Investment Summary

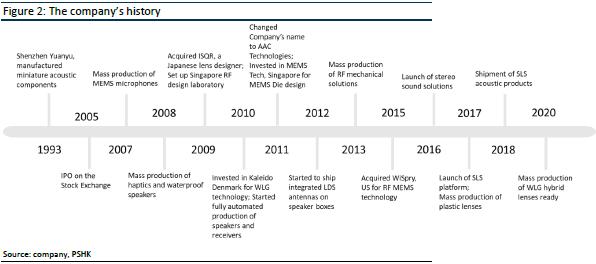

Shenzhen Yuanyu, the predecessor of AAC Technologies was found in 1993, started to manufacture miniature acoustic components and was listed on the main board of the Hong Kong Stock exchange in 2005. The Company is the world's leading solution provider for smart devices with cutting-edge technologies in materials research, simulation, algorithms, design, automation and process development in Acoustics, Optics, Electromagnetic Drives and Precision Mechanics, and MEMS, providing advanced miniaturized and proprietary technology solutions in smartphones and portable electronic devices across the world.

Gross profit margin of Acoustics increases sharply, launching standardized small-cavity speaker module in Android market

In terms of gross profit margin, the gross profit margin of the company's core business dynamic components has risen sharply from 28% in 2020, to 37.4% in the first quarter of 2021 (+11.4 ppts yoy, +9.4% mom). It is expected that the segment's annual gross profit margin will end the three-year continuous downward trend. The company has been deploying on Android customers in recent years, and the revenue and gross profit provided by Android customers to the company will continue to rise in 2020. In the first quarter of 2021, half of the company's segment revenue is contributed by Android customers, and gross profit is approximately 28%. In addition, the company has introduced standardized small-cavity speakers to improve the versatility to be applicable to various Android phone models. Account for about 20%-30% of total shipments in 2021, the company aims to standardize small-cavity speakers to account for about 70%-80% of total shipments in the future. It is expected that the company will still have huge room for growth in the Android market in the future, and its gross profit margin will also increase further.

Gross profit margin of plastic lens rise sharply, WLG lens technology expected to overtake in concers

Until the fourth quarter of 2020, the market share of plastic lenses has steadily increased, and the monthly output of plastic lenses has reached the level of 7kk-8kk per month in the fourth quarter. Its gross profit margin has risen sharply from -2.7% in the second quarter of 2019 to 28% in the fourth quarter of 2020, and its gross profit margin in 2021 reached 36.3%, which is close to the gross profit margin of the leading company Sunny Optical in plastic lenses, mainly due to product quality. In addition, the company's first WLG project has been successfully shipped in the first quarter of 2021, and the first mobile phone equipped with WLG glass-plastic hybrid lens has been promoted in the market. This product uses the 1G5P WLG glass hybrid lens solution. Compared with a plastic lens of the same specification (corresponding to a 6P lens), the light input is increased by 15%, the resolution is increased by 5%, and the overall lens height will be reduced by 5-10%.

Financial forecast and company valuation

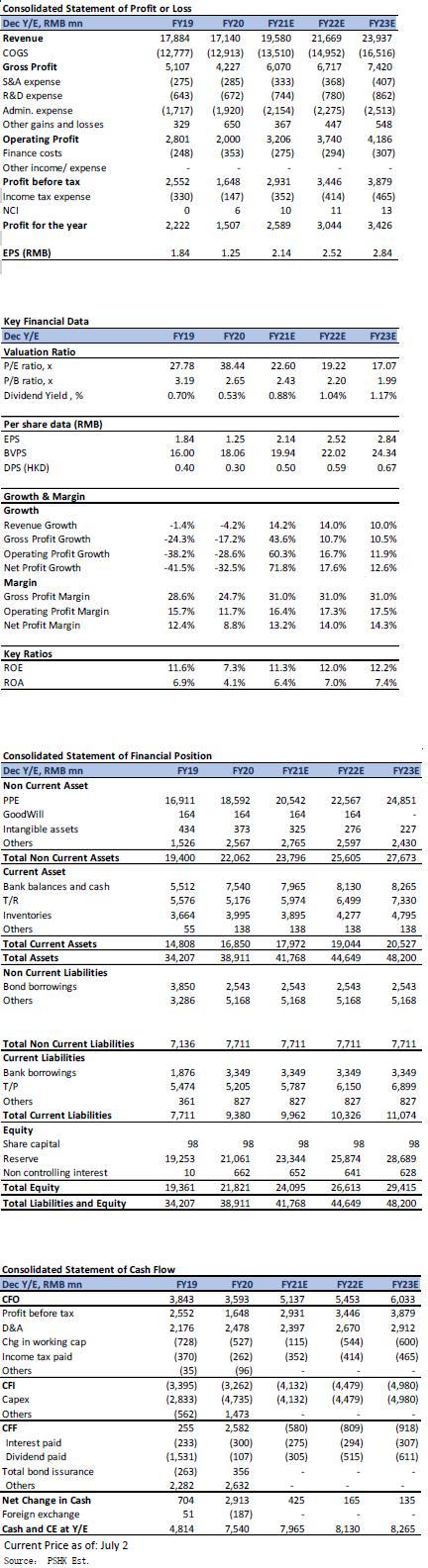

From the first quarter report, the reveneue is RMB 4.29 billion (+21% yoy). It is expected that the overall revenue will increase in the third and fourth quarters during the peak seasons of mobile phone nad other electronic product sales. To reverse the company's three consecutive years of decling revenue, it is predicted that the revenue in 2021/ 2022/ 2023 will be RMB 19.58/ 21.67/ 23.94 billion (+14% yoy in 2021).

Considering the company's leading position in the acoustics industry, expansion of the optical business, and the expected end of three consecutive years of negative growth in revenue and gross profit, the company is given an “accumulate” rating (first coverage). The 2021 target price given to the company is HK$63.0, which corresponds to a P/E ratio of 25x/ 21.26x/ 18.89x, corresponding to the EPS of 2021/ 2022/ 2023.

Company Profile

Shenzhen Yuanyu, the predecessor of AAC Technologies was found in 1993, started to manufacture miniature acoustic components and was listed on the main board of the Hong Kong Stock exchange in 2005. The Company is the world's leading solution provider for smart devices with cutting-edge technologies in materials research, simulation, algorithms, design, automation and process development in Acoustics, Optics, Electromagnetic Drives and Precision Mechanics, MEMS, Radio Frequency and Antenna, providing advanced miniaturized and proprietary technology solutions in smartphones and portable electronic devices across the world.

Company Development Process

Shenzhen Yuanyu, the predecessor of AAC Technologies was found in 1993 and started to manufacture miniature acoustic components. In 1998, the company started to massively produce transducers and massly produce multifunctional receivers, high-quality speakers and ECM microphones in 2002. In 2005, the company was listed on the main board of the Hong Kong Stock exchange. In 2008, the company produce of haptics and waterproof speakers massively in 2008. In 2009, the company started to target the optical business and acquired ISQR, a Japanese lens designer. In 2010, the company started fully automated production of speakers and receivers. In 011, the company changed its name to AAC Technologies and started to ship integrated LDS antennas on speaker boxes in 2012. In 2013, the company produced RF mechanical solution. In 2015, the company acquired WiSpry, US for RF MEMS technology and commenced 3D glass business to build on optic foundation. In 2016, the company launched of stereo sound solutions and achieved delivery of bulk orders for miniaturized lens. In 2018, the company transformed into Smart Manufacturing and a new era of big data supported high precision manufacturing. In 2019, the company become one of the top 3 global supplier of plastic lenses for smartphones and started to produce WLG hybrid lenses massively in 2020.

Operating condition

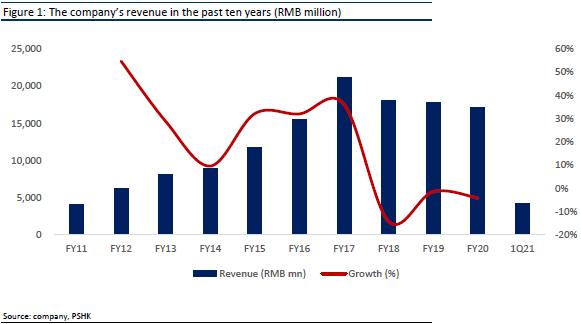

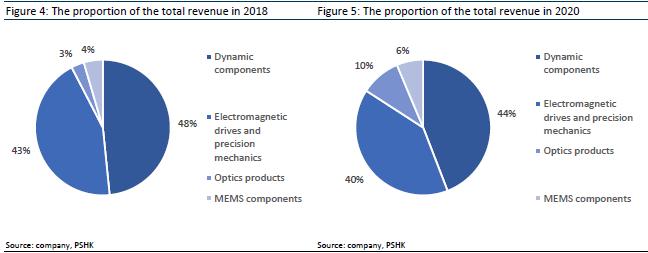

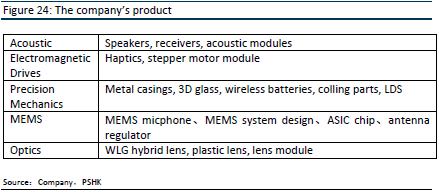

In 2020, due to the impact of the global epidemic on the supply chain, the company's total revenue was RMB 17.14 billion (-4.2% yoy), while the total revenue in 2018/ 2019 was RMB 18.13/ 17.88 billion (-14.1%/ -1.4% yoy). The revenue has experienced negative growth for three consecutive years, and the CAGR for the period 2018-2020 is -2.77%. The company is currently divided into four major businesses: 1) Dynamic components, 2) Electromagnetic drives and precision mechanics, 3) Optics products, 4) MEMS components, which account for approximately 44%/ 40%/ 10%/ 6% of the revenue in 2020, respectively. The company has been in the optical business for many years and has made significant breakthroughs in 2020. The proportion of optical business in total revenue has increased from 3% in 2018 to 10% in 2020 and the CAGR of segment revenue for 2018-2020 is 72%. However, the revenue of the acoustic and electromagnetic drives and precision mechanics business continued to decline, mainly due to the slowdown in the upgrade demand of its main customer, Apple.

In 2020, dynamic component was the company's largest business segment, accounting for 44% of total revenue, and the segment revenue was RMB 7.56 billion (-7% yoyo); the company's second largest business segment was electromagnetic drives and precision mechanics, which accounted for 40% of total revenue. Segment revenue was RMB 6.85 billion (-11% yoy); Optical business is currently a rapidly growing business of the company, but currently only accounts for 10% of the company's total revenue, segment revenue was RMB 1.63 billion (+53% yoy); The MEMS components accounted for 6% of total revenue segment revenue was RMB 1.08 billion (+17%).

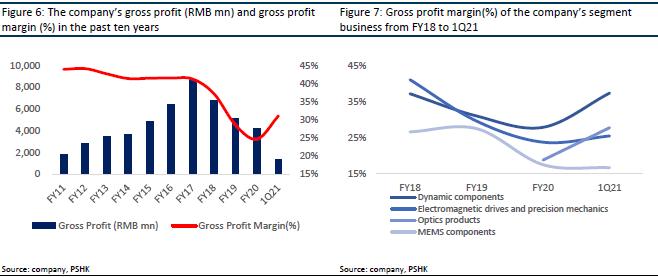

In terms of gross profit margin, the company has remained at around 41.5% from 2013 to 2017, but since 2018, the overall gross profit margin has begun to decline. The company's gross profit margin for 2018/ 2019/ 2020 is 37.2%/ 28.6%/ 24.7%. The gross profit margin in 2020 has dropped by 3.9% year-on-year which dynamic components, electromagnetic drives and precision mechanics, as well as MEMS components have all shown a continuous downward trend. The company's gross profit for 2018/ 2019/ 2020 was RMB 42.3/ 51.1/ 6.74 billion (-22.7%/ -24.3%/ -17.2% yoy).

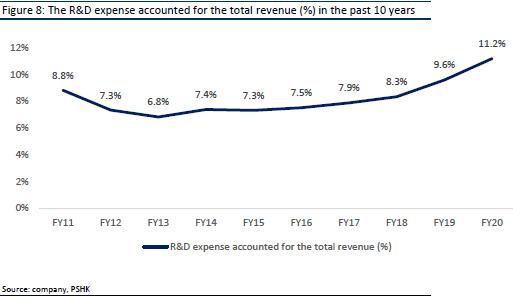

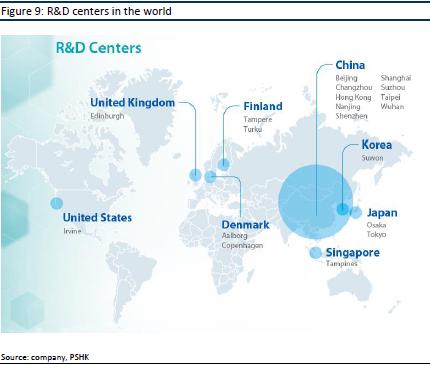

In terms of expense ratio, the company always aims to “lead innovation and enhance user experience”. Focusing on high-tech entry barrier and high value-added precision manufacturing business and establishing the leading edge in each segment, we achieve sustainable development capability. Therefore, a large amount of research and development expense are invested every year, and the proportion of research and development expenses in total revenue has been increased in the past 8 years. In 2020, R&D expenses were RMB 1.92 billion, accounting for 11.2% of total revenue, (+1.6ppts. yoy). The company has set up 19 R&D centers all over the world, with 4,335 R&D talents, and by the year end 2020, obtained 6,034 patents as well as 6,287 patent applications.

Industry Analysis

Global smartphone shipments recover and enter integrative market

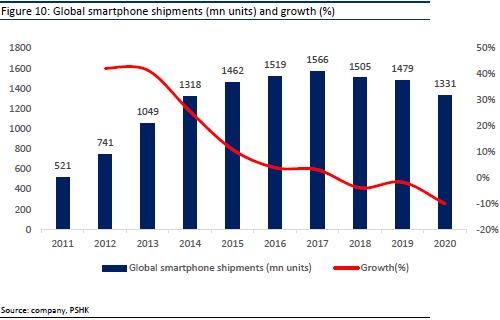

In 2020, due to the epidemic, the shortage of components such as chips, and the slowdown in consumer demand for new equipment, the pattern of the smartphone market has changed. The poor performance of the smartphone terminal market, restricted sales channels, and tight supply chain production have led to a decline in overall smartphone shipments. Besides, the global mobile phone equipment configuration has been downgraded, and the 5G replacement wave has slowed down. Accounting to the data released by Counterpoint, a market research organization, global smartphone shipments will be 1.33 billion units in 2020, (-10% yoy). Subsequently, market research agency Canalys announced that global smartphone shipments in the first quarter of 2021 were 347 million units, (+24% yoy). In the first quarter of the world's shipments, Samsung is still the world's largest smartphone seller, with shipments of 76.5 million units and a market share of about 22%. China's top three mobile phone manufacturers (Xiaomi, OPPO, Vivo) have a market share of 37%; Apple's mobile phone shipments are the second, reaching 52.4 million units, accounting for 15% of the total shipments, compared with 37.1 million units shipped in 2019 (+41% yoy).

Accounting to the authoritative release of CAICT, China's smartphone market has shown a clear recovery, and domestic 5G mobile phone shipments accounted for the increase in total smartphone shipments, accounting for more than 70% from March 2021. The rapid growth in the number of 5G users is a major factor in promoting equipment replacement. As of the end of the first quarter of 2021, 5G users have exceeded 350 million, and operators are also accelerating the migration of 4G users to 5G: operators reduce 4G packages and switch to new users or old users provide 5G packages, so it is expected that when most consumers in China change their devices, 5G smartphones will become the best choice. According to the Ericsson Mobile Trends Report, it is estimated that there will be 3.5 billion 5G users by the end of 2026, accounting for more than 50% of mobile data.

The degree of integration of consumer electronics products is getting higher and higher, and the demand for miniature speakers is also increasing. Speakers are the basic configuration of most electronic consumer products, and the usage of stand-alone devices has shown an upward trend year by year. At present, mobile phones, laptop computers, headsets and other electronic consumer products are equipped with speakers or receivers. Among them, the number of micro speakers in emerging applications such as wireless (TWS) headsets and smart speakers has continued to increase: acoustics components are the core accessories of TWS headsets. The outbreak of TWS headsets will further drive the development of the upstream acoustic device market in the industry chain; At the same time, the penetration rate of smart speakers among consumers is rapidly increasing. Smart speakers are equipped with acoustic device equipment. At present, smart speakers are still an incremental market. Acoustic devices will therefore be driven by a significant market growth. According to data released by the New Sijie Industry Research Center, the global micro speaker market size was 8.86 billion U.S. dollars in 2017, and its market size rose to 9.57 billion U.S. dollars in 2019. The 2017-2019 compound annual growth rate is 3.9%, and it is expected to be in 2024. It is expected to break through to 11 billion U.S. dollars or more in the year, with a compound annual growth rate of 2.8% in 2019-2024. According to the analysis of Counterpoint Research Institute, global TWS headset shipments exceeded hundreds of millions of pairs in 2019, with shipments of nearly 129 million pairs, a year-on-year increase of 179%. Among them, in the fourth quarter of 2019, Apple TWS headsets accounted for 41% of the global market share, followed by Xiaomi, Samsung, QCY and JLAB.

In terms of stereo sound, two or more independent sound effect channels are mainly used to express sound with a certain level of azimuth, rather than playing through a single speaker. In terms of mobile phone applications, Apple mobile phones have been using dual speakers since the iPhone 7 series. At present, Apple manufacturers do not have an obvious plan to increase the configuration and number of speakers; In terms of Android products, the current coverage rate is not high. In the future, with the technical optimization of speakers such as standardized small-cavity speaker modules, the utilization rate of Android's overall dual speakers will increase.

MEMS microphone technology breakthrough, gradually replaces EMC microphone

The microphone of acoustic devices is mainly a key device for collecting sound, and the early application is mainly electret condenser microphone (ECM). At the end of the 20th century, after Knowles invented the MEMS microphone, this product replaced some of the application scenarios of ECM with its technological advantages. Both use the principle of capacitor charging and discharging to operate. The diaphragm of the capacitor plate will vibrate due to sound, causing the charge between the plates to change, thereby performing signal transmission. However, there is a big difference between the two in terms of physical structure. MEMS microphones are the product of semiconductor technology, with higher performance density and relatively low temperature sensitivity difference. Compared with ECM, MEMS microphone has more uniform frequency response between components, and the performance of the final product is more stable.

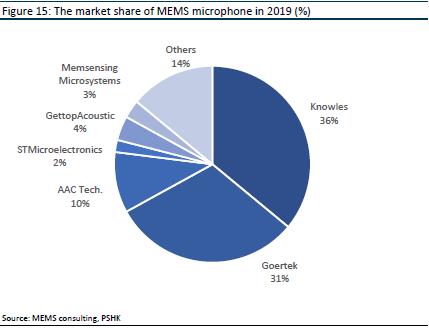

According to data from China's MEMS consulting service company, in 2019, Knowles has the world's first MEMS microphone market share, accounting for 36%; Followed by Goertek shares, accounting for 31%; AAC Technologies ranks third with a global share of 10%. As early as 2010, Knowles was an absolute leader in the MEMS microphone market, with a market share of over 80%. With the progress of Chinese MEMS microphone manufacturers in recent years, Goertek, AAC Technologies, GettopAcoustic, and Memsensing Microsystems have also become major players in global MEMS microphones, with a total market share of 48%, accounting for nearly half of the global market. Well-known manufacturers such as Knowles, Goertek and AAC Technologies mainly compete in the high-end market, with typical customers such as Apple and Samsung; Dozens of domestic manufacturers represented by GettopAcoustic and Memsensing Microsystems are growing rapidly and are developing in the low-end market.

According to data from Memes Consulting, the global MEMS microphone market has grown from RMB 1.59 billion in 2010 to RMB 8.68 billion in 2019, with a CAGR of 20.75% from 2010 to 2010. In the past, the huge global smartphone shipments accelerated the scale of the MEMS microphone market, mainly because MEMS microphones are the standard configuration of smartphones. Some high-end smartphones even use 3-4 MEMS microphones: One is used for sound collection, one or two is used for noise cancellation, and one is used to improve speech recognition.

Nowadays, voice-based virtual personal assistants have become the main driving force of the audio industry. Major technology companies around the world are participating in the competition, such as Apple's Siri, Amazon's Alexa, Google's Google Assistant, and Microsoft's Cortana. And this technology can be used in various electronic product systems, in addition to smart phones, but also smart speakers, smart watches, TWS headsets, cars, smart TVs, etc. Since Amazon launched the smart speaker Echo system product, leading the development of the smart voice market, Google, JD, and Alibaba have all launched smart speakers built by their own voice assistants. According to product design and price positioning, a smart speaker can carry up to 2-8 MEMS microphones to form a microphone array. The shipment volume of MEMS microphones in smart speakers is at a compound annual growth rate of about 10%, which has become one of the space for the development of MEMS microphones.

At the same time, in addition to accelerating the development of micro-speakers, TWS headsets have also driven the market scale of MEMS microphones. With the release of Apple Airpods in 2016, it led the wave of TWS headsets. The subsequent release of Airpods2 voice wake-up function and AirPods Pro active noise reduction function has attracted attention. The number of MEMS microphones in each TWS headset has been increased to 2-3, that is, the number of MEMS microphones in each TWS headset reaches 4-6. According to the forecast of Memes Consulting, the compound annual growth rate of MEMS microphone shipments in TWS headsets is expected to be as high as 30% from 2021 to 2026.

Fierce compeititon in the optical lens business, WLG hybrid lens business is expected to become the focus

In terms of mobile phone camera modules, although the global mobile phone market shipments will decline year-on-year in 2020, the overall sales and performance of leading companies in the upstream of the industrial chain of mobile phone lens module manufacturers such as Sunny Optics, Qiuti Technology, and OFILM are generally Reverse growth. At present, there are not many companies that can supply three-camera and four-camera camera modules on a large scale, such as South Korea's LGinnotek, Japan's SHARP, OFILM and Sunny Optical. At the same time, even if smart phones have entered the stock market, the growth demand for mobile phone camera modules is still strong. The industry has also deployed advanced technology fields such as periscope lenses, TOF lenses, and 3D sensing lenses, forming high technical barriers in high-end products, resulting in the continuous increase of market share of leading companies. The market share of CR5 module manufacturers has increased from 2015 The 28% in 2018 rose to 41% in 2018. However, the total cost of mobile phone camera modules is relatively high and the gross profit margin is low. Moreover, there are many production companies and the market is relatively scattered. However, as industry companies suspended low-price competition, the gross profit margin of leading companies has increased significantly.

The current product price competition is fierce, and the competitive landscape is relatively mild for high-end products such as multi-camera, periscope, and 3D imaging. As the lens continues to upgrade, the technical requirements for module assembly will also increase, and the increase in value can also increase the pricing power of high-end products. Among them, the global shipments of smartphones equipped with periscope lenses were 15 million units in 2019. With the penetration of high-, mid-, and low-end phones, global shipments of smartphones equipped with periscope lenses have a chance in 2024. Over 400 million units.

In the optical lens industry, the barriers to mobile phone lens technology are high, and the competitive landscape is relatively concentrated, with CR5 at about 70%. The company needs to continue to meet the larger production capacity requirements and higher yields of mobile phone brands in order to maintain its market share, total profit and gross profit margin in the industry. As a leading company in the past, Largan's gross profit margin was as high as 60%-70%. However, due to the epidemic in 2020, the mobile phone lens industry has reduced the allocation and regulations, and its main customer Huawei has been affected by the Sino-US trade friction. Being able to maintain its technological advantage in the high-end market, Sunny Optical will come from behind; And Sunny Optical's gross profit margin remains between 40%-50%. On the other hand, since Taiwan's other major competitor Yujingguang made a breakthrough in equipment and machines in 2016, its yield rate has increased significantly, and its gross profit margin has also increased significantly from about 10% to about 40%, narrowing the distance with Largan and Sunny.

Global mobile phone lens market expands

In 2020, smartphone lens specifications will be downgraded, and global lens shipments will grow by only 3%, about 4.5 billion units. However, the growth momentum is expected to continue until 2021, and mobile phone lenses will exceed 5.07 billion units. The rate reached 11%. Although the mobile phone market has entered the stock market, shipments of mobile phone lens sets have maintained positive growth. The number of single-camera lenses has continuously increased from 2.2 in 2015 to 3.21 in 2019, and is expected to rise to 4.9 in 2024. The growth momentum of the number of mobile phone lenses mainly comes from the transition from front single-camera to dual-camera and the transition from low-end mobile phones to rear-mounted four-camera; Mobile phone manufacturers, such as Samsung and Huawei, have also begun to introduce high-end phones with five rear cameras. However, as the camera lens of the mobile phone increases, the thickness of the module will also increase, resulting in obvious camera protrusions on the back of the mobile phone, affecting the overall appearance of the mobile phone and going against the trend of thinner mobile phones. The configuration scheme of 6 cameras and above can only Penetration in high-end mobile phones is difficult to popularize.

On the other hand, due to the high-tech barriers in the high-end market, the mobile phone market will gradually slow down the upgrade of high-end mobile phone specifications. For example, Largan has already introduced 8P lenses into its customers` products, and although customers have begun to carry 9P lenses, but it is still in the optimization stage, and the technology is not yet fully mature; In addition, competitors such as Sunny Optics, AAC Technologies have successfully put into production 7P lenses, and some have also successfully developed 8P mobile phone lenses, putting more pricing pressure on Daguangli.

In the future, glass lenses and glass-plastic hybrid lenses will become a trend, because in order to achieve a breakthrough in the future sales of models, mobile phone brand manufacturers need new specifications of lenses to seek competitive advantages of performance differentiation, such as ultra-high pixels, ultra-large image surface, and ultra-large Aperture, ultra wide angle, ultra miniaturization, high zoom optical zoom, optical image stabilization, etc. improve user experience. This puts forward higher requirements for lens design height, stability, and resolution level. The performance of plastic lenses is close to the limit, and it has encountered bottlenecks in optical performance such as imaging clarity and distortion rate. The advantages of low dispersion, large light input, and thermal stability of the glass lens enable the glass-plastic hybrid lens to obtain greater lens design freedom, larger aperture and stronger resolution, breaking through the current bottleneck period of imaging technology.

Moreover, the addition of glass lenses can also effectively reduce the height of the lens, making the mobile phone lighter and thinner. However, the current glass-plastic hybrid lens involves a high technical threshold for the molding process and glass molding, and there are still few applications in mobile phones. There are four processes for preparing glass lenses, and the wafer-level glass technology (WLG) process is one of the directions that can be mass-produced. Compared with the traditional plastic lenses of mobile phones, WLG wafer-level glass lenses have a larger amount of light, which can effectively improve the picture quality, and the richness of the picture is greatly increased.

Electromagnetic drives

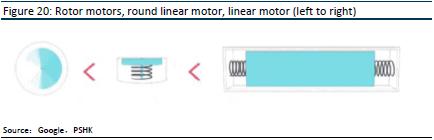

Mobile phone motors generally refer to small vibration motors applied to mobile phones, which mainly generate vibration effects through magnetic force and provide users with feedback during operation. At present, there are mainly two types of rotor motors and linear motors. Rotor motors use electromagnetic induction to drive the rotor to rotate and generate vibrations with a magnetic field caused by current. The principle of a linear motor is similar to that of a pile driver. It relies on a spring mass that moves in a linear form to directly convert electrical energy into a linear motion mechanical energy engine module, thereby generating vibration.

At present, most mobile phones on the market use a rotor motor as the source of mobile phone vibration, mainly because of its simple manufacturing process and low cost. But there are many limitations, such as slow start, slow braking, non-directional vibration, and difficult to control the volume and thickness. As mobile phones become thinner, rotor motors are gradually unable to meet the strict requirements of mobile phone space size.

In terms of linear motors, there are Z-axis haptics and XY-axis haptics. Under the principle of coordinates, the Z-axis represents the longitudinal direction, and the Z-axis linear motor is generally in the shape of a flat cylinder. Since the Z-axis haptics has a relatively small volume, its longitudinal stroke is relatively short. The XY-axis represents the horizontal direction, the XY-axis haptics is generally rectangular parallelepiped, the XY-axis haptics is a rectangular parallelepiped shape, its stroke is relatively long, and its vibration is stronger than the Z axis haptics. Since the design of iPhone 6s and iPhone Plus models, Apple began to equip them with a horizontal linear motor called "Taptic Engine". On the iPhone 7, the configuration is further improved to better simulate the real "home button" feedback. At present, more and more high-end flagship mobile phones choose to use horizontal linear motors. For example, the Haptic vibration motor of the OnePlus 7 Pro launched in 2019 is a horizontal linear motor.

Company Competitive Advantage

Started from acoustic devices, diversified business development

Before 2013, AAC Technologies had a relatively single business, mainly engaged in acoustic devices, and more than 80% of its revenue was in Dynamic components. In 2014, the company began to expand two new business segments, namely electromagnetic drive business and radio frequency and Micro-Electro-Mechanical System (MEMS). Then in 2015, AAC Technologies shifted its strategic positioning from "a global leader in micro-acoustic technology" to "a leading integrated micro-device technology company", and began to develop diversified businesses such as optics and precision structural parts.

Since the establishment of the company, the acoustic business has always been the company's main business. Currently, it uses dynamics components, including speakers, acoustic modules/micro speaker modules, receivers, etc. In 2018, the company made a breakthrough in the field of precision acoustics technology and began to launch the Super Linear Structure Solution (SLS). By innovating the traditional diaphragm design technology, this technology reduces the vibration of the diaphragm through the dual suspension structure, so that the effective amplitude of the sound diaphragm can be continuously increased, thereby bringing a fuller low frequency, higher volume, and clearer and more transparent sound quality performance. The user's auditory experience.

As of 2018, entry-level ultra-linear structure products have successfully penetrated into some Android flagship models. The launch of new super-linear structure products has obviously driven the increase in unit price. In October 2019, the third-party authoritative evaluation agency DXOMARK began to score the acoustic performance of smartphones. The flagship mobile phones using the company's classic SLS products received the highest scores, which will bring benefits to smartphone manufacturers, especially domestic manufacturers. More motivation for acoustic upgrades. The company studies to improve the acoustic performance and expand the upgrade path to release more versions of SLS products, such as ±0.75mm amplitude SLS products. Symmetrical dual-speaker stereo products will gradually cover the flagship and mid-to-high-end projects of each customer, and accelerate the expansion of in-vehicle, New markets such as smart speakers, AR, TWS wireless earphones and wearable fields.

In 2021, the company plans to launch a standardized small-cavity speaker module that will reduce the volume by 20-30% while maintaining a high level of sound quality to meet the trend of lighter and thinner mobile phones to further enhance the technical barriers of the industry. It is expected that by the end of 2021, the small cavity speaker module will account for 20%-30% of the group's Android acoustic shipments. Standardized products can effectively reduce the number of product models on the basis of increasing shipments. The use of platform-based and automated production methods can effectively improve capacity utilization and reduce cost losses caused by production line transformation, thereby optimizing the cost structure and improving the profitability of acoustics.

All in all, the continuous development of 5G mobile phones has put forward requirements for the lighter and thinner design of mobile phones. The smaller volume design of small cavity speaker modules will accelerate the market trend of 5G mobile phone stereo and multi-channel solutions. Stereo or multi-channel solutions increase the number of acoustic modules in a single mobile phone, thereby increasing the value of stand-alone acoustic products. At present, stereo has become the standard configuration of flagship mobile phones, and it is expected to gradually penetrate into low-end models in 2022. In the future, multi-channel is expected to be adapted to folding mobile phones and high-end tablets to achieve super bass and immersive sound field experience. At the same time, the group will also customize higher-end acoustic speaker modules with the R&D capabilities of the acoustic platform, integrated algorithm software and other R&D capabilities to provide consumers with a higher-end listening experience.

Taptic targets on Android customers

The company's main customer for haptic motors for a long time has been Apple manufacturers, accounting for 80-90% of its revenue, and shipments have remained stable. However, since 2018, the slowdown in innovation demand has intensified competition, which has led to the haptic motor business. Average unit price and output decreased, and overall revenue and gross profit margin decreased. In 2019, the company successfully produced the world's first smartphone horizontal vibration motor, and at the same time became the world's largest supplier of horizontal vibration motors. In 2020, the company's horizontal linear motors have been successfully promoted to mainstream Android flagship machines, and successfully imported into Android mid-range models, and Android motor shipments reached 20 million.

In the future, the company will continue to promote mid- and low-end linear motors to replace the current Z-direction circular motors on the market. At the same time, the company will promote it to applications such as automobiles, gamepads, and PCs, with the goal of achieving 300% growth. In terms of product development, the group innovated on the basis of applications, established in-depth cooperation with leading content and application vendors, formed a series of product matrices, broadened the moat, and developed high, medium, and low grade devices based on application experience. In 2021, the company expects to launch a variety of motor solutions, to provide customers with a full set of electromagnetic drive solutions of "algorithm + hardware", improve product viscosity, and open up a broader market.

Gross profit margin of plastic lens rise sharply, WLG lens technology expected to overtake in concers

In 2018, the company's optical business penetrated into major smartphone customers, and its revenue increased strongly to RMB 550 million, accounting for 3% of total revenue, a year-on-year increase of 240%. As of the end of 2018, the monthly production capacity of plastic lenses has reached 4kk pieces, and the monthly shipment volume has exceeded 2kk pieces. Until the fourth quarter of 2020, the market share of plastic lenses has steadily increased, and the monthly output of plastic lenses has reached the level of 7kk-8kk per month in the fourth quarter. Its gross profit margin has risen sharply from -2.7% in the second quarter of 2019 to 28% in the fourth quarter of 2020, and its gross profit margin in 2021 reached 36.3%, which is close to the gross profit margin of the leading company Sunny Optical in plastic lenses, mainly due to good products. Rate and management efficiency continue to improve. In terms of customer structure, the Group continued to make breakthroughs in high-end Android models, and entered the selection stage of some flagship phones. Overseas Android customers have also expanded smoothly, contributing to high-end plastic lenses.

The company has a decade-long R&D investment and strategic layout in the optical field, and in 2019, it has established the optical business as an important strategic direction in the future. The company's first wafer-level glass(WLG) lens design and manufacturing solution makes it possible to apply glass materials with better optical performance in the smartphone market on a large scale. Compared with the existing plastic lenses on the market, it has the advantages of larger aperture, more temperature resistance and lower thickness. It has more development potential under the general trend of miniaturization and resolution enhancement of optical components in the future. At present, WLG products have completed the development certification of 48M, 64M, 108M and Periscope G+P.

The company's first WLG project has been successfully shipped in the first quarter of 2021. The first mobile phone equipped with WLG glass-plastic hybrid lens has been promoted in the market. Compared with 6P lens, the light input is increased by 15%, the resolution is increased by 5%, and the overall lens height will drop by 5-10%. In addition, in terms of production technology, due to the completion of the Chongqing factory in 2020 and the plan to start mass production in the Czech factory in mid-2021, the production scale and efficiency of molding will be greatly increased, which will help improve the WLG glass-plastic hybrid lens project as delivery efficiency and cost optimization space brought by the scale effect. In addition, the development project of hybrid lens with more than 2 pieces of WLG glass is being actively promoted, and the amount of light input will continue to increase, providing strong support for the group's high-end optical lens.

MEMS microphones expand diversified markets

The company's main mobile phone customers for MEMS microphones are still Apple manufacturers, and the current shipments of MEMS microphones are relatively stable. In addition, the company broke the foreign technology monopoly for the first time in the field of 70dB high signal-to-noise ratio MEMS microphones and achieved national production. Achieve multiple breakthrough innovations in vibration mode design and power consumption. With the maturity of voice interaction technology and the popularization of wearable devices and smart home products in the non-smartphone field, the company successfully penetrated its products into IoT products through a distribution model. MEMS microphones have successfully entered the automotive market, realized the supply of leading auto companies, and continued to expand to TWS headsets, smart speakers, tablet computers and other categories, and will continue to increase market penetration.

In the first quarter of 2021, MEMS segment sales increased by 42.2% year-on-year to RMB 283 million due to the increase in market share, and the gross profit margin was stable at 16.7% year-on-year. The company expects to continue to increase its market share and maintain a high market share in the mobile phone business, continue to expand in the IoT, smart home, wearable devices, automotive and other markets. The company is currently a MEMS microphone supplier for a well-known brand of new energy vehicles . In addition, the TWS headset and notebook computer market has a need for upgrading products with higher signal-to-noise ratio, smaller size and lower power consumption. The penetration of the company's products into these markets will help increase the proportion of high-end products. It is expected that the overall MEMS microphones will be released in 2021. Cargo volume has achieved substantial growth year-on-year.

Financial forecast

The company's four major businesses: Dynamic components, electromagnetic drives and precision mechanics, optics products, MEMS components accounts for approximately 44%/ 40%/ 10%/ 6% of the total revenue in 2020 respectively. From the first quarter report, the reveneue is RMB 4.29 billion (+21% yoy). It is expected that the overall revenue will increase in the third and fourth quarters during the peak seasons of mobile phone nad other electronic product sales. To reverse the company's three consecutive years of decling revenue, it is predicted that the revenue in 2021/ 2022/ 2023 will be RMB 19.58/ 21.67/ 23.94 billion (+14% yoy in 2021). In terms of gross profit margin, the gross profit margin of the company's core business dynamic components has risen sharply from 28% in 2020, to 37.4% in the first quarter of 2021 (+11.4 ppts yoy, +9.4% mom); The gross profit margin of optical products also increased significantly from 19% to 27.8%; while electromagnetic drives and precision mechanics rose slightly from 24% to 25.5%. MEMS devices fell from 18% to 16.7% from 2020 to the first quarter of 2021. It is predicted that the company's overall gross profit margin in the future will keep it at about 31%.

In terms of acoustics, the compnay has been deploying on Android customers in recent years, and the revnue and gross profit increased in 2020 contributed by Android customers. From the revenue in the first quarter of 2021, hlaf of the company's segmental revenue is contributed by Android customers, and the gross profit is approximately 28%. In addition, the company has introduced “standardized small cavity speaker module” to improve versatility to be applicable to various Android phone modules. The number of speakers has been reduced from 300-400 models to about 100, which will help the company reduce R&D costs and scale. It is expected to account for 20%-30% of the total shipment volume in 2021. The company's goal is that “standardized small cavity speakers” will account for about 70%-80% of total shipments in the future. It is expected that the company will still have huge room for growth in the Android market in the future and its gross profit margin will also increase further.

In terms of electromagnetic drives and precision mechanics business, the company's current main customers in taptic is Apple which accounts for about 80%-90% of the segmental revenue. However, due to competition and low demand for upgrades for Apple, the company contunes to be under pressure on unit prices, while gorss profit margin margins remain stable. The company is currently graudally increaing the penetration rate of taptic on Android models. Through the design of taptic for Andriod customers, the unit price is lower than that of Apple, resulting in a smooth promotino. In 2020, the shipment volume of Android's taptic is about 20 million. The shipments to Android customers in the fourth quarter of 2020 and the first quarter of 2021 have both increased by about 60% mom. It is expected to maintain rapid growth throughout 2021, and its shipments may increase by 2-3 times, reaching more than 40 million units.

In the optical business, the compnay's monthly production capacity for plastic lenses is currently 6kk-7kk, and is expected to expand to 7kk-8kk in the third or fourth quarter of 2021. The company currentyl has 10 production lines for mobile phone lens modules, and aims to expand 25-30 production lines by the end of 2021. The module gross profit margin has also shifted from negative to approximately 10% in the fourth quarter of 2020.

In terms of expense ratio, the company is expected to continue to increase research and development expenses to maintain its competitiveness in the industry. It is estimated that the research expenses will be RMB 2.15/ 2.28/ 2.51 billion in 2021-2023, accounting for approximaely 11% of the total operating income.

Company valuation

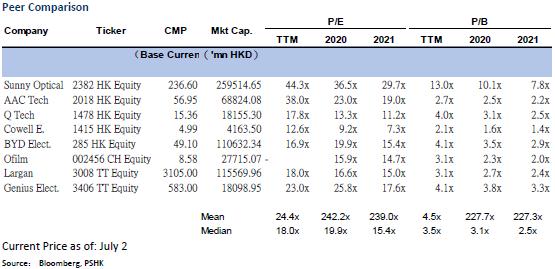

As of July 2, the closing price was 56.95HKD, the company's rolling price-earnings ratio was 37.91x. We predict that the company's earnings per share in 2021/ 2022/ 2023 will be RMB 2.14/ 2.52/ 2.84, and the CAGR from 2021-2023 will be 15.2%. Taking into account the company's leading position in the acoustics industry, expansion of the optical business, and the expected end of three consecutive years of negative growth in revenue and gross profit, the company is given an “accumulate” rating (first coverage). The 2021 target price given to the company is HK$64.3, which corresponds to a P/E ratio of 25x/ 21.26x/ 18.89x, corresponding to the EPS of 2021/ 2022/ 2023.

Risk factors

1) Epidemic

2) The sales of global mobile phone (typically 5G smartphone) is less than expected

3) The company's promotion in the Andriod market fell short of expectation

4) The compnay's progress in the opticsal business is slower than expectation

Financial

Click Here for PDF format...