it is difficult to make a breakthrough in a short period due to the epidemic. At present, the company's main source of income is smartphone-related products. From the perspective of the medium and long-term in the future, it is expected that the company's vehicle-related products will become a strong growth point and the shipment of VLS will be expected to increase significantly. We expect the company's earnings per share for 2021/ 2022/ 2023 to be RMB 5.27/ 6.78/ 8.52 and the CAGR from 2021-2023 is 27.2%. We give the company a twelve-month target price of HKD 247.8. The price-earnings ratio is 40x/ 31x/ 25x, corresponding to 2021/ 2022/ 2023, the initial cover, gives an “accumulate” rating.

Company Profile

Yuyao Country Second Optical Instruments Factory, the predecessor of SUNNY OPTICAL was found in 1984 and was listed on the main board of the Hong Kong Stock exchange in June 2007. It is the first domestic optical enterprise listed in Hong Kong. The company is principally engaged in the design, research and development, manufacture, and sales of optical and optical-related products. Such products include optical components (such as glass spherical and aspherical lenses, Optical plane products, handset lens sets, vehicle lens sets, security surveillance lens sets and other various lens sets), optoelectronic products (such as handset camera modules, three intelligent equipment for testing). At present, the company has formed eight business sectors: mobile phone business, automobile business, security business, microscopes business, robot business, AR/VR business, industrial detection business and medical detection business. Among them, the market share of handset lens sets (HLS) ranks No. 1 in the world in 2020, the market share of vehicle lens sets (VLS) ranks No.1 in the world for many years, and the headset camera modules (HCM) ranks Top 2 in the world.

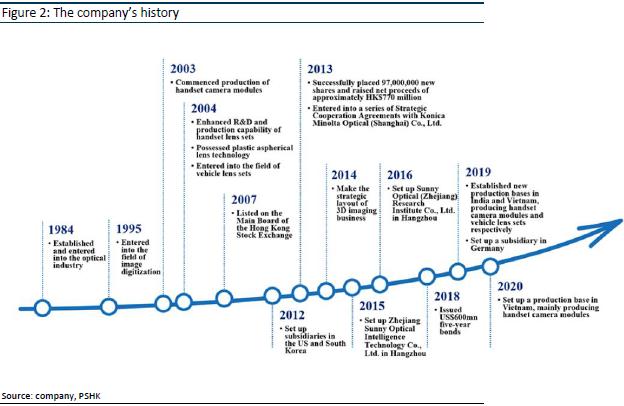

Company Development Process

1984-2004

Yuyao Country Second Optical Instruments Factory, the predecessor of SUNNY OPTICAL was found in 1984. In 1989, it cooperated with the Department of Opto-Instrument of Zhejiang University to establish a scientific and technological production consortium and started the development product model of “You design, I produce”. Later, using foreign capital and commercial channels, the products were sold aboard and quickly embarked on the track of export-oriented enterprises. In 2000, the company was recognized as a “National Key High-tech Enterprise”, marking the company's formal entry into a technology-intensive enterprise.

2004-2013

In 2004, the company adheres to the principle of “customer-centered” which became the key to quickly integrating into the international optoelectronic industry chain. In the same year, the company successfully achieved mass production of HCM and established Sunny Optoelectronics in 2005 to enter the mobile phone industry. Focus on R&D, manufacturing, and sales of optoelectronic products such as HCM.In 2007, the company was successfully listed on the main board of the Hong Kong Stock Exchange, becoming the first domestic optical company to enter the international capital market. In the same year, a well-known German multinational company signed a cooperation project with Sunny Zhejiang Optics to use optical lenses to monitor road conditions when driving. The company noticed that the installation of optical lenses in automobiles will be an inevitable trend in the development of the automobile industry in the future. In 2008, Ningbo Sunny Automotive Optical Technology Co., Ltd. was established to enter the automobile lens automotive industry. In 2012, the company established Sunny Optoelectronics North America Co., Ltd. and Sunny Optoelectronics Korea Co., Ltd. in the United States and South Korea.

2014 till now

At the celebration of its 30th anniversary, the company put forward the grand goal of “1 trillion sales” and determined the strategic direction of “two transformations” which are transformed from an optical product manufacturer to a smart optical system solution provider, and transformation from an instrument product manufacturer to a system solution integrator. In 2016, the company increased its investment in technology and became the first company to mass-produce dual-camera lens module products, seizing opportunities in the high-end HCM market. In 2019, the company established new production bases in India and Vietnam, producing HCM and VLS respectively. In 2020, the company swiftly promote the construction of Yuyao Chengxi Production Base and it is expected to fully deliver by the end of 2021.

Operating condition

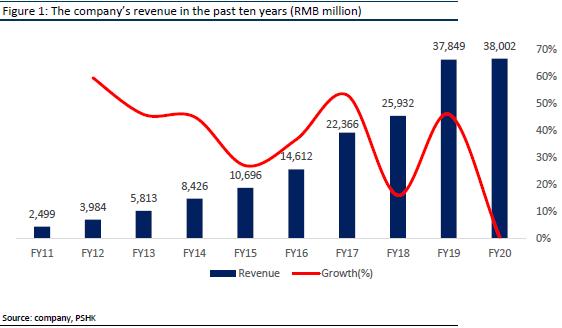

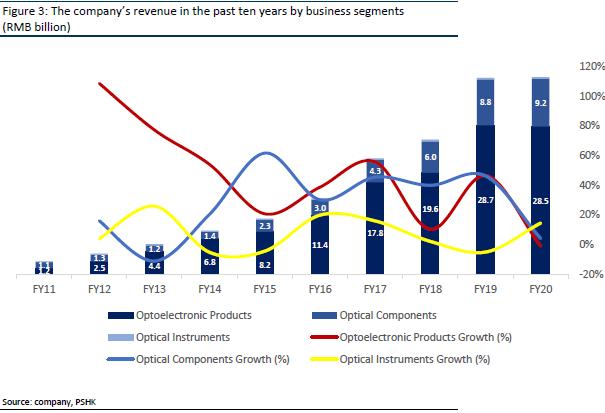

In 2020, mainly due to the pandemic and the Sino-U.S. trading friction, the company's revenue was approximately RMB 38 billion, representing a slight increase of approximately 0.4% compared to the last year. The revenue was RMB 37.8 billion in 2019 (+46% yoy). The CAGR reached 27% from 2016 to 2020. The company is mainly divided into three major business segments: 1) Optical Components, 2) Optoelectronic Products, 3) Optical Instruments which accounted for approximately 24%/ 75%/ 1% of revenue, respectively. Among them, the HLS, VLS in Optical Components and HCM in Optoelectronic Products are the main revenue products.

In 2018/ 2019/ 2020, the company's optical component revenue were RMB 6.023/ 8.815/ 9.181 billion respectively, (+4.1% yoy) in 2020 and CAGR reached 23.5% during 2018-2020. The revenue from optoelectronic products in 2018/ 2019/ 2020 were RMB 19.609/ 28.748/ 28.494 billion, (-0.9% yoy) in 2020 and CAGR is 20.5% during 2018 -2020. The revenue from optical instrument revenue were RMB 300/ 285/ 326 million, (+14.6% yoy) in 2020 and CAGR is 4.2% during 2018 – 2020.

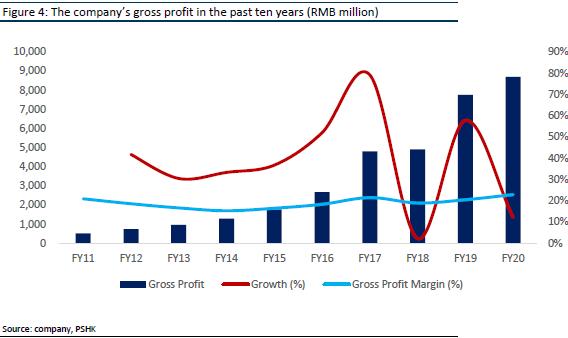

In terms of gross profit margin, benefiting from the company's higher pricing bargaining power, gross profit in 2020 is approximately RMB 8,697 million, yoy increased of 12.2%, gross profit margin is 22.9%, yoy increased of 2.4 ppts. The increase in gross profit margin was mainly attributable to the optimization and automation of the production line module of HCM under the optoelectronic products business which the gross profit margin has increased from 9.3% in 2019 to 12.6% in 2020. This business accounts for approximately 75% of the company's total revenue, resulting in a boost of the overall company's gross profit margin. The gross profit margins of optical components and optical instruments in 2020 were 42.8% and 39.2% respectively, yoy decreased of 2.4% and 2.1%.

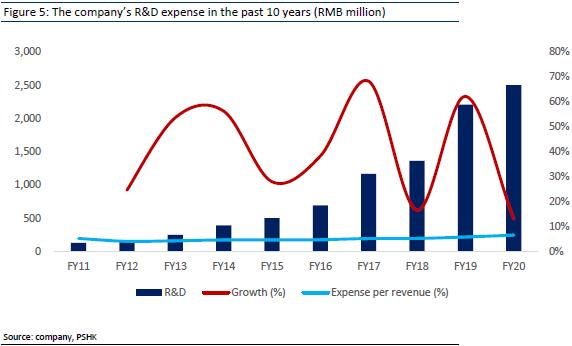

In terms of operating expense ratio, the company's main expense is R&D expense which accounted for 4% - 7% of the total profit on average. The growth of R7D expenses varies with changes in overall revenue which affects the net operating profit. The company's R&D expenditure in 2020 is RMB 2.499 billion, accounting for approximately 6.6% of the company's revenue, yoy increase of 0.8ppts. The increase in overall R&D expenditure is due to the investment in the upgrading of existing products and the new business-related products, such as biological identification business and 3D vision-related market applications.

Shipment Analysis

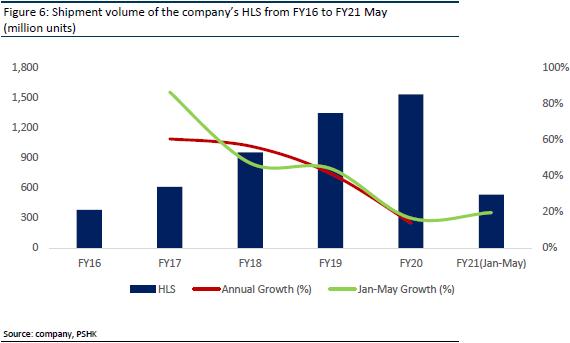

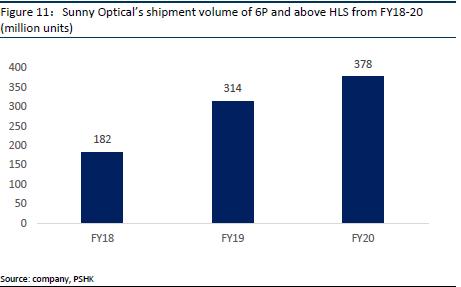

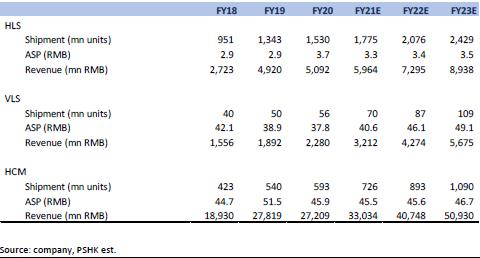

The annual shipments of HLS, VLS and HCM will directly affect the company's revenue growth. In terms of the shipment of HLS, it continued to increase yoy, but the growth rate also continued to slow down. In 2020, the company's shipments of HLS reached 1.53 billion units (+ 13.9% yoy). Its shipment was 1.353 billion units in 2019, (+41.3% yoy). Among them, the shipment volume of the company's 6P and above HLS accounts for 380 million units, around 24.7% of the total shipments, (+20.3% yoy). The total shipment volume of HLS from January to May 2021 was around 631 million. The shipment in May was 99 million units (+2% yoy and -19.7 mom). In the future, the wave of 5G replacement and the trend of the multi-camera lens, the 6P and above HLS market will further push the price and quantity simultaneously.

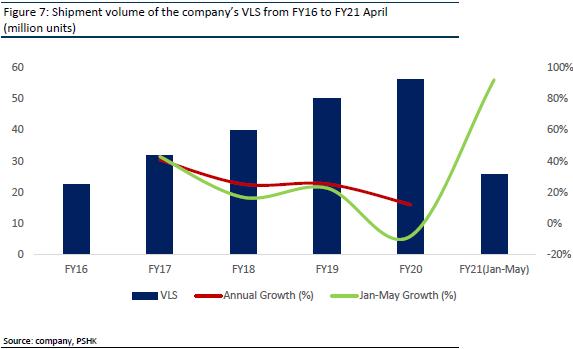

In terms of the shipment volume of VLS, while the overseas customers gradually resumed work in the second half of the year, the company's shipment of VLS rebounded rapidly. In 2020, the total shipment volume of VLS was 56.17 million units (+12.1% yoy), ranking first in the world and 50.1 million units (+25.4% yoy). In 2021, the total shipment volume from January to May was 32.372 million units. The shipment volume in May was 6.614 million (+159.7% yoy and +8.0% mom). As autonomous driving is becoming mainstream, the company is expected to replicate the growth logic of the mobile phone sector, benefiting from the acceleration of localization, and is expected to become the company's new growth engine in the medium to long term.

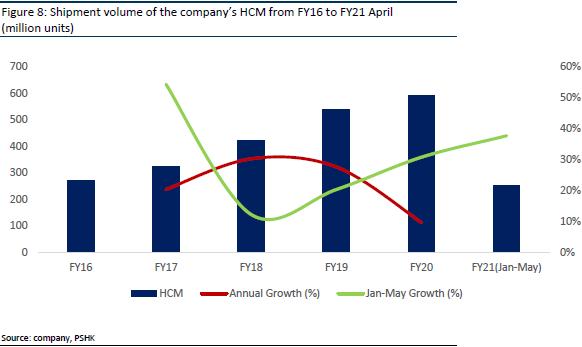

In terms of the shipment volume of HCM, In 2020, the total shipment volume of HCM was 591 million units (+9.7% yoy), and 540 million units (+27.7% yoy) in 2019. Among them, the total shipment volume of the company's periscope modules and large image size modules accounted for approximately 10.3% of the total shipments (+93.7%), the increase is higher than the industrial average. In 2021, the total shipment volume from January to May was 310 million units. The shipment volume in May 2021 was 55.385 million units (+16.0% yoy and -12.7% mom). With the development of the multi-camera configuration of smartphones, it is gradually moving towards a trend of requiring multi-camera modules.

Industry Analysis – HLS

Global smartphone shipments recover and enter integrative market

In 2020, due to the epidemic, Sino-U.S. trading friction and the demand for new configuration from consumer slowed down, the trend of the smartphone market has changed. The poor performance of the smartphone terminal market blocked sales channels, and tight supply chain production has led to a decline in overall smartphone shipments. According to data released by market research agency Canalys, global smartphone shipments in 2020 are approximately 1.265 billion units (-7.5% yoy). Strategy Analytics released global smartphone shipment data for the first-quarter of 2021 with a total shipment of 340 million units (+24% yoy). In the world's first quarter shipments, Samsung is still the world's largest smartphone seller with a market share of 23%, and China's three major mobile phone manufacturers (Xiaomi, OPPO, Vivo) have a market share of 37%. Chip Shortages and supply constraints did not have a significant impact on first-tier brands in the first quarter. Huawei's shipments fell out of the top five, mainly due to US sanctions and chip supply disruptions.

Concentrated competition in HLS market

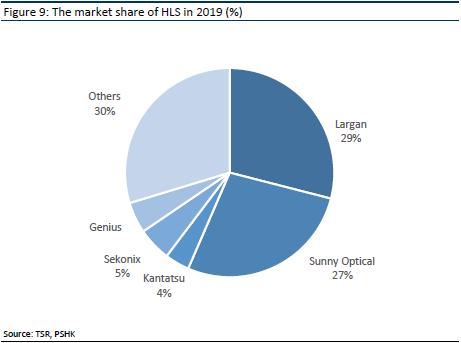

CR 5 in the HLS is about 70%. In 2020, the company's total shipment of HLS has a market share of more than 30%, surpassing the leading competitors in the industry, Largan, and ranked number 1 in the world. Sunny Optical and Largan have a total of nearly 60% of the global market share. Due to the high barriers to HLS technology, the more concentrated competitive landscape, and the oligopoly, the company needs to continue meeting the high production capacity and product yield rate to maintain its market share in the industry. As a leading company in the past, Largan's gross profit margin was as high as 60%-70%. However, due to the epidemic in 2020, the HLS has reduced the allocation and downgraded. Largan's main customer, Huawei, has been affected by the Sino-U.S. trade friction and failed to maintain its technological advantage in the high-end market. Sunny Optical has come from behind and its gross profit margin remains between 40%-50%. On the other hand, since Taiwan's another major competitor, Genius Electronic Optical (GSEO) made a breakthrough in equipment and machines in 2016, its product yield rate has increased significantly and thus, gross profit margin increased from 10% to about 40%, bringing it closer to Largan and Sunny Optical.

Global HLS market expands

In 2020, the specifications of HLS has downgraded, and the global HLS has grown by only 3%, about 4.5 billion units. However, the growth momentum is expected to continue in 2021, and HLS will exceed 5.07 billion units (+11% yoy). Although the mobile phone market has entered the stock market, shipments of HLS has maintained growth. The number of the single-camera lens has continuously increased from 2.2 in 2015 to 3.21 in 2019 and is expected to rise to 4.9 in 2024. The growth momentum of the number of HLS mainly comes from the transition from single front camera to dual camera and the transition from low-end mobile phones to rear four cameras. Mobile phone manufacturers, such as Samsung and Huawei, have also begun to introduce high-end phones with five rear cameras. However, as the camera lens of the mobile phone increases, the thickness of the module will also increase, resulting in obvious camera protrusions on the back of the mobile phone. This will affect the overall appearance of the mobile phone and going against the trend of thinner mobile phones. The configuration scheme of 6 cameras and above can only penetrate in high-end mobile phones market which is difficult to popularize.

In the high-end mobile phone market, due to the high-tech barriers, the upgrade speed of the high-end mobile phones will gradually slow down. For example, Largan has already introduced 8P lenses in its customers` products and further, although some products have begun to carry 9P lenses, it is still in the optimization stage and the technology is not yet fully mature. In addition, competitors such as Sunny Optical, AAC Technologies and Ofilm Group have successfully put into production 7P lenses, and some have also successfully developed 8P lenses, which puts Largan under pricing pressure. To achieve a breakthrough in the future sales of models, smartphone brand manufacturers have to look for cameras with new specifications to increase competitive advantage via differentiated performance, such as ultra-high resolution, ultra- large image size, ultra-large aperture, ultra-wide angle, ultra-miniaturization, high time optical zoom, optical image stabilization in a bid to improve user experiences.

In conclusion, the growth of the market size of HLS is mainly affected by two factors: 1) the increase in sales of HLS, 2) the increase in unit price. In the case of downgraded specification of smartphone cameras presented, this is conducive to the expansion of mid-to-low-end manufacturers, leading to oversupply and the overall average selling price (ASP) of HLS has fallen. However, with the restart and upgrade of HLS in 2021 and the expected 5G replacement wave, the increase in the proportion of high-end products in the future is expected to hedge the impact of price wars on low-end products. It is expected that the ASP of HLS will gradually stabilize.

Industry Analsis - VLS

Due to the epidemic in 2020, the global automotive industry has been hit hard, and overall sales have fallen. According to data from the research institute HIS Markit, global car sales in 2020 will be 76.8 million vehicles, which is far below the peak in 2017 (98 million vehicles). Starting in the second half of 2020, demand for automobiles in the Chinese market has recovered rapidly. With the gradual increase in global demand for electric vehicles, more new vehicles enterprise enter the industry, injecting new impetus into the automotive industry.

Concentrated and limited competitors in VLS

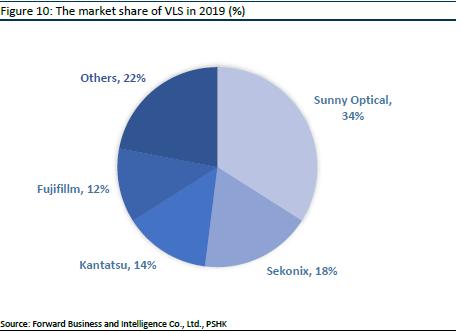

There are few and concentrated competitors in the VLS industry, with CR4 reaching 78%. As a leading company, Sunny Optical has a market share of 34% and more than one-third of the market. Its shipments rank first in the world, followed by Seknoix of South Korea, Kantatsu and Fujifilm of Japan.

VLS maintains rapid growth with positive market outlook

With the increasing concern on global carbon neutrality and environmental protection, the development of the “electrified, connected, intelligent, shared” of vehicle driving, the gradual increase in the penetration rate of advanced driver assistance system (ADAS), and the level of autonomous driving, the overall development of VLS is in the ascendant. From the perspective of hardware architecture, ADAS is mainly for environmental perception, calculation analysis and execution control. ADAS sensors include ultrasonic radar, millimeter wave radar, etc. According to the China Automobile Association's calculations, from 2015 to 2020, the scale of China's ADAS market has grown at a rapid rate, with a CAGR of 50%. Although the year-on-year growth rate has continued to decline, it is still above 20%, and the growth momentum is expected to continue. The main reason is that electric vehicle companies have integrated the ADAS system at the beginning of the architecture design because ADAS is an important application of the software-defined automotive concept, which has become competitiveness comparable to traditional car companies. Since Tesla launched the Model S, more new electric vehicle manufacturers have quickly entered the industry and the penetration rate of ADAS is expected to increase.

On the other hand, the ADAS has a higher requirement for the functions and quality of VLS, especially the side, surround, front, and in-cabin view and other lens sets, which will impose higher requirements on various functional indicators such as accuracy and reliability of the optical components of the vehicle cameras, thereby driving the development of vehicle cameras with high specification.

At present, VLS is mainly used in reversing images (rear view) and 360-degree panoramic view (surround view). According to Yole, the global average number of VLS per car will increase from 1.7 in 2018 to 3 in 2023. The number of onboard lenses for smart cars is generally high. The level 3 high-end car generally will equip more than 5 lenses, and the level 4 will have up to 7-8 lenses, which assist the driver in parking, trigger an emergency brake etc. Taking Tesla Autopilot as an example, a total of 8 lenses are configured, including 3 front lenses, 2 side front view lenses, 2 side rear view lenses and 1 rear view lens. The field of view cover 360-degrees, the farthest detection distance from the front and rear reach 250m and 50m, respectively.

Industry Analysis- HCM

Market fragmentation, leading companies seize high-end market share

Although shipments of the global mobile phone market are declining year-on-year in 2020, the overall sales and performance of the leading companies in the upstream of the industry chain, such as Sunny Optical, Q Tech, Ofilm Group have generally reversed growth. At present, there are not many companies that can supply three-camera and four-camera modules on a large scale, such as South Korea's LGinnotek, Japan's Sharp, Q Tech and Sunny Optical. At the same time, even if smartphones have entered the stock market, the growth of the demand for HCM is still strong. The industry has also deployed advanced technology fields, such as periscope lenses, TOF lenses, and 3D sensing lenses, forming high technical barriers in high-end products, resulting in the continuous increase of the market share of leading companies. The market share of CR5 of HCM has increased from 28% in 2015 to 41% in 2018. However, the total cost of HCM is relatively high and the gross profit margin is low. Moreover, there are many production companies, and the market is relatively scattered. As industry companies suspended low-price competition, the gross profit margin of leading companies has increased significantly.

The current product price competition is fierce, and the competitive landscape is relatively mild for high-end products such as multi-camera, periscope modules, 3D imaging. As the lens continues to upgrade, the technical requirements for module assembly will also increase, and the increase in value can also increase the bargaining power of high-end products. Among them, the global shipments of smartphones equipped with periscope lenses were 15 million units in 2019. With the penetration of high-, mid- and low-end phones, global shipments of smartphones equipped with periscope lenses could exceed 400 million units in 2024.

From the perspective of customer layout, Sunny Optical occupies mainly the demanding Android market, typically the high-end market and continues to increase its share of Samsung mobile phones, which currently account for the highest share of global mobile phone. The return on investment is expected to be higher than that of the Apple industry. Q Tech mainly occupies the low-end Android market. Through technological improvement, it continued to expand in recent years, including Vivo, OPPO, Xiaomi and Huawei.

Company Competitive Advantage

Unswervingly implement the “Mingpeijue” strategy

In 2004, the company adheres to the principle of “customer-centered”, always puts the interest of customers in the first place, responds to customers` needs quickly and has established a stable, close and long-term strategic cooperative relationship with global famous customers in relevant business sectors. At present, the company's main customers in the optical industry are Samsung, Sony, Nikon, Magna, Autoliv, Continental, etc., and the optoelectronics business areas include Google, Qualcomm, Bosch, Amazon, ZTE, Huawei, Lenovo, OPPO, Vivo, Xiaomi etc., instrument business areas such as Carl Zeiss, Olympus etc.

HLS strives to be the no. 1

In 2020, the company successfully reached the top in the HLS industry, becoming the highest shipment volume in the world, surpassing its largest competitor in the optical segment business, Taiwan Largan. The company remains optimistic about its HLS shipment volume in 2021 and has given a 15%-20% growth guidance which is higher than the expected industrial average growth rate of 5%. The company aims to gain more market share in 2021 to consolidate its current position in terms of shipment volume. The company aims to optimize the production line and expand the production capacity of HLS from 160kk per month to 180kk per month to correspond to the guidance on shipment growth.

The company's shipment volume HLS in 2020 is 1.53 billion units (+13.9% yoy) with a record high. Among them, the 6P and above products accounted for approximately 24.7% of the total shipments. Besides, the Group has successfully developed several high-specification products during the year under review, mainly including continuous zoom handset lens sets, 8P high-resolution handset lens sets, freeform handset lens sets and millimeter scale ultra-macro shooting handset lens sets. At the same time, the Group's 100 mega pixel large image size handset lens sets and supers-mall distortion wide-angle (115°) handset lens sets have commenced mass production. As the future wave of 5G replacement and the trend of multi-camera continue, with high technology in the industry, the company can benefit from the availability of new trend of price and quantity in the HLS of 6P and above high-end products.

VLS is expected to become a strong revenue growth segment

The VLS is currently in a stage of upgrading and development. The company entered the VLS field in 2004 and now ranks no. 1 in the world in terms of shipments, with a global market share of 34%, significantly leading other competitors in the industry. In 2021, the growth shipment volume guidance of VLS is 20-25% which is higher than the industry's average growth rate of 15%. In terms of production capacity, it is expected to increase from 6kk to 7kk per month. At the same time, the company has also prepared sufficient factories to expand flexibly according to customer requirements. The company's current global market share in ADAS has more than 50%. With the development of electric vehicles and unmanned driving systems in the future, the company can rely on its relatively high industry technology and experience to maintain its position as the top company in the market.

The company's main products currently include front-view, rear-view, surround-view, side-view, and internal-view lens, and provide a variety of optical radar (LiDAR) optical solutions, HUD optomechanical solutions, with core optical components production experience. Customers cover Europe, America, Japan, South Korea and China, and are widely used in BMW, Benz, Audi, Toyota, Honda, Chrysler, Ford, GM, VW, Volvo and many other models. Drawing on the development experience of smartphones, the company can review the development experience of smartphones, the company can review the development trend of multi-camera and apply in VLS. Meanwhile, the company achieved breakthroughs in the innovation of VLS technology continuously with completed the R&D of 2-mega pixel hybrid front-view VLS which can overcome the technological barrier of temperature stability of lens sets containing plastic lenses. In addition, the pure glass 8-mega pixel front-view VLS with glass aspherical lenses commenced mass production and delivery. It has also completed the R&D of megapixel smart headlight lens sets of vehicles which can help to seize the opportunities in the industry.

From the perspective of mainstream trends, ADAS L2-L3 stages increase the market space of vehicle lens/ modules, autonomous driving L4-L5 accelerates the application and penetration of LiDAR. In the future, with the popularization of automobile intelligence and the decline in costs, the application of HUD will have an upward trend, and the company's development will benefit from the acceleration of localization. In addition to the VLS that the company has deployed for many years, the company is also actively deploying automotive optical-related products, such as automotive camera module, HUD, and LiDAR etc. It is expected to replicate the growth logic of the HLS business, and related businesses will become an important growth segment in the future.

Goal to become the world's Top 1 in HCM

HCM are the main optoelectronic products for the company, including fixed focus modules and autofocus modules. It currently ranks second in the market share, with a market share of approximately 14% and its growth space is broader than other businesses. The company aims to have the highest shipment volume this year, 2021. The shipment volume guidance is increased by 20%-25% yoy, which is higher than the industrial average growth rate of 7%. The production capacity is expected to increase from 75kk to 100kk every month. Among them, the periscope modules, and the large image size modules accounted for approximately 10.3% of the shipments (+93.7% yoy), which was higher than the industrial average.

In the high-end camera modules, the company's market share is higher than that of OFilm and Q Tech, and the unit price of the company's modules is higher than its peers, which is beneficial to maintain its advantage. In addition, the company used to have a relatively low share of HCM in Korean brand customers. Since 2019, the company has begun to cooperate with its customer Samsung and the process goes smoothly. The company successfully equip periscope lenses for Samsung mobile phone in 2020, but the current shipments are not high. At present, the company is also setting factories in Vietnam to produce HCM, mainly serving the manufacturer Samsung. It is expected to be put into production in the fourth quarter of 2021 to gain more market share.

In line with customer demand and the latest development trends of the industry, the Group has completed the R&D of continuous zoom handset camera modules and sensor-shift handset camera modules. In addition, gimbal stabilization HCM and HCM with the second-generation of molding on board and second-generation of molding on-chip packaging technique have commenced mass production.

Multi-point layout in emerging businesses

The company continued to build a robotic vision platform, deploying the two product lines of robotic recognition and positioning. In terms of the biological identification business, the company has deployed a series of biological identification lens sets. In addition, with the gradual landing and clarification of 3D vision-related market applications, the time of flight (“TOF”) products and technical solutions of the Group can be applied to robotic vision, facial recognition payment, smart retail, smart logistics and other related fields. The Group's 3D interactive lens sets adopted new interactive technology that can provide a variety of different types of 3D interactive lens sets following customer demands.

The face scan payment solution based on ToF technology has obtained the WeChat testing certification, thereby allowed to enter the supply chain of WeChat pay equipment manufacturer customers; and the Group completed the development of a structured light system applied to smart door locks and conducted strategic cooperation with customers. In terms of the positioning business, the Group completed the R&D of the ToF-related algorithm of the sweeping robot and the development of the binocular solution and completed the project delivery with key customers.

Financial forecast

The company's 90% of the revenue are from three main products (HLS, VLS, HCM). Estimating the profit growth of the company from three main products, based on the proportion of the company's revenue, the company's three businesses account for approximately 74%/ 25%/ 1% of the total profit. It is expected that the company will enter a key growth year in 2022, mainly due to the impact of the 5G replacement wave, the recovery of the supply chain and the overall development of electric vehicles. It is predicted that the company's revenue from optical components in 2021/ 2022/ 2023 will be RMB 10.742/ 13.105/ 16.119 billion, the CAGR from 2021-2023 is 22.5%. The company's revenue from optoelectronic products in 2021/ 2022/ 2023 will be RMB 34.763/ 43.454/ 54.317 billion, the CAGR from 2021-2023 is 25%. The company's revenue from optical instruments in 2021/ 2022/ 2023 will be RMB 375/ 432/ 496 million, the CAGR from 2021-2023 is 15%. The total revenue in 2021/ 2022/ 2023 will be RMB 45.880/ 57.991/ 71.933 million, the CAGR from 2021-2023 is 24.3%.

In terms of gross profit margin, it is expected to be 22.4%/ 22.6%/ 23.0% in 2021/2022/2023. Considering that the gross profit margin of HCM under the optoelectronic products has increased from 9.3% in 2019 to 12.6% in 2020, the gross profit margin will be relatively stable in the coming year. In terms of mobile phones and car lenses, it is expected that with the economic recovery in 2021, the demand and shipments of low-end products will increase significantly, and gross profit margin will be reduced as a result, and the high-end products will return to the market focus in 2022/ 2023. Thus, the gross profit margin will gradually recover.

In terms of expense, it is predicted that the company will continue to increase R&D expenses and increase with the increase in total profit income to maintain competitiveness in the industry. The corresponding R&D expenses in 2021/ 2022/ 2023 are RMB 3.034/ 3.826/ 4.833 billion. It accounts for approximately 6.7% of total profit revenue.

Company valuation

As of June 18, the closing price was 228.6 HKD, the company's rolling price-earnings ratio was 42.47x. The company's historical valuation has been between 25-40x for a long time in the past 3 years. We believe that the company has sound fundamentals and steady growth in various businesses, the volume of the shipments is expected to continue to rise, but it is difficult to make a breakthrough in a short period due to the epidemic. At present, the company's main source of income is smartphone-related products. From the perspective of medium and long-term in the future, it is expected that the company's vehicle-related products will become the strong growth point and the shipment of VLS will be expected to increase significantly due to the growth of the ADAS market, vehicle modules, LiDAR optical solutions and HUD optomechanical solutions will become company's new growth engine which may increase the proportion of the company's business revenue. As the company continues to benefit from the high industry boom and the company is a leader in the optical industry, it has been focusing on the development and R&D of the optical business for many years. At present, with considering the vehicle-related products are having a bright prospect, we give the company a target price-earnings ratio of 40x for 2021, which is higher than the industry average price-earnings ratio.

We expect the company's earnings per share for 2021/ 2022/ 2023 to be RMB 5.27/ 6.78/ 8.52 and the CAGR from 2021-2023 is 27.22%. We give the company a twelve-month target price of HKD 247.8. The price-earnings ratio is 40x/ 31x/ 25x, corresponding to 2021/ 2022/ 2023, the initial cover, gives an “accumulate” rating.

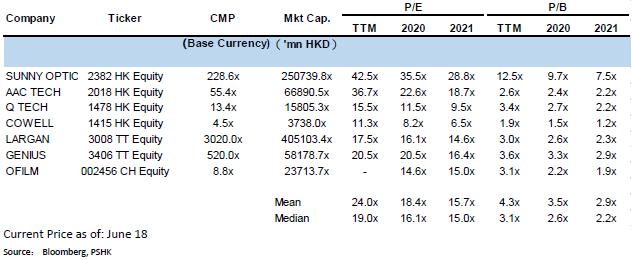

Peer Comparison

Risk factors

1) Epidemic

2) The 5G replacement wave and the demand for electric VLS are less than expected

3) The company's shipment growth is less than expected

4) Cross-market valuation may be at risk of overestimation due to declining enthusiasm for emerging businesses

Financial

Click Here for PDF format...