Investment Summary

Q Technology (1478.HK) was found in 2007 and was listed on the main board of the Hong Kong Stock Exchange in 2014. The company is a global leading mid-to-high end camera and fingerprint recognition module manufacturer for intelligent mobile terminals, such as global smart phones and table PC brands, Internet of Things (IoT), smart vehicles, etc. The company is one of the first few manufacturers in the PRC to use chip on board (COB) and chip on flex (COF) technologies and molding on board (MOB) and molding on chip (MOC) technologies in the manufacture of camera modules. At present, the company continues to focus on mid-to-high end camera module products, and its main customers are Vivo, OPPO, Huawei and Xiaomi.

Improved on the product structure of mobile phone camera

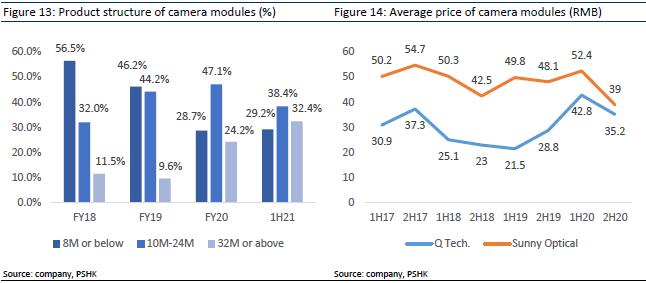

The company aims to continue to improve the mid-to-high-end product structure while increasing the average unit price to catch up with the performance of the leading company Sunny Optical. In 2020, the company's shipments of 32 million pixels and above camera modules accounted for 24.2% of the company's total shipments (+14.6 ppts yoy). The camera modules with 10 to 24 million pixels rose steadily, accounting for 47.1% in 2020 (+2.9 ppts yoy). The proportion of lower-end camera modules with 8 million pixels and below dropped from 46.2% in 2019 to 28.7% in 2020 (-17.5 ppts yoy). The company's goal is that by 2021, 32 million pixel and above cameras will account for no less than 30% of shipments. According to the shipment volume performance in the first half of 2021, the proportion of 32 million pixel and above cameras accounts for 32% and the goal is expected to achieve.

In the first half of 2020, the company's average unit price of camera modules reached RMB 42.8, but in the second half of 2020, its unit price dropped to RMB 35.2. The main reason was the decline in sales of Huawei's high-end mobile phones as the trade friction between China and United States. As a result, the company's shipments of high-end camera modules have been affected. In the short term, because Huawei's high-end products account for a certain proportion of the company and are irreplaceable, sales of Huawei's mobile phones have also fallen. Therefore, it is predicted that with the increase in the penetration rate of mid-and high-end products in 2021, the average unit price will slightly increase in the second half of 2021. In the long run, with the upgrading of high-end camera module specifications and the acceleration of penetration rate, and the application of 3D modules, automotive and IoT camera modules, it is predicted that the overall average unit price will still have room for increase.

Financial forecast and company valuation

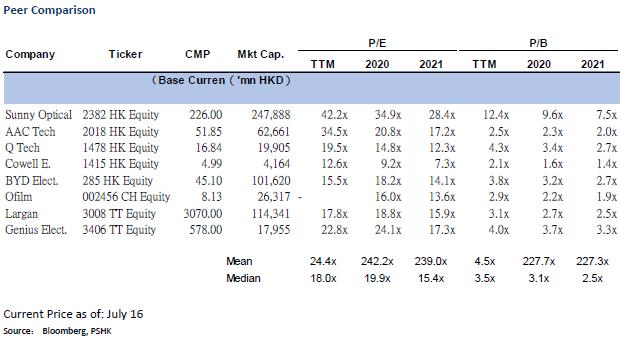

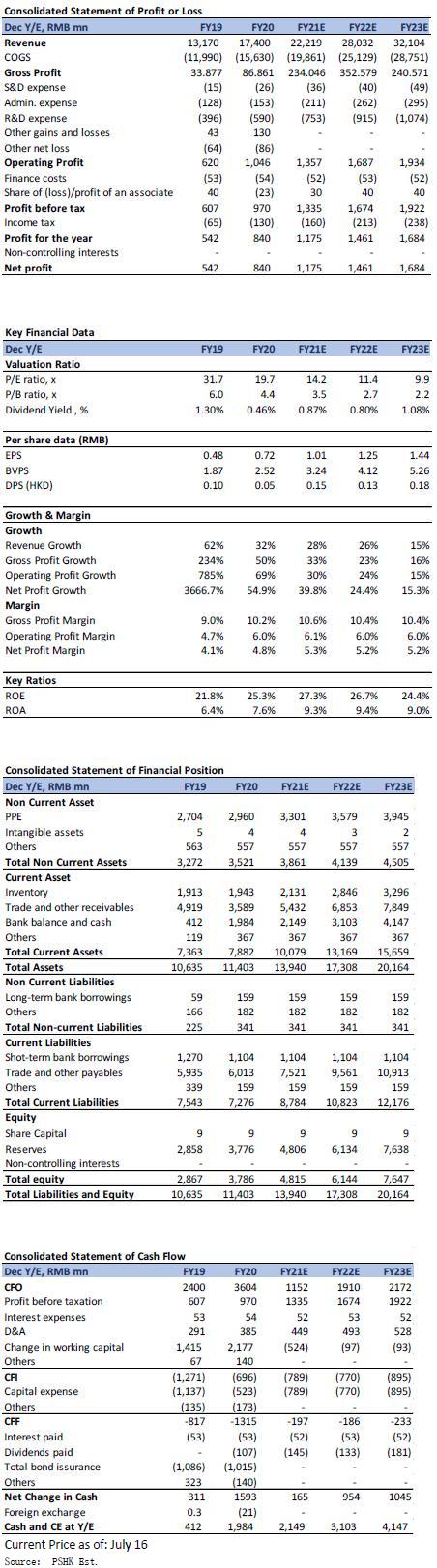

As of July 16, the closing price was 16.84, the company's rolling price-earnings ratio was 19.51x. We predict that the company's earnings per share in 2021/ 2022/ 2023 will be RMB 1.01/ 1.25/ 1.44, and the CAGR from 2021-2023 will be 19.4%. Considering that the company occupies a certain position in the camera module industry, the demand for camera modules in mobile phones, automobiles, and IoT has increased, and the company has begun to diversify its layout. The company is given an “accumulate” rating (first coverage). The 2021 target price given to the company is HK$20.12, which corresponds to a P/E ratio of 17.0x/ 13.7x/ 11.9x, corresponding to the EPS of 2021/ 2022/ 2023.

Risk factors

Epidemic, the sales of global mobile phone (typically 5G smartphone) is less than expected, the compnay's progress in the opticsal business is slower than expectation

Company Profile

Q Technology (1478.HK) was found in 2007 and was listed on the main board of the Hong Kong Stock Exchange in 2014. The company is a global leading mid-to-high end camera and fingerprint recognition module manufacturer for intelligent mobile terminals. The company is primarily engaged in the design, research and development, manufacture and sales of camera modules and fingerprint recognition modules, and centred on mid-to-high end market for intelligent mobile terminals, such as global smart phones and table PC brands, Internet of Things (IoT), smart vehicles, etc. The company is one of the first few manufacturers in the PRC to use chip on board (COB) and chip on flex (COF) technologies and molding on board (MOB) and molding on chip (MOC) technologies in the manufacture of camera modules. At present, the company continues to focus on mid-to-high end camera module products, and its main customers are Vivo, OPPO, Huawei and Xiaomi.

Company Development Process

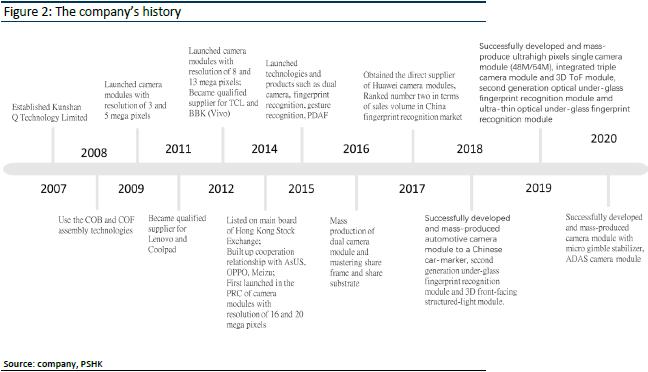

Mr. He Ningning, currently the chairman of the Board, established Kunshan Q Technology Limited. In 2008, the company started to use the COB and COF assembly technologies. The company launched camera modules with resolution of 3 mega pixels and 5 mega pixels in 2009 and launched camera modules with resolution of 8 and 13 mega pixels in 2012. In 2014, the company first launched in the PRC of camera modules with resolution of 16 mega pixels and 20 mega pixels and started mass process and sales of camera module with OIS (optical image stabilization) function. In 2015, the company launched technologies and products for dual camera, fingerprint recognition, gesture recognition, PDAF (phase detection auto-focus). In 2016, it produced fingerprint recognition module and mastering the two major manufacturing know-how including cover-type and coating-type massively. In 2017, the company has a strong growth in fingerprint recognition business and ranked number two in terms of sales volume in China market. Besides, it invested in Newmax Technology Co., Ltd (3630.TW), hold 36% of stake and become the single largest shareholder, facilitate a faster vertical integration of supply chain. In 2018, the company successfully developed and mass-produced the automotive camera module to a Chinese carmaker module to a Chinese carmaker as well as second generation under-glass fingerprint recognition module and 3D front-facing structured-light module. In 2020, the company successfully mass-produced automotive-grade advanced driver assistance system (ADAS) camera module.

Operating condition

In 2020, despite the impact of the global epidemic and the negative impact of smartphone sales, the company successfully continued its growth momentum in 2019, achieved new highs in sales revenue and net profit, and achieved new highs in sales revenue and net profit. The company has achieved three strategic goals: 1) The product structure and unit price of camera modules increased significantly yoy, strengthening the market position of the company as one of the Tier 1 manufacturers of camera modules, 2) more balanced and comprehensive coverage of major mobile phone brand customers adopting Android system at home and abroad, 3) the continuous improvement of layout of non-handset business such as automotive camera modules and internet of Thing (IoT) product camera modules and the successive mass production and sales, paving way for long-term growth. However, as affected by factors including the pandemic, the company failed to achieve the sales volume and production expansion targets of camera modules set at the beginning of the year.

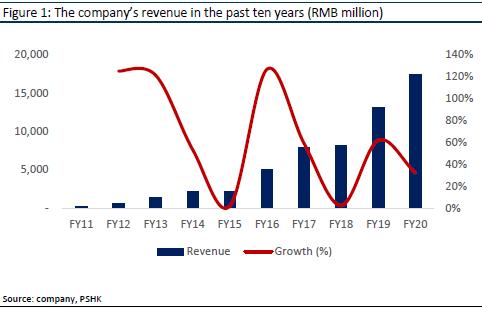

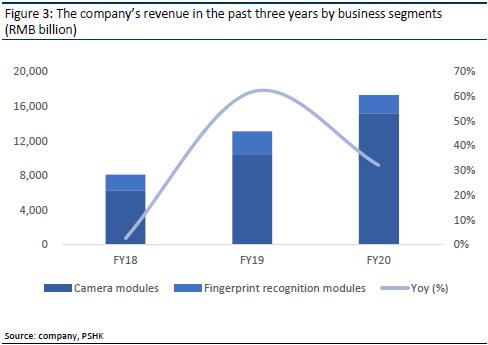

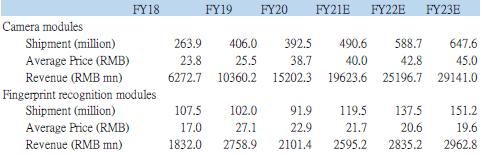

The company's sales revenue in 2002 was RMB 17.4 billion (+32% yoy). In 2018/2019, sales revenue was 8/13.2 billion (+2%/ 62% yoy) and the CAGR for the period 2018-2020 was 46%. The company is currently divided into two major businesses: 1) camera modules and 2) fingerprint biometric devices. The revenue in 2020 will account for approximately 87%/ 12%. Among them, camera modules are the company's main revenue products. In 2018/ 2019/ 2020, the company's camera modules will be approximately RMB 6.3/ 10.4/ 15.2 billion (-34%/ 65%/ 47% yoy respectively). The CAGR for the period 2018-2020 is 55%. In terms of fingerprint recognition modules, the company's revenue in 2018/ 2019/ 2020 was approximately RMB 18/ 28/2.1 billion (-10%/ 51%/ -24% yoy respectively) and the CAGR for the period 2018-2020 was 7%.

In 2020, affected by epidemic, global smartphone shipments have fallen. The sales volume of the company's camera modules has fallen less than that of smartphone terminals. There are three main reasons: 1) The increase in the proportion of handsets with tri-camera and quad-camera design, resulting in the continuous increase in the average number of camera modules assembled by each smartphone, 2) increase in market share of high-end camera modules, 3) continuous optimization of customer structure. In terms of fingerprint recognition module products, stagnant shipment of smartphones had a relatively bigger impact. There are four main reasons: 1) each mobile phone is usually equipped with only one fingerprint recognition module, leading to a highly correlated shipping volume of both products, 2) under-glass fingerprint recognition module is more widely adopted by high-end smartphones, the weakness of sales of which indirectly caused the product mix enhancement of fingerprint recognition module products slowdown, 3) the delayed the specification upgrade of fingerprint recognition modules, and the launch of certain new products such as ultra-thin fingerprint recognition modules and large-size fingerprint recognition modules was delayed, 4) the increase in competition for sensing chips, which led to a decrease in material costs and lowered the overall product selling price.

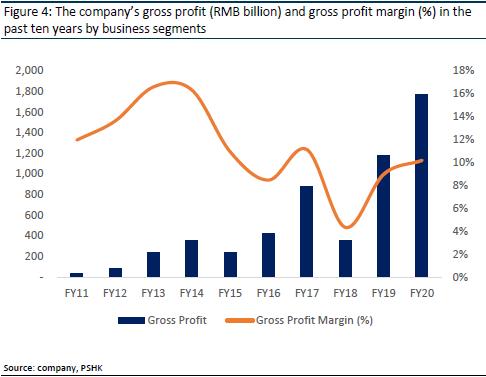

In terms of gross profit, the company's gross profit in 2020 is RMB 1.7 billion(+50% yoy). The 2018/2019 gross profit was RMB 0.35/ 1.2 billion (-60%/ 234% yoy respectively). In terms of gross profit margin, the company's 2018/2019/ 2020 are 4%/ 9%/ 10% respectively. The main reason why the company's gross profit margin has risen steadily is 1) the significant optimization of the product mix of camera modules helped to enhance the added value of camera module business, 2) the intensified effectiveness of production line upgrading and reformation through automated and digitized production as well as the reducing demand for production staff with the same production capacity.

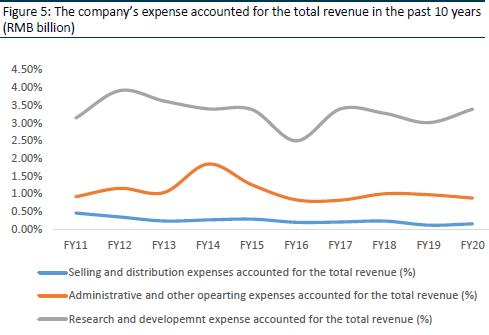

In terms of expense ratio, the company's main expenses are research and development expenses which is RMB 500 million (+49% yoy), accounting for 3.4% of the company's total revenue. The company has maintained a stable level of 3% -3.5% over the past 10 years. It can be used to upgrade and transform new products, processes, and automation.

Industry Analysis

Global smartphone shipments recover and enter integrative market

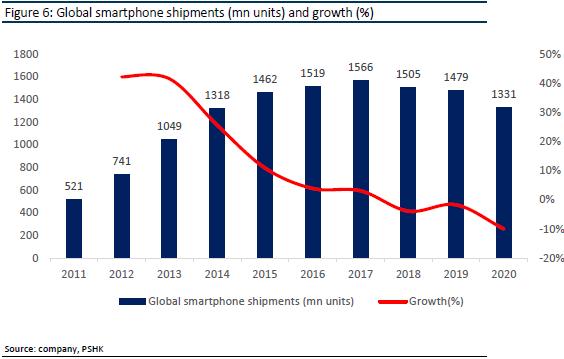

In 2020, due to the epidemic, the shortage of components such as chips, and the slowdown in consumer demand for new equipment, the pattern of the smartphone market has changed. The poor performance of the smartphone terminal market, restricted sales channels, and tight supply chain production have led to a decline in overall smartphone shipments. Besides, the global mobile phone equipment configuration has been downgraded, and the 5G replacement wave has slowed down. Accounting to the data released by Counterpoint, a market research organization, global smartphone shipments will be 1.33 billion units in 2020, (-10% yoy). Subsequently, market research agency Canalys announced that global smartphone shipments in the first quarter of 2021 were 347 million units, (+24% yoy). In the first quarter of the world's shipments, Samsung is still the world's largest smartphone seller, with shipments of 76.5 million units and a market share of about 22%. China's top three mobile phone manufacturers (Xiaomi, OPPO, Vivo) have a market share of 37%; Apple's mobile phone shipments are the second, reaching 52.4 million units, accounting for 15% of the total shipments, compared with 37.1 million units shipped in 2019 (+41% yoy).

Accounting to the authoritative release of CAICT, China's smartphone market has shown a clear recovery, from Jan-May 2021, the total mobile phone shipments in the domestic mobile phone market totaled 148 million units (+7% yoy). Moreover, domestic 5G mobile phone shipments accounted for the increase in total smartphone shipments, reaching 108 million units (+134.4% yoy). The rapid growth in the number of 5G users is a major factor in promoting equipment replacement. As of the end of the first quarter of 2021, 5G users have exceeded 350 million, and operators are also accelerating the migration of 4G users to 5G: operators reduce 4G packages and switch to new users or old users provide 5G packages, so it is expected that when most consumers in China change their devices, 5G smartphones will become the best choice. According to the Ericsson Mobile Trends Report, it is estimated that there will be 3.5 billion 5G users by the end of 2026, accounting for more than 50% of mobile data.

Global Handset Lens sets (HLS) market expands

In 2020, the specifications of HLS has downgraded, and the global HLS has grown by only 3%, about 4.5 billion units. However, the growth momentum is expected to continue in 2021, and HLS will exceed 5.07 billion units (+11% yoy). Although the mobile phone market has entered the stock market, shipments of HLS has maintained growth. The number of the single-camera lens has continuously increased from 2.2 in 2015 to 3.21 in 2019 and is expected to rise to 4.9 in 2024. The growth momentum of the number of HLS mainly comes from the transition from single front camera to dual camera and the transition from low-end mobile phones to rear four cameras. Mobile phone manufacturers, such as Samsung and Huawei, have also begun to introduce high-end phones with five rear cameras. However, as the camera lens of the mobile phone increases, the thickness of the module will also increase, resulting in obvious camera protrusions on the back of the mobile phone. This will affect the overall appearance of the mobile phone and going against the trend of thinner mobile phones. The configuration scheme of 6 cameras and above can only penetrate in high-end mobile phones market which is difficult to popularize.

In the high-end mobile phone market, due to the high-tech barriers, the upgrade speed of the high-end mobile phones will gradually slow down. For example, Largan has already introduced 8P lenses in its customers` products and further, although some products have begun to carry 9P lenses, it is still in the optimization stage and the technology is not yet fully mature. In addition, competitors such as Sunny Optical, AAC Technologies and Ofilm Group have successfully put into production 7P lenses, and some have also successfully developed 8P lenses, which puts Largan under pricing pressure. To achieve a breakthrough in the future sales of models, smartphone brand manufacturers have to look for cameras with new specifications to increase competitive advantage via differentiated performance, such as ultra-high resolution, ultra- large image size, ultra-large aperture, ultra-wide angle, ultra-miniaturization, high time optical zoom, optical image stabilization in a bid to improve user experiences.

In conclusion, the growth of the market size of HLS is mainly affected by two factors: 1) the increase in sales of HLS, 2) the increase in unit price. In the case of downgraded specification of smartphone cameras presented, this is conducive to the expansion of mid-to-low-end manufacturers, leading to oversupply and the overall average selling price (ASP) of HLS has fallen. However, with the restart and upgrade of HLS in 2021 and the expected 5G replacement wave, the increase in the proportion of high-end products in the future is expected to hedge the impact of price wars on low-end products. It is expected that the ASP of HLS will gradually stabilize.

Camera Modules Industry

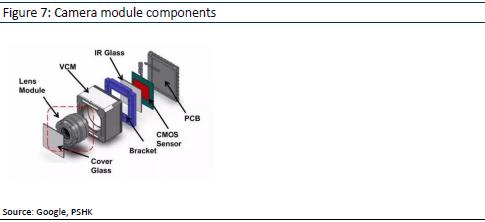

The components of the mobile phone camera mainly include optical lens, voice coil motor and CMOS image sensor etc. Among them, CMOS image sensors account for the highest cost among mobile phone cameras for 45.2%. For module packaging, it refers to the assembly of lens, CMOS image sensors and other components into a camera module, and the cost of camera module accounts for 25.7%.

Market fragmentation, leading companies seize high-end market share

Although shipments of the global mobile phone market are declining year-on-year in 2020, the overall sales and performance of the leading companies in the upstream of the industry chain, such as Sunny Optical, Q Tech, Ofilm Group have generally reversed growth. At present, there are not many companies that can supply three-camera and four-camera modules on a large scale, such as South Korea's LGinnotek, Japan's Sharp, Ofilm and Sunny Optical. At the same time, even if smartphones have entered the stock market, the growth of the demand for camera module is still strong. The industry has also deployed advanced technology fields, such as periscope lenses, TOF lenses, and 3D sensing lenses, forming high technical barriers in high-end products, resulting in the continuous increase of the market share of leading companies. The market share of CR5 of HCM has increased from 28% in 2015 to 41% in 2018. However, the total cost of HCM is relatively high and the gross profit margin is low. Moreover, there are many production companies, and the market is relatively scattered. As industry companies suspended low-price competition, the gross profit margin of leading companies has increased significantly. Looking back at the camera module development, 2015-2016 is the initial stage of multi-camera technology in mobile devices, from a single camera to a dual camera. Then it developed to three cameras in 2018-2019 and developed to four cameras in 2020. According to data released by Yole, the total revenue of global camera modules in 2019 was 31.3 billion US dollars. The total revenue in 2015 is predicted to be 57 billion US dollars, and the CAGR for 2019-2025 is 10.5%. In 2019, the global shipment of camera modules was 5.5 billion and it is predicted to reach 8.9 billion by 2025.

From the perspective of customer layout, Sunny Optical occupies mainly the demanding Android market, typically the high-end market and continues to increase its share of Samsung mobile phones, which currently account for the highest share of global mobile phone. The return on investment is expected to be higher than that of the Apple industry. Q Tech mainly occupies the low-end Android market. Through technological improvement, it continued to expand in recent years, including Vivo, OPPO, Xiaomi and Huawei.

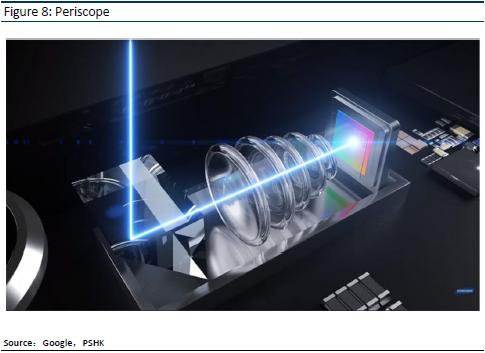

The current product price competition is fierce, and the competitive landscape is relatively mild for high-end products such as multi-camera, periscope modules, 3D imaging. As the lens continues to upgrade, the technical requirements for module assembly will also increase, and the increase in value can also increase the bargaining power of high-end products. Among them, the global shipments of smartphones equipped with periscope lenses were 15 million units in 2019. With the penetration of high-, mid- and low-end phones, global shipments of smartphones equipped with periscope lenses could exceed 400 million units in 2024.

In addition, 3D sensor camera technology can realize multiple functions such as face recognition, gesture recognition, three-dimensional measurement and environmental perception, and is widely used in mobile phones, drones, robots, AR, VR, security, car driving assistance and other fields. Among them, the 3D structured light technology uses infrared lasers to project light with certain structural characteristics onto the object to be photographed, and then collect it by a special infrared camera to obtain a three-dimensional structure. The time of flight (TOF) is to send processed pulsed infrared light through the sensor, which will be reflected when it hits an object. By capturing the round-trip time, the distance between the objects can be calculated.

Fingerprint recognition module Industry

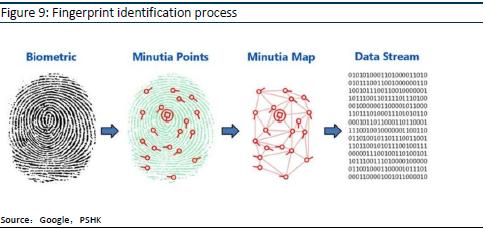

Fingerprint identification technology is a reliable biometric identification technology. By comparing its fingerprint with a pre-saved fingerprint, its identity can be verified. Because every person (including fingerprints) has different skin patterns, breakpoints, and intersections, and they are unique. Therefore, relying on this uniqueness and stability, fingerprint identification technology can be applied. The process of fingerprint identification technology generally includes fingerprint image collection, fingerprint image processing and minutia matching.

Popularization of under-glass fingerprint recognition technology

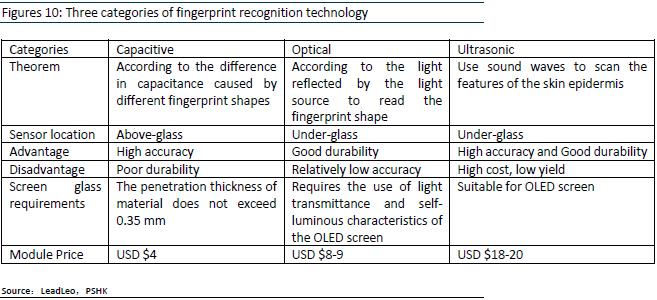

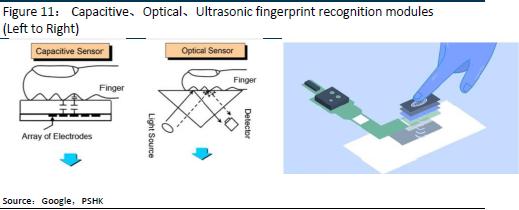

At present, fingerprint recognition technology can be divided into three categories: capacitive fingerprint recognition modules, optical under-glass fingerprint recognition modules and ultrasonic fingerprint recognition. Among the three technologies, the most mature and traditional technology is capacitive fingerprint recognition. It uses silicon wafers and conductive subcutaneous electrolyte to form an electric field. The fluctuations of fingerprints will cause different changes in the pressure difference between the two to achieve accurate fingerprint determination and there are no special requirements for the use of environment. At the same time, it is still the main fingerprint recognition solution for low-end models of smartphones.

The optical under-glass fingerprint recognition modules use the principle of light refraction and reflection identify the user's fingerprint, which is suitable for under-glass fingerprints. However, this technology has certain requirements for the temperature and humidity of the use environment. In terms of ultrasonic fingerprint recognition, a signal is transmitted through a radio frequency sensor, which penetrates the epidermis of the finger. It uses the difference of fingerprints to reflect the ultrasound to build 3D images to obtain information. Compared with the other two technologies, the RF sensor has lower requirements for the finger cleanliness and can unlock with wet hands. However, due to the need to actively transmit signals, the power consumption is relatively high compared to the capacitive type, and its cost is relatively high. Currently, optical screens and ultrasonic fingerprint recognition technology can be applied for under-glass fingerprints modules.

With the popularization of the concept of full-screen mobile phones, mainstream mobile phone vendors in the market can also use under-glass fingerprint recognition technology to complete fingerprint recognition and unlocking under the screen glass. Since 2013, the iPhone 5S adopted the push-type capacitive fingerprint recognition technology, which has driven the demand for smartphone fingerprint recognition, and the current capacitive fingerprint recognition market is becoming saturated. In 2018, the under-glass optical fingerprint recognition chip was commercialized, and Vivo X21 became the first mobile phone brand to launch under-glass fingerprint recognition. Optical fingerprint technology continues to be iteratively upgraded. In 2019, Xiaomi launched the CC9 series of ultra-thin solutions, and optical fingerprint unlocking gradually became the mainstream of the market. In 2020, Samsung released its flagship model Samsung S10, equipped with ultrasonic fingerprint technology, occupying the technological high ground. However, due to the difficulty of research and development of ultrasonic fingerprint recognition chips, currently the ultrasonic fingerprint technology is difficult to commercialize and mass produce.

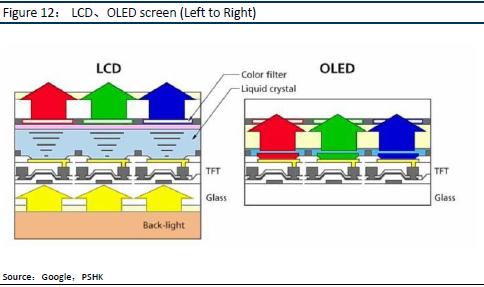

According to the China Internet Data Information Network, the under-glass fingerprint in China market (calculated based on the shipments of under-glass fingerprint mobile phones) has grown from 3.907 million units in 2015 to 60.567 million units in 2019. The CAGR for 2015 -2019 was 98.4%. The main reasons are 1) OLED screens may become the mainstream of mobile phone screens in the future. At present, the penetration rate of OLED screens in China is less than 50%, and there is still a lot of room for growth. The development of OLED screens will further drive the market for fingerprints under optical screens, 2) The trend of full-screen mobile phones. At present, the fingerprint recognition module under the screen is mainly used in conjunction with the OLED screen, because the OLED screen can be self-luminous, thin panel with good light transmission and can be folded. In terms of traditional LCD screen, its light-emitting principle mainly relies on the backlight layer, plus the existence of the backlight layer and the liquid crystal layer. Therefore, it is relatively thick. The backlight will easily interfere with the optical fingerprint recognition, and the light transmittance of the LCD is not good. Using the fingerprint under the optical screen under the LCD screen will cause the accuracy to decrease. In 2020, Xiaomi announced that it has developed the fingerprint technology under the LCD screen, but there is still no mass production model released.

Company Competitive Advantage

Balanced and comprehensive coverage of domestic and overseas Android mobile phone brand customers

Q Technology has been focusing on the camera module business since 2007, and has accumulated various first-line mobile terminal brands over the years. At present, the company's main customers include Vivo, Oppo, Huawei and Xiaomi while Vivo and OPPO are the company's largest customers, accounting for about 60% of the company's shipments. The overseas Samsung mobile phone manufacturers are the company's new customers in mid 2020, and currently only account for a low single-digit percentage of the company's total shipments. The company will benefit with the expand of the overall market rate of mobile phone vendors of Chinese customers.

Improved on the product structure of mobile phone camera

The company aims to continue to improve the mid-to-high-end product structure while increasing the average unit price to catch up with the performance of the leading company Sunny Optical. In 2020, the company's shipments of 32 million pixels and above camera modules accounted for 24.2% of the company's total shipments (+14.6 ppts yoy). The camera modules with 10 to 24 million pixels rose steadily, accounting for 47.1% in 2020 (+2.9 ppts yoy). The proportion of lower-end camera modules with 8 million pixels and below dropped from 46.2% in 2019 to 28.7% in 2020 (-17.5 ppts yoy). The company's goal is that by 2021, 32 million pixel and above cameras will account for no less than 30% of shipments. According to the shipment volume performance in the first half of 2021, the proportion of 32 million pixel and above cameras accounts for 32% and the goal is expected to achieve.

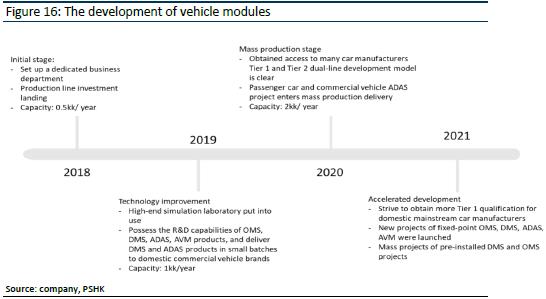

At present, the company's camera modules with 32 million pixels and above include not only mobile phone single-camera modules, dual/ multi-camera modules, and 3D modules, but also automotive cameras and IoT modules. However, the current shipments of automotive cameras modules account for less than 1% of the company's total shipments of camera modules. It is predicted that it will increase to 1-2% in 2021, and 2023 will account for 3-5% of the total shipments.

In the first half of 2020, the company's average unit price of camera modules reached RMB 42.8, but in the second half of 2020, its unit price dropped to RMB 35.2. The main reason was the decline in sales of Huawei's high-end mobile phones as the trade friction between China and United States. As a result, the company's shipments of high-end camera modules have been affected. In the short term, because Huawei's high-end products account for a certain proportion of the company and are irreplaceable, sales of Huawei's mobile phones have also fallen. Therefore, it is predicted that with the increase in the penetration rate of mid-range products in 2021 and the proportion of high-end products to remain as of the proportion in the second half of 2020, the average unit price will slightly increase in 2021. In the long run, with the upgrading of high-end camera module specifications and the acceleration of penetration rate, and the application of 3D modules, automotive and IoT camera modules, it is predicted that the overall average unit price will still have room for increase.

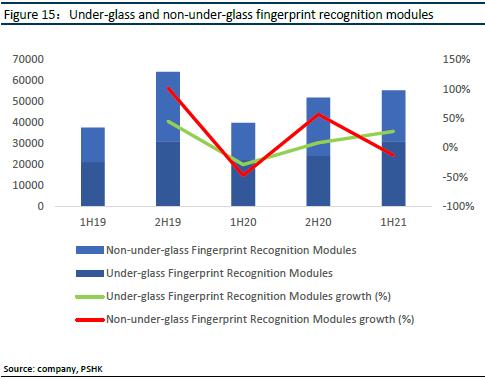

Under-glass fingerprint recognition modules continue to grow

The company started to produce fingerprint modules in 2015 and has announced the shipments of its under-glass and non-under-glass fingerprint recognition modules since March 2019. The under-glass fingerprint products are innovated, and the fixed-position optical under-glass fingerprint + ultra-thin solution will be launched in 2019. In 2020, large-area/ half-screen optical fingerprints and LCD optical fingerprints will be launched. With the development of full screens, it is expected that Android phones will gradually reduce non-screen fingerprint recognition modules (capacitive fingerprint modules), while under-screen fingerprint products will increase, and their shipments will continue to pick up since the second half of 2020. The under-screen fingerprint products are expected to continue to develop in the future. The technical development direction is mainly AMOLED optical under-glass half-screen fingerprints and LCD optical under-glass fingerprints. The company is expected to benefit from the continuous upgrade of under-glass fingerprint products.

Accelerated the development of emerging businesses

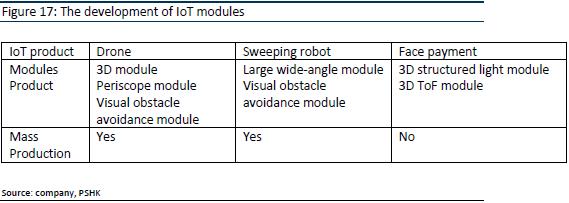

The company has been committed to developing emerging businesses, including smart mobile terminal customer services for automobiles, smart homes and other IoT application scenarios. The company launched its automotive camera module products for the first time since the second quarter of 2018, obtained the Tier 1 or Tier 2 supplier qualifications for various well-known domestic automobile brands within less than two years, as well as successfully commenced the mass production of advanced driver assistance system (ADAS) and intelligent cabin (In-Cabin) camera module products. At present, the camera module projects of more than ten automobile models have entered the stage of product R&S and certification, striving to achieve mass production in 2021. At the same time, the company began to make mass production of IoT products such as sweeping robots camera modules and drones camera modules for the Year, covering leading customers in the relevant industry, entered into the camera module market of wearable devices, including smart watch products, and continued to expand in non-handset industry fields.

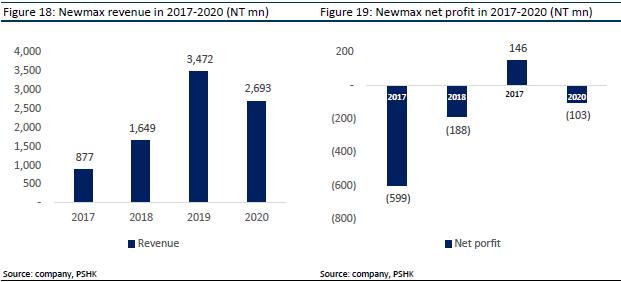

Apollo Project – Vertical integration

The company has been vertically integrating the core components of intelligent vision to provide customers with products at the best prices, which facilitates the time for customer supply chain management and enhances customer experience. In 2017, the company invested in Newmax Technology, a listed company in Taiwan, stock code: 3630, to strengthen resource integration in the field of high-resolution RGB lenses. After two years of resource integration and technology sharing, Newmax technology turned losses into profits, with revenue of NT $3.4 billion (+110%), and net profit of NT $500 million in 2019. In addition, to support the further expansion of operating scale of Newmax Technology and improve its operating results, the company actively participated in the action of capital injection and shareholding expansion of Newmax Technology during the year which successfully raised a fund of approximately NT $2.07 billion for Newmax Technology, providing capital reserve for the expansion of production base of Newmas Technology and enhancement of its research and development capability and thereby laying a solid foundation for the continuous and sound development of Newmax Technology. However, in the first half of 2020, Newmax Technology was hit by the suspension of production due to the pandemic, recording a net loss attributable to shareholders of approximately NT $190 million. With the hard works in the second half of 2020, the results improved significantly and the sales revenue increased by approximately 40.1% hoh. The net loss attributable to shareholders in 2020 was NT $280 million.

Besides, the core competitiveness of Newmax Technology, such as customer base, technical capabilities and production capacity scale continued to improve. In the second half of the Year, the company made a breakthrough in the expansionof the high-resolution RGB lens business, including successfully obtained the supplier qualification of two famous mobile phone brand customers using Android system, and gradually secured more projects of the handset RGB lens of 5P or above. In addition, the construction of the new plant in the central science park of Taichung was progressing satisfactorily. It is expected that the civil construction and decoration works will be completed by mid-2021, and the production capacity of lens sets will be expanded to a relatively larger scale according to customer needs. After the technology accumulation and customer structure optimization in 2020, it will expectantly enter a new stage of sales expansion.

Spin-off subsidiary listed on A shares to create a dual capital platform

The company announced in June 2021 that Kunshan Q Technology China had submitted a proposed listing application to the Shenzhen Stock Exchange's GEM. Before submitting the proposed listing application, Kunshan Q Technology had a registered capital of RMB 2.89 billion. Currently, Kunshan Q Technology China is an indirect wholly owned subsidiary of Q Technology. It is expected that Kunshan Q Technology China will remain a subsidiary of the company after the completion of the listing. The long-term goals of this listed capital restructuring: 1) Expand the scale of mobile phone camera modules, 2) Accelerate the development of vehicle and IoT module business, 3) Long-term strengthen the integration of key device resources.

Financial forecast

The company's two major businesses are camera modules and fingerprint recognition modules accounted for 87% and 23% of the company's total revenue, respectively. On July 16, the company has announced the positive profit alert and it is expected that the consolidate profit attributable to the Shareholders of the Group for the six months ended 30 June 2021 may increase by approximately 40% to 60% as compared to the that ended 30 June 2020. Besides, the company has also adjusted the objective of shipment of camera modules which changed from the target of increase by not less than 30% to 25% of the shipment of camera modules in 2021 and we think it is achievable. In terms of camera modules, from the data released by the company's shipments form January to June 2021, the company's shipments in the first half of 2021 performed well. Shipments in the first half of 2021 increased by 24% yoy and 5% mom. In addition, from the perspective of product structure of camera module shipments in the first half of 2021, 8 million pixels and below/ 10-24 million pixels/ 32 million pixels and above camera modules accounted for 29%/ 38%/ 32% of the total shipments, respectively. The proportion of mid-and-high-end products continues to rise. In view of this, it is predicted that the company's average unit price of camera modules will increase slightly in 2021. With the increase in shipment volume and average unit price, the segment revenue of camera modules will increase.

In terms of fingerprint identification modules, from the data released by the company's shipments from January to June 2021, the shipments volume performed well. Shipments in the first half of 2021 increased by 38.7% yoy and 6.5 mom. It is expected that the target set by the company: the shipment volume of fingerprint identification modules for the whole year will increase by not less than 30% yoy, which is expected to be achieved. At the same time, the proportion of under-glass and non-under-glass fingerprint recognition modules in 2021 will be 56%/ 44% respectively. The corresponding proportion in 2020 is 51%/ 49%. It is expected that with the increase in annual shipments and the proportion of fingerprint recognition modules under the glass, the segment revenue of fingerprint recognition modules will also increase.

In terms of expense ratio, the company is expected to continue to increase research and development expenses to maintain its competitiveness in the industry. It is estimated that the research expenses will be RMB 7.2/ 9.0/ 1.05 billion in 2021-2023, accounting for approximately 3.4% of total operating income.

Company valuation

As of July 16, the closing price was 16.84, the company's rolling price-earnings ratio was 19.51x. We predict that the company's earnings per share in 2021/ 2022/ 2023 will be RMB 1.01/ 1.25/ 1.44, and the CAGR from 2021-2023 will be 19.4%. Considering that the company occupies a certain position in the camera module industry, the demand for camera modules in mobile phones, automobiles, and IoT has increased and the company has begun to diversify its layout. The company is given an “accumulate” rating (first coverage). The 2021 target price given to the company is HK$20.12, which corresponds to a P/E ratio of 17.0x/ 13.7x/ 11.9x, corresponding to the EPS of 2021/ 2022/ 2023.

Risk factors

1) Epidemic

2) The sales of global mobile phone (typically 5G smartphone) is less than expected

3) The compnay's progress in the opticsal business is slower than expectation

Financial

Click Here for PDF format...