Investment Summary

Results Hit a Record Q1 High in 2021Q1

According to the results report for Q1 2021, Fuyao Glass reported revenue of RMB5,706 million in 2021Q1, up by 36.8% yoy, and down by 6.9% qoq; the net profit attributable to the parent company was RMB855 million, up by 85.9% yoy, and down by 2.6% qoq; the net profit attributable to the parent company excluding non-recurring items was RMB813 million, up by 113.8% yoy, and up by 2.4% qoq. The reason for the year-on-year increase was the low base in the same period due to the coronavirus pandemic in 2020. However, compared to the first quarter of 2019, Fuyao Glass's revenue, net profit attributable to the parent company, and net profit attributable to the parent company excluding non-recurring items still increased by 15.7%, 41% and 57%, respectively, hitting a record high in its first quarter. In addition, after deduction of the exchange gains and losses caused by the exchange rate turbulence in the first quarter, the total profit increased by 102.8% yoy, which is far higher than 67.8% before the deduction. Compared to 2020Q4, the results declined slightly in 2021Q1, mainly dragged by the shortage of chips in the automotive industry.

Rising Capacity Utilisation Rate Drove Year-on-year Increase in Gross Margin

The Company recorded a 40.6% gross margin in 2021Q1, up by 6.2 ppts yoy, and down by 2.2 ppts qoq. The significant yoy increase was mainly due to 1) the lower base caused by the low capacity utilisation rate due to the pandemic last year, and 2) the substantial year-on-year decrease in losses of the Germany-based subsidiary SAM. The qoq decline was mainly due to the shortage of chips in 2021Q1, which resulted in a lower capacity utilisation rate than in the fourth quarter of 2020.The period expense ratio was 22.3%, up by 1.6 ppts yoy. Specifically, the sales expense ratio, administration expense ratio, R&D expense ratio, and financial expense ratio was 7.3%, 8.9%, 4.1%, and 2.0%, respectively, down by 0.2 ppts, down by 2.1 ppts, up by 0.5 ppts, and up by 3.5 ppts, respectively yoy. The increase in financial expense ratio was mainly due to fluctuations in exchange gains and losses (RMB142 million), which resulted in an increase of RMB180 million in financial expenses over the same period last year.

The Smart Car Era Is Coming, and the Company Will Benefit from the Value Improvement of Single Vehicles in the Long Term

In order to promote technological upgrading and increase the added value of products, the Company has maintained a higher R&D input ratio in the industry. In the first quarter of 2021, the R&D expense ratio reached 4.13%, up by 0.5 ppts yoy. In 2020, the proportion of high value-added products, such as thermal insulation glass, head-up display glass, and dimmable glass, increased by approximately 2.64 ppts compared with the same period last year. Benefiting from the demonstration effect brought by Tesla, several automotive manufacturers began to launch new models with canopy glass in 2020. It is expected that canopy glass will be popularized rapidly from 2021. In the future, the Company's matching value of glass for single vehicles is expected to increase by 2 to 3 times, to stimulate the continued growth of follow-up results. On the other hand, in 2020, the Company signed strategic cooperation agreements with partners such as BOE and Beidou Zhilian to strengthen cooperation on smart dimming automotive glass, car window display, high-precision GNSS positioning and communication multi-mode smart antenna + automotive glass fusion solutions. The penetration rate of smart glass such as HUB glass is expected to further increase with the rapid development of automobile intelligence. The Company also raised funds to enter the field of photovoltaic glass, continuously expanded its product mix, and further established its long-term sustainable growth.

Investment Thesis

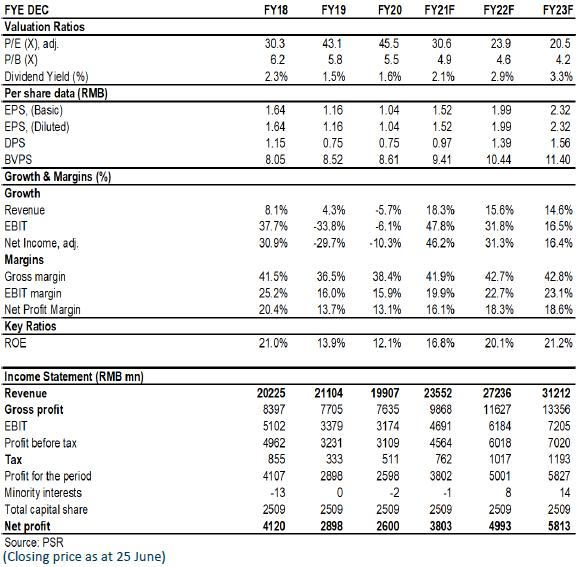

Overall, considering the steady leading position, continuous optimization of the product structure and a high dividend rate, we give the "Accumulate" rating, with a slightly revised target price to be HK$60, equivalent to 33/25.6/22x P/E for 2021/2022/2023E. (Closing price as at 25 June)

Risks

Demand for automobiles keeps sluggish; cost of raw materials increases; RMB appreciates

Catalyst

Success market development of overseas automobile market; rebound of domestic demand for automobile; depreciation of RMB

Financials

Click Here for PDF format...