Investment Summary

Gets Rid of the Negative Impact of the Pandemic in 2020 and Restores Growth in 2021

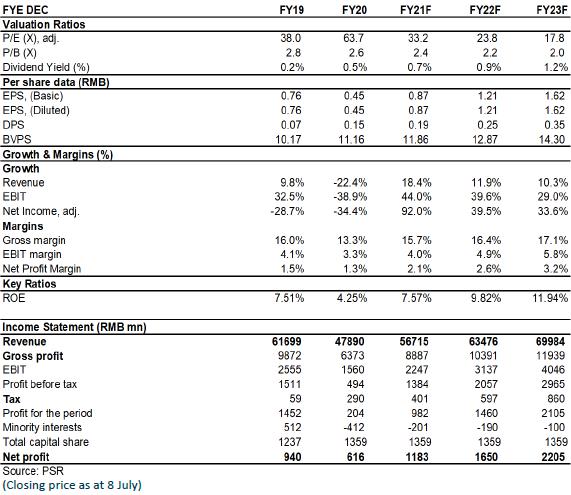

In 2020, Joyson Electronics reported operating revenue of RMB47.89 billion, down by 22.4% Y-o-Y. The net profit attributable to the parent company was RMB620 million, down by 34.5% Y-o-Y. The net profit attributable to the parent company excluding non-recurring items was RMB340 million, down by 66% Y-o-Y. Earnings per share was RMB0.45. Dividend per share was RMB0.15, with the dividend payout ratio of 31%.

The revenue saw a large decline in 2020, mainly because 1) the global business was impacted by the pandemic, and 2) the revenue of the joint venture Yanfeng KSS was moved off the balance sheet at the end of 2019. Excluding these factors, the Company's domestic business revenue increased slightly last year. Secondly, the non-recurring profits and losses mainly came from: 1) Non-recurring fixed expenses of RMB1.3 billion (pre-tax) due to the pandemic and non-operating expenses of RMB270 million (pre-tax) generated from Joyson Safety Systems` global integration, as well as 2) a pre-tax income of RMB1.82 billion generated from the sale of 51% equity in Joyson Quin, a subsidiary of Joyson Electronics, before the end of2020.

In the first quarter of 2021, Joyson Electronics recorded operating revenue of RMB12,287 million, a slight increase of 0.6% Y-o-Y. Excluding the impact of Joyson Quin's business being moved off the topline, its operating revenue increased by 7.5% Y-o-Y. The net profit attributable to the parent company was RMB221 million, a significant increase of 272.7% Y-o-Y. The net profit attributable to the parent company excluding non-recurring items was RMB241 million, down by 12.9% Y-o-Y. In addition to the low base caused by the pandemic last year, the main reason for the substantial increase in results in the first quarter was due to the fact that the integration effect of the Company's automotive safety business began to gradually release. There was a decline in the net profit after deduction of non-recurring profit or loss, mainly because the Company classified the fixed expenses of RMB220 million caused by the work stoppage due to the pandemic in the same period last year as non-recurring losses.

GM Improves Significantly QoQ, and Is Expected to Further Increase in the Future

In 2020, the overall gross margin decreased by 2.69 ppts Y-o-Y. In addition to the pandemic and the revenue of Yanfeng KSS being moved off the topline, 1.38 ppts was dragged down by the changes in accounting standards. Specifically, the gross margin of automotive safety, automotive electronics and functional parts, which are the major business sectors, decreased by 4.0 ppts, 2.1 ppts and 1.5 ppts, respectively. The gross margin of intelligent car networking increased by 6.1 ppts.

The gross margin in 2021Q1 was 15.4%, down by 2.0 ppts Y-o-Y. This was due to the increase in raw material prices during the current period and the inclusion of freight charges in operating costs under the new accounting standards. The gross margin climbed by 6.7 ppts Q-o-Q. The period expense ratio dropped by 3.5 ppts Y-o-Y, mainly because the financial expense ratio decreased by 1.6 ppts Y-o-Y. The main reasons were due to the decrease in interest expenses and the generation of exchange gains; the sales expense ratio decreased by 1.0 ppt Y-o-Y, because the freight charges were no longer included in the sales expenses under the new revenue recognition standards; the administration expense ratio declined by 0.7 ppts Y-o-Y, which was due to the decrease in the Company's restructuring and integration expenses. As the integration of the automotive safety department is gradually completed, it is expected that the subsequent integration expenses will be significantly reduced, and the profitability will improve.

New Orders Are Saturated, with Sound Business Climate

In 2020, the Company has won more than RMB59.6 billion worth of new orders for the whole year. Specifically, the new orders over the entire life cycle for the automotive safety systems business were approximately RMB37.5 billion. In particular, the number of new orders for domestic business has continued to remain high. The Company has continued to advance toward a goal of market share of 40%. For overseas business, although customers have postponed the outsourcing of some projects due to the coronavirus pandemic, it is expected that the above-mentioned new projects will be designated in 2021 consecutively. The Company will obtain more than USD8 billion worth of new orders for the automotive safety systems business. With the continuous improvement of safety regulations, the configuration rate of safety products will continue to increase in the future, especially the demand for the increase in the domestic market configuration rate will become more obvious. The safety products will become an important growth point in the future.

The new orders over the entire life cycle for the automotive electronics business were approximately RMB14 billion, maintaining good market competitiveness. Specifically, for new energy vehicle products, the Company has obtained new orders from Volvo in Europe, and orders for new models of Volkswagen's MEB platform in China. For the intelligent car networking business, the Company has moved from R&D to mass production, and received approximately RMB1 billion worth of new orders. Specifically, NIO's 5G-V2X platform project was designated, and the orders over the entire life cycle were approximately RMB660 million. The products include 5G-TBOX and 5G-VBOX for V2X.

In the first quarter of 2021, the Company sped up obtaining orders, with more than RMB20 billion worth of new orders over the entire life cycle. With the support of saturated orders, it is expected that the capacity utilisation rate will maintain a good level, and future results growth will be fully guaranteed.

In addition, Joyson Electronics has recently completed its strategic investment in Innovusion, a liDAR manufacturer. Joynext will join hands with Innovusion to provide ultra-long-distance high-precision liDAR to NIO. In the future, both parties will also conduct cooperation in liDAR perception fusion, V2X data fusion, and domain controllers. In the second half of 2020, Joynext has introduced several external investors to increase capital by RMB720 million, and introduced measures such as executive share incentives, laying a solid foundation for further development at the capital level.

Intellectualization and new energy remains the theme of the entire industry. In the future, the Company will focus more on forward-looking directions such as active and passive safety, automatic driving, car networking, and smart cockpits, and increase input in liDAR, domain controllers, 5G-V2X, and new energy vehicle electronic control and management technology. In addition, it will establish a new global R&D center in Shanghai, accelerate product arrangement and market expansion, and promote further business upgrade..

Investment Thesis

Although the domestic car market will be affected by the chip shortage, we are optimistic about the firm leading position of the Company and the broad development space for new businesses. By the way, the Company expressed its intention to list the above-mentioned automotive electronics businesses to support further development of new businesses.

We revised the target price of RMB 34 equivalent to 39/28/21x P/E and 2.9/2.6/2.4x P/B of 2021/2022/2023, and assign Accumulate ratings. (Closing price as at 8 July)

Risk

Operating collision in Joyson's M&A

Worse-than-expected downstream demand

Financials

Click Here for PDF format...