Change in ERP Solutions structure, Increase in the proportion of additional services

The company aims to continue to improve the mid-to-high-end product structure while increasing the average unit price to catch up with the performance of the leading company Sunny Optical. In 2020, the company's shipments of 32 million pixels and above camera modules accounted for 24.2% of the company's total shipments (+14.6 ppts yoy). The camera modules with 10 to 24 million pixels rose steadily, accounting for 47.1% in 2020 (+2.9 ppts yoy). The proportion of lower-end camera modules with 8 million pixels and below dropped from 46.2% in 2019 to 28.7% in 2020 (-17.5 ppts yoy). The company's goal is that by 2021, 32 million pixel and above cameras will account for no less than 30% of shipments. According to the shipment volume performance in the first half of 2021, the proportion of 32 million pixel and above cameras accounts for 32% and the goal is expected to achieve.

Achieve profitability in SaaS products

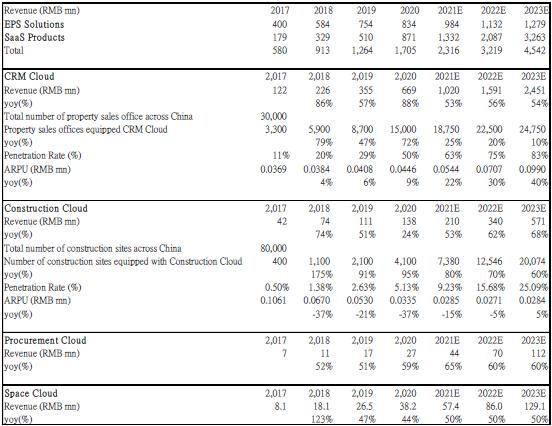

Based on the focuses in the industry chain, the company's SaaS products can be classified into three major categories, namely CRM Cloud for the marketing market, Construction Cloud and Procurement Cloud for the supply chain market, and Space Cloud for the existing market. Among them, CRM Cloud is the most mature SaaS product with a high growing trend. In 2020, the revenue from CRM Cloud was RMB 669 million (+88.3% yoy) while the revenue of that was RMB 355 million in 2019. Besides, the growth rate of the company's other three major products, Construction Cloud, Procurement Cloud and Space Cloud also maintained rapid growth. In 2020, the revenue was RMB 137, 27, 38 million respectively (+23.5%, +58.5%, +44.1% yoy). At the same time, the SaaS product business turned losses into profits for the first time, while a net profit of RMB 18.7 million. In 2019, there was a loss of RMB 60.5 million (+144.7% yoy). In 2018, 2019 and 2020, 92, 96 and 97 of the Top 100 property developers subscribed for at least one of the SaaS products.

Accelerating the marketing and service channel expansion to cover lower-tier cities, Further strengthening in depth cooperation with industry-leading enterprises

The number of cities covered by the company's market and service network increased from 42 to 70, to provide localized professional services for customers. The company sell and deliver SaaS products and ERP solutions through company's direct sales force and a nationwide network of regional channel partners. The revenue from SaaS products and ERP solutions generated through regional channel partners was significant and accounted for approximately 47% of total revenue in 2020. In 2020, 97 of the Top 100 property developers subscribed for at least one of the SaaS products and the average amount of cooperation with the Top 100 property developers increased significantly from RMB 4.7 million in 2019, to RMB 6 million in 2020, fully demonstrating the trust of industry-leading enterprises in the company's products and services. Besides, the company provided ERP solutions services for 89 of the Top 100 property developers.

Company valuation

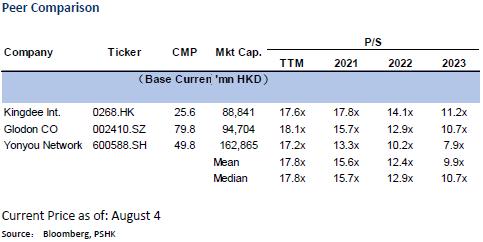

As of August 4, the closing price was HKD 29.0. The company is a SaaS company, and ERP solutions provide stable revenue and growth. Therefore, we will use the segment valuation method to evaluate the company's two businesses separately. Based on the 25x target P/E on 2022 ERP solution net profit and 35x target P/S on 2022 SaaS products revenue which adopting a higher P/S valuation in the industry, the target price given to the company is HKD 48.90, which corresponds to a P/S of 41.6x/ 29.9x/ 21.2x, corresponding to 2021/ 2022/ 2023. The company is given an “Buy” rating (first coverage).

Company Profile

Ming Yuan Cloud Group was found in 2003 and was listed on the main board of the Hong Kong Stock Exchange in Sept 2020. The company specialize in providing enterprise-grade SaaS products (including CRM Cloud, Construction Cloud, Procurement Cloud and Space Cloud) and ERP solution for property developers and other industry participants in the real estate value chain in China to help them achieve delicate and digital operation of their businesses. The company is the no. 1 software solution provides for property developers in China with a market share of 18.5% in terms of revenue in 2019, according to Frost & Sullivan. Within this market, the company is also the no. 1 provider of both ERP solutions and SaaS products in terms of revenue, with leading market shares of 16.6% and 23.3%, respectively. In 2020, 97 of the Top 100 property developers subscribed for at least one of the SaaS products.

Company Development Process

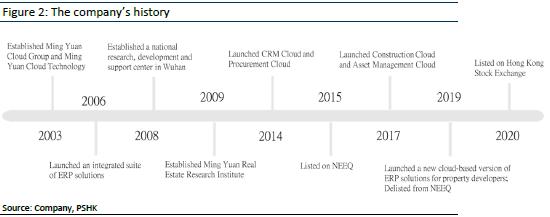

The company was founded in 2003 with the establishment of one of the principal subsidiaries, Ming Yuan Cloud Technology. In 2006, the company launched an integrated suite of ERP solutions for property developers to manage their business processes across organization. In 2014, the company launched CRM Cloud and Procurement Cloud; In 2017, the company launched Construction Cloud and Asset Management Cloud. In 2019, the company launched a new cloud-based version of ERP solutions for property developers and served nearly 3,000 property developers in 2019, covering 99 of the Top 100 property developers.

Besides, in March 2011, Ming Yuan Cloud Technology applied for listing of its shares on the growth enterprise board of the Shenzhen Stock Exchange, but was not successful pursuant to a decision of the CSRC as the CSRC considered at the relevant time that 1) majority of its sales were derived from existing customers rather than from new customers; 2) relatively large amount of its sales revenues were contributed by small and medium-sized property developers; 3) the procurements of products from small and medium-sized customers may be adversely affected by the macro-policy adjustment of the property development industry in the PRC since 2010. The company view that these issues are no longer applicable and relevant since 2012 due to developments in the company's business model and customer base, and the change in the macro-economic environment in the PRC.

Subsequently, the company was listed on the NEEQ in June 2015 to obtain an active and effective corporate financing platform for the company and strengthen corporate governance in pursuit of long-term business development. Subsequently, in 2019, having considered that the trading activity and brand awareness on the SME Board may not be able to meet our expectation. In particular, the company considered that international investors are relatively more familiar with the Company's industries, business, and the SaaS products. In January 2019, the company was delisted from NEEQ by way of its voluntary application for delisting. After completing the company's reorganization, the company will finally be officially listed on the Hong Kong Stock Exchange in September 2020 to find the identification of the company's fair value, while exploring potential overseas expansion opportunities and expanding access to global investors.

Industry Analysis

Slow growth in market size of China's real estate industry

In the past years, the real estate market in China has grown steadily in the past years. China's rapid urbanization and rising middle class with increasing demand for housing have been and are expected to continue serving as the main growth engines of its real estate industry including its new housing market. The transaction value of new houses in China had grown from approximately RMB8.7 trillion in 2015 to RMB16.0 trillion in 2019. According to Frost & Sullivan, driven by the increasing urbanization in China and government support, the real estate market in China is expected to continue growing as a major driving force to the national economy in the future, with the transaction value of new houses expected to reach approximately RMB21.6 trillion in 2024, 2021-2024 CAGR is 8.1%.

Driving Forces of China's Real Estate Industry Chain

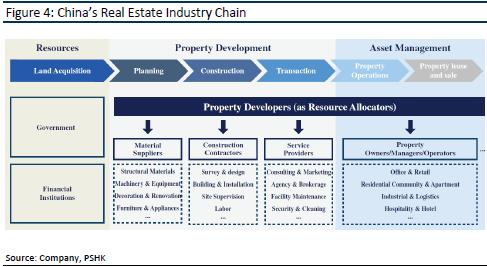

The real estate value chain in China involves a variety of participants throughout the entire property development and asset management cycle, including property developers, property sales agents, suppliers, asset managers, property operators and other industry participants along the real estate value chain, in a complex array of business scenarios. Among these participants, property developers represent the key driving force for the growth of the entire real estate industry, connecting various other participants along the value chain. Uniquely positioned to coordinate and allocate resources throughout the entire value chain, China's property developers have gained tremendous influence over other industry participants and have taken the helm of the industry trends.

Technological transformation needs of China's real estate industry

As market competition in China continues to intensify, it has become increasingly important for property developers to reduce operating costs, improve management efficiency and transparency, and better manage customer relationships to achieve sustainable and profitable growth in this highly competitive market with more than 30,000 property developers in 2019. Property developers in China have historically been underserved by enterprise grade technologies that can streamline and optimizing their complex business functions and facilitating the gathering and processing of a vast amount of data and information. Many of these companies have been relying on manual processes or operating with a variety of disparate and disintegrated systems. With technological advancements and rising awareness of property developers, the real estate industry has witnessed an enormous, growing demand for software solutions that enable digitalized, streamlined, and optimized business operations for property developers. Apart from property developers, digitalization through adoption of software solutions also empowers other key participants along the real estate value chain under a full spectrum of business scenarios, including procurement, construction, customer relationship management, and property asset management. In 2019, the market for software solutions to the real estate value chain in China reached approximately RMB17.0 billion.

Rapidly growth in software solutions of China's Real Estate industry

The market for software solutions to the real estate value chain in China had a penetration rate of 0.10% in 2019, significantly lower than that of 1.55% in the U.S. market and still lower than other comparable industries in China, such as banking services and healthcare. The main reason is property developers and other industry participants have historically been focused on driving rapid business growth by competing for the tremendous, fast-growing housing demand, which had significantly outpaced the development of their internal management and technology systems. The penetration rate of software solutions in China's real estate industry is expected to rapidly increase from 0.10% in 2019 to 0.30% in 2024, 2019-2024 CAGR is 24.6%.

The market for software solutions to the real estate value chain in China in terms of revenue has experienced significant growth in recent years, growing from approximately RMB7.1 billion in 2015 to RMB17.0 billion in 2019. With the increasing awareness of digital transformation among property developers and other industry participants, the advancement in technologies and the growing market acceptance of SaaS products that serve various application scenarios, the market for software solutions to the real estate value chain in China in terms of revenue is expected to continue its rapid growth.

According to Frost & Sullivan, it is expected to reach RMB 65.5 billion in 2024, representing a CAGR of 31.0% from 2019 to 2024. China's real estate industry software solutions are mainly composed of two parts: 1) software solutions for real estate developers, and 2) software solutions provided to other industry participants (such as construction contractors and property asset management companies) which has demonstrated significant potential to grow with a penetration rate of 0.1% in 2019. As of 2019, there were approximately 90,000 construction contractors and 120,000 property asset management companies in this highly fragmented and rivalrous market. The expected growth is largely driven by increasing demands for data analytics, supply chain management, and a variety of complex and data-driven business and operational scenarios relating to property asset management.

Software Solutions to Property Developers in China

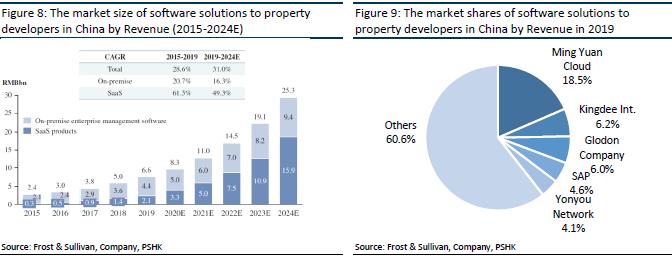

Software solutions to property developers enable property developers to optimize core property-related operations, including sales and marketing, procurement, cost management, project management, budgeting, and property asset management, thereby significantly enhancing business results and efficiency. According to Frost & Sullivan, the market for software solutions to property developers in China in terms of revenue has achieved significant growth in recent years, growing significantly from approximately RMB2.4 billion in 2015 to RMB6.6 billion in 2019 at a CAGR of 28.6%. With the increasing adoption of technology-driven software solutions, we expect the penetration of software solutions to accelerate, with the market size in terms of revenue increasing to RMB25.3 billion in 2024, representing a CAGR of 31.0% from 2019 to 2024. The market is relatively concentrated and the main competitors are Ming Yuan Cloud, Kingdee International and Glodon Company. The CR5 accounts for about 39.3% of the market share. Ming Yuan Cloud is the absolute leader with 18.5% of the market share.

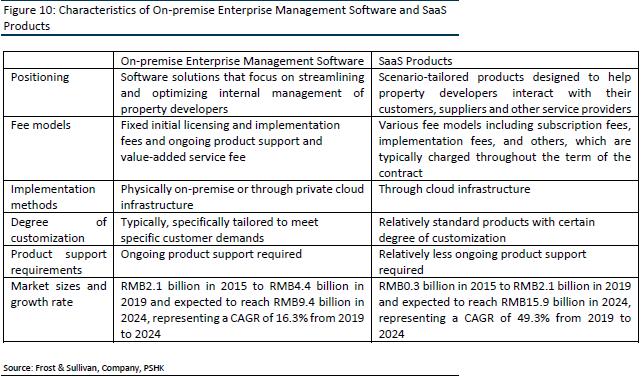

Among them, the software solutions to property developers mainly consist of 1) on-premise enterprise management software and 2) SaaS products. On-premises enterprise management software includes a universe of software solutions that focus on streamlining and optimizing internal management of property developers, such as ERP solutions that integrate multiple core business operations into a unified system and database, and various other software solutions that are specifically tailored to standalone business functions such as supply chain management and human capital management. SaaS products are scenario-tailored products that are designed to help property developers interact with their customers, suppliers, and other service providers with a goal to enhance business efficiency and drive long-term growth.

On-premise Enterprise Management Software includes software licensing, implementation services, product support services and value-added services. Ongoing product support plays a key role in ensuring the effective operation of on-premise enterprise management software. In addition, property developers` increasing need for upgrading ad customization call for a variety of value-added services tailored to thespecific needs of customers. As such, product support and value-added services have been and are expected to continue driving the overall growth of this market. According to Frost & Sullivan, market sizes of product support and value-added services in terms of revenue are expected to further reach RMB2.5 billion and RMB3.5 billion in 2024, at a CAGR of 26.9% and 21.1% from 2019 to 2024, respectively. The total on-premise enterprise management software CR5 is 40.4%, while Ming Yuan Cloud ranks no. 1 with 16.6% market shares.

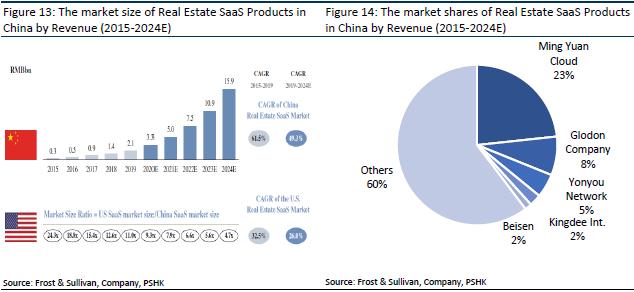

Despite rapid historical growth, China's real estate SaaS products market is still underdeveloped with significant potential for accelerated growth, as compared to that of the United States. According to Frost & Sullivan, the U.S. real estate SaaS products market was 11.0 times of that in China in 2019 in terms of revenue. Therefore, its Chinese market has huge potential for accelerating growth. The market for real estate SaaS products in China in terms of revenue had exponentially grown from approximately RMB0.3 billion in 2015 to RMB2.1 billion in 2019, representing a CAGR of 61.5%, and it is expected that the market in terms of revenue will be RMB15.9 billion in 2024, representing a CAGR of 49.3% from 2019 to 2024. The total SaaS products CR5 is 39.7%, while Ming Yuan Cloud also ranks no. 1 with 23% market shares.

Frequently promulgated policies for the real estate industry, Different influence on large, medium-sized real estate companies

In August 2020, the People's Bank of China and the Ministry of Hosing and Urban-Rural Development jointly convened a symposium on key real estate companies, proposed a series of rules for the monitoring and financing of real estate companies` funds, and established “three red lines”, including 1) the debt-to-asset ratio after excluding advance receipts shall not be greater than 70%, 2) the net debt ratio shall not be greater than 100%, 3) the short-term debt ratio is not less than 1. Besides, according to the number of “stepping on the line” of the regulatory indicators, corresponding to the four levels of “red, orange, yellow and green”. If all indicators meet the regulatory requirements, they will be classified as “green” and the growth rate of interest-bearing liabilities can reach 15%. The one, two and indicators of “steeping on the line” correspond to “yellow, orange, green” and the growth rate of interest-bearing liabilities must not exceed 10%/ 5%/ 0%. In addition, the “centralized land supply” policy requires key cities to reasonably arrange the timing of bidding, auction and listing residential land. Two sets of regulation are established, 1) the transfer announcement shall be issued in a centralized manner, and in principle shall not exceed 3 times throughout the year, and the interval and the amount of land supply shall be relatively balanced; 2) centrally organize transfer activities.

A series of policies launched by the government are mainly aimed at stabilizing land prices and housing prices and establishing a long-term mechanism for perfecting the real estate market. They have different impacts on various types of real estate developers. For example, high-debt real estate developers who are in the “red” and have always relied on high-leverage models to obtain land and business scale through financing will be restricted. At the same time, it reduces the profitability of large real estate companies, which poses greater challenges to capital allocation and operational capabilities. On the other hand, it is more difficult for small and medium-sized real estate developers to achieve corner overtaking by leveraging, and sales will slow down. In the case of poor allocation of funds, SMEs are exposed to greater credit risks. Therefore, for the entire industry of real estate developers, the first tasks they need to face are fast sales, high turnover, and increased cash flow to improve corresponding policies and indicators. Real estate developers are increasingly eager for sophisticated and digital operations.

Company Competitive Advantage

Ming Yuan Cloud provide 1) Enterprise-grade ERP solutions, focused on streamlining and optimizing internal management and operations of property developers, and typically procured by property developers at the group level in accordance with their IT expenses budget; 2) SaaS products, including CRM Cloud, Construction Cloud, Procurement Cloud and Space Cloud, help property developers and other real estate industry participants to optimize their procurement, construction, marketing and sales, property asset management and other property related operations. Benefitting from the cloud infrastructure and technology, the company SaaS products are effectively integrated with our ERP solutions.

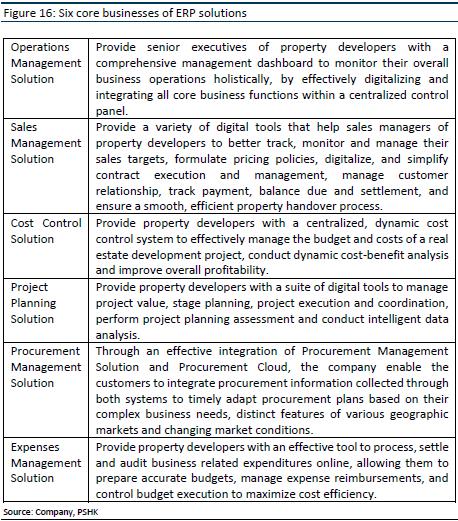

ERP Solutions – Helping Property Developers run the business optimally

The company's ERP solution assists real estate developers in optimizing operating efficiency, covering six core businesses, including Operations Management Solution, Procurement Management Solution, Cost Control Solution, Project Planning Solution, Expenses Management Solution and Sales Management Solution. They enable property developers to access and analyze key operational and financial data in real time, offer insights into daily operations, provide holistic and actionable suggestions, and connect business functions and the people within them. In 2017, the company introduced a cloud-based version of the ERP solutions where the solutions are hosted and delivered through cloud-based infrastructure of their customers.

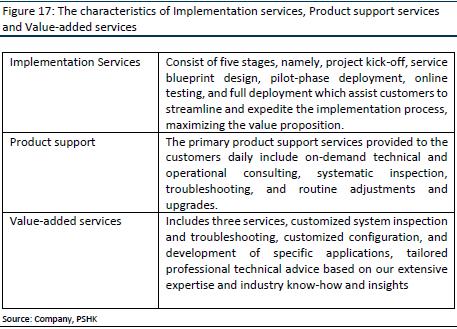

Implementation services, Product support services and Value-added services

In addition to software licensing, the company offer customers a variety of delivery and support services to ensure successful implementation and effective operation of the ERP solution. The customers typically subscribe for implementation services and one-year product support services when they enter into software licensing agreements.

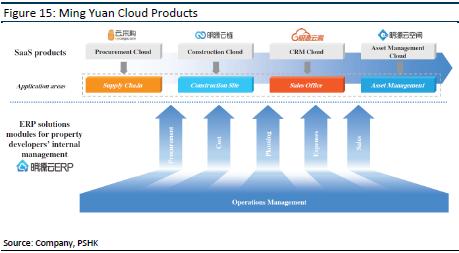

Providing smart solutions to diversified real estate industry participants by SaaS products

The company's SaaS products include four major cloud service offerings, namely CRM Cloud, Construction Cloud, Procurement Cloud and Asset Management Cloud, catering to the diverse needs of property developers, construction materials suppliers and property asset management companies.

CRM Cloud

CRM Cloud provides property developers with various digitalized tools to improve their customer acquisition capabilities and optimize the site management of their property sales offices. It enables property developers to effectively generate sales leads and identify prospective property purchasers, allows sales representatives of property developers to interact with third-party sales agents and brokers efficiently, thereby improving sales performance and streamlining the property sales process with a superior customer experience and lower transaction costs. It includes three features, 1) Multi-channel digital marketing tools, enables property developers to quickly and easily establish their own online AI cloud stores and 5G mobile sales offices running on Weixin/WeChat mini program by using drag-and-drop tools without writing code, 2) Smart property sales offices and site management, leveraging the company's big data analytics and AI technology to improve sales efficiency and results. 3) End-to-end facilitation of property sales process, serves a wide array of business scenarios in a property purchase transaction, from first-time sales office visits to confirming property purchases and paying deposits, from property inspections to contract executions.

In 2018, 2019 and 2020, a total number of approximately 1,700, 2,400 and 4,200 paying end group customers subscribed for CRM Cloud, respectively. The number of property sales offices across China equipped with CRM Cloud was approximately 5,900, 8,700 and 15,000 in 2018, 2019 and 2020, respectively. The annual customer account retention rate for CRM Cloud was approximately 93%, 96% and 90% in 2018, 2019 and 2020, respectively.

Construction Cloud

Construction Cloud offers property developers a comprehensive suite of digitalized solutions to manage the entire property construction and delivery process, allowing them to enhance operating efficiency and quality control and reduce costs and associated risks. It has three main features, 1) Property construction, focuses on the key elements of the property construction process, including progress planning, process management, materials management, and measuring. 2) Property inspection and delivery, through our mobile app and Weixin/WeChat mini program, property developers, construction contractors, and property owners have real-time access to the latest status of property inspection, defect rectification, and property handover process. 3) Cost management, improve the operational efficiency of property construction and delivery process with online contract execution, payment, and settlement services, which allows property developers to monitor and manage costsin real time.

In 2018, 2019 and 2020, approximately 300, 400 and 800 paying end group customers subscribed for Construction Cloud, respectively. The numbers of construction sites equipped with Construction Cloud in China were approximately 1,100, 2,100 and 4,100 in 2018, 2019 and 2020, respectively. The total annual customer account retention rate for quality inspection and customer service products of Construction Cloud was 85% in 2020.

Procurement Cloud

Procurement Cloud is a procurement and supply chain management platform that connects property developers and construction materials suppliers and other service vendors and allow both parties to reduce transaction costs and improve the efficiency and transparency of the material procurement process in connection with property development. It has mainly two features, 1) online procurement platform for property developers, providing a massive and dynamic database capable of intelligently connecting the relevant suppliers with procurement requests of our property developer customers. 2) Online marketing platform for suppliers, allowing suppliers to optimize marketing efforts and effectively participate in online bidding process.

Asset Management Cloud

Asset Management Cloud provides property developers, property asset management companies and property management companies with various tools to streamline and optimize real estate management process and improve operational efficiency and reduce costs through digital management of various property assets across different geographic locations. It has three features, 1) Asset optimization, covering a full spectrum of business functions and processes through the entire life cycle of a variety of residential or commercial property assets, including property investment, financing, construction, management, and disposition. 2) Lease management, providing mobile-friendly digital tools for customers to manage lease execution, renewal, and termination, as well as rental payment and billing, enabling them to optimize their rental and pricing strategies and maximize investment returns. 3) Property operations, focusing on three core business scenarios, property on-site management, customer services and payment and billing management, which have traditionally been carried out manually or through a combination of software products of various vendors.

PaaS Plat – Skyline Open Platform

In November 2020, the company launched Skyline Open Platform, a powerful enterprise-grade PaaS platform. With a focus on the five major independent capabilities of “agile development, full-area integration, process driven, data insight and technological innovation”. Skyline Open Platform provides more than 10 core capability areas, including “modeling platform, mobile platform, BPM process platform, data analysis platform, big data management platform, integrated and open platform, AIoT platform etc., implementation and management of applications.

Compared with the traditional application platform, Skyline Open Platform supports users in fully developing “user interface, business logic, process services and data services” through “no-code and low-code” methods and improves productivity through cross-platform portability for users. The company can develop high-quality SaaS products and update products in a short period of time to cater to changing customer needs and technological innovation. On the other hand, the company can also open up the functions of the Skyline Open platform to customer's IT teams, third-party real estate developers, and business partners to encourage customers to provide innovative application and enrich the company's product features and technology ecosystem.

Operating Condition

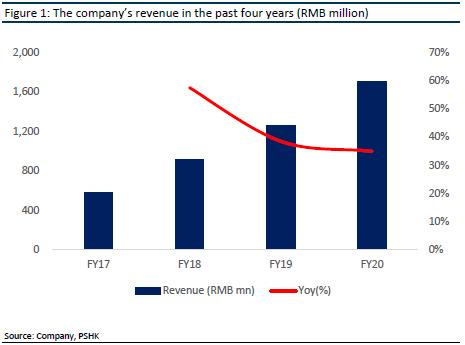

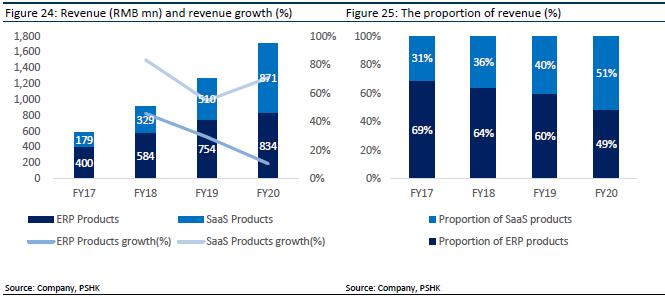

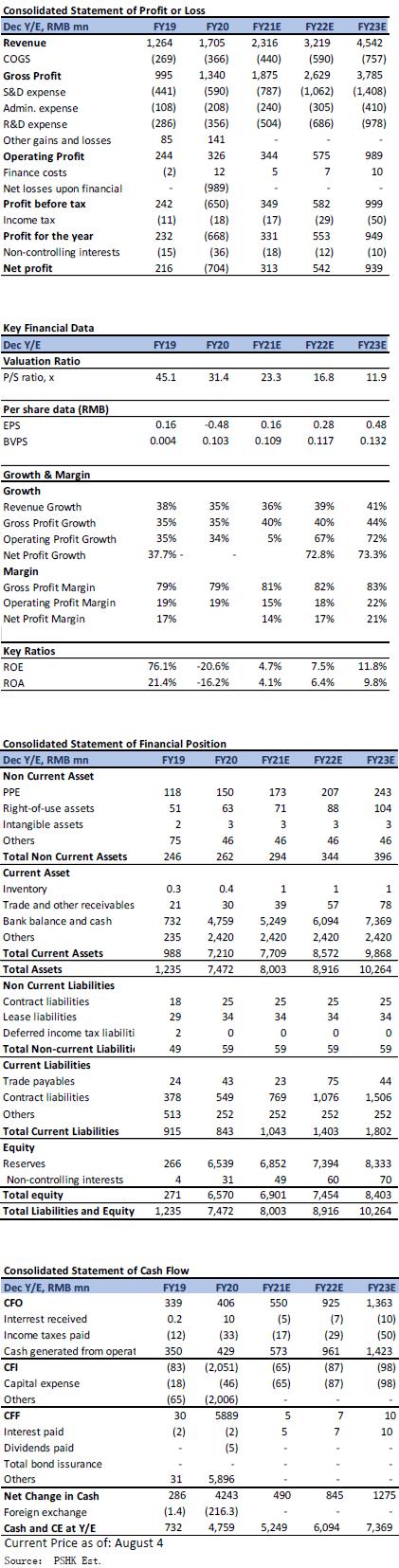

In 2020, the outbreak of COVID-19 had a great impact on the upstream and downstream industries of the real estate value chain, which has also brought about greater innovations in the industry. In 2020, the company's total revenue was RMB 1.7 billion (+34.9% yoy), and the company reported a net loss of approximately RMB 668.2 million, compared to the profit of approximately RMB 231.6 million for the year 2019. Besides, the company reported the adjusted net income was RMB 383 million (+62.2% yoy), which included net losses upon financial liabilities at FYPL transferred to equity RMB 989 million.

The company's current products are mainly divided into ERP solutions and SaaS products, accounting for 49% and 51% of revenue in 2020, respectively. In 2020, the total revenue of SaaS products accounted for the first time higher than that of ERP solutions. In 2018/ 2019, they accounted for 64% and 36%/ 60% and 40% respectively. In 2020, the company's revenue from ERP solutions was RMB 834 million (+10.6% yoy) and 2018/ 2019 accounted for RMB 754/ 584 million. In addition, in 2020, the company's revenue from SaaS products is RMB 871 million (+70.9% yoy). The revenue of SaaS products surpassed the revenue of ERP solutions for the first time and the growth trend of SaaS products is obvious. At the same time, the SaaS product business turned losses into profits for the first time, while a net profit of RMB 18.7 million. In 2019, there was a loss of RMB 60.5 million (+144.7% yoy).

Change in ERP Solutions structure, Increase in the proportion of additional services

The company's ERP solution revenue is mainly divided into four parts, software licensing, implementation services, product support and value-added services. In 2020, the revenue will be RMB 250/ 103/ 138/ 344 million respectively. Due to the impact of the epidemic, the decision-making cycle of end customers for the new purchase and upgrade of software products and the demand for value-added services was postponed, which resulted in a slowdown in the growth rate of revenues from product sales and value-added services in 2020. On the other hand, the company began to outsource a portion of the value-added services and product support services to third-party software service providers. Such services mainly include routine and standard software development and product maintenance services which it is more cost-effective to be performed by experienced third-part service providers. Therefore, value-added services and product support services have a high growth.

From the perspective of the trend of the proportion of ERP solutions, the company's proportion in software licensing and implementation services continues to decline, from 39% and 17% in 2017, to 30% and 12% in 2020 respectively. On the contrary, the proportion of product support and value-added services has continued to rise, from 14% and 29% in 2017 to 17% and 41% in 2020, respectively.

In terms of gross profit, the gross profit of ERP solutions in 2020 is RMB 581 million (+10% yoy) and the gross profit margin remains at around 70% for a long time, compared with 69.7% in 2020 (-0.5 ppts). There is a slight downward trend in gross profit margin, and the main increased costs are outsourcing expenses and the cost of inventories sold.

Achieve profitability in SaaS products

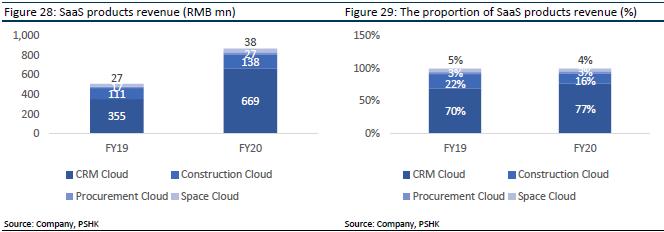

Based on the focuses in the industry chain, the company's SaaS products can be classified into three major categories, namely CRM Cloud for the marketing market, Construction Cloud and Procurement Cloud for the supply chain market, and Space Cloud for the existing market. Among them, CRM Cloud is the most mature SaaS product with a high growing trend. In 2020, the revenue from CRM Cloud was RMB 669 million (+88.3% yoy) while the revenue of that was RMB 355 million in 2019. Besides, the growth rate of the company's other three major products, Construction Cloud, Procurement Cloud and Space Cloud also maintained rapid growth. In 2020, the revenue was RMB 137, 27, 38 million respectively (+23.5%, +58.5%, +44.1% yoy). At the same time, the SaaS product business turned losses into profits for the first time, while a net profit of RMB 18.7 million. In 2019, there was a loss of RMB 60.5 million (+144.7% yoy). In 2018, 2019 and 2020, 92, 96 and 97 of the Top 100 property developers subscribed for at least one of the SaaS products.

From the perspective of the proportion of SaaS products, CRM Cloud is a major source of revenue for the company, accounting for 77% of the company's total revenue from SaaS products (+7 ppts yoy). CRM Cloud continued to increase market penetration and customer unit prices, and launched a new version of the Handheld Sales Office which integrates various application scenarios including online dissemination, digital exhibition hall, VR showing and online property launch, so as to promote the efficient interaction among home buyers, property consultants, third-party sales agents and brokers, greatly improve the experience of home buyers, and the customer acquisition ability and transaction conversion efficiency of property developers, and effectively help property developers reduce their marketing transaction costs significantly. In 2020, a total number of approximately 4,200 paying end group customers subscribed for CRM Cloud, respectively.

In term of gross profit, the gross profit was 758 million in 2020 (+63% yoy), but the gross profit has a little decline from 91.2% in 2019 to 87.1% in 2020 (-4.1 ppts yoy), mainly because with regard to the CRM Cloud products, the company increased their investment in the integration of hardware and software, based on the demand at the sales site, and intelligent hardware was used more and more widely, while the gross profit margin of intelligent hardware sales was comparatively lower.

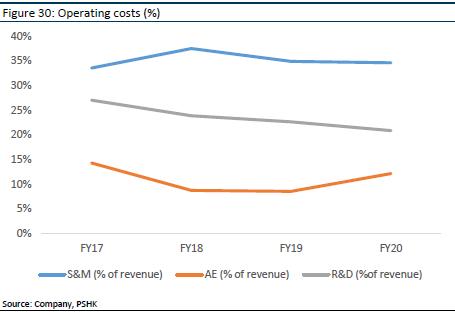

Selling and Marketing Expenses

The company's operating costs mainly include selling and marketing expenses, general and administrative expenses, research and development expenses. Among them, selling and marketing expenses will reach RMB 590 million in 2020 (+33.8% yoy). The expense ratio is maintained at approximately 35% of total revenue. The increase in selling and marketing expenses was mainly due to the increase in dealer commission expenses arising out of the increase in revenues from SaaS products, and the increase in employee benefit expenses of the sales team. For the general and administrative expenses, and research and development expenses, the proportion of that to the total revenue are 12% and 21% which accounts for the expenses 208 million and 356 million respectively (+12% and +24% yoy).

Accelerating the marketing and service channel expansion to cover lower-tier cities, Further strengthening in depth cooperation with industry-leading enterprises

The number of cities covered by the company's market and service network increased from 42 to 70, to provide localized professional services for customers. The company sell and deliver SaaS products and ERP solutions through company's direct sales force and a nationwide network of regional channel partners. The revenue from SaaS products and ERP solutions generated through regional channel partners was significant and accounted for approximately 47% of total revenue in 2020. In 2020, 97 of the Top 100 property developers subscribed for at least one of the SaaS products and the average amount of cooperation with the Top 100 property developers increased significantly from RMB 4.7 million in 2019, to RMB 6 million in 2020, fully demonstrating the trust of industry-leading enterprises in the company's products and services. Besides, the company provided ERP solutions services for 89 of the Top 100 property developers.

Financial forecast

The company's ERP solution revenue is mainly divided into four parts, software licensing, implementation services, product support and value-added services. The company provided ERP solutions services for 89 of the Top 100 property developers which the penetration rate of ERP products in leading real estate companies has been relatively high. It is expected that the sinking market will continue to be explored in the future. With the increasing penetration rate in the future, the product support services are expected to grow faster. We expected the company's overall year-on-year growth rate in ERP solutions in 2021/ 2022/ 2023 to be 18%/ 15%/ 13%, respectively.

In terms of SaaS products, they include 1) CRM Cloud, 2) Construction Cloud, 3) Procurement Cloud and 4) Space Cloud. CRM Cloud has always been the company's main source of revenue for its SaaS products. It is expected that as the company continues to increase its penetration rate, the number of property sales offices across China equipped with CRM Cloud continues to increase, and the company's revenue will increase by 52.5% yoy in 2021. The growth logic of Construction Cloud is similar to that of CRM Cloud that the growth rate of the number of construction sites equipped with Construction Cloud in China is expected to remain strong, and the revenue will increase by about 53% yoy. The Procurement Cloud currently has the lowest revenue base, and it is expected that under the continuation of the epidemic, Procurement Cloud provides real estate developers with online tools to assist them in completing online supplier sourcing, matching negotiations, bidding, and procurement, etc. Its revenue is expected to increase by 65% yoy in 2021. Space Cloud comprises two sub-product lines, among which Asset Management Cloud focuses on the field of asset management, providing various forms of online asset management digitization solutions for asset owners. On March 2021, the company has acquired Woxiang Technology (沃享科技), an internet+ commercial real estate digital solution provider. It is expected that the company will accelerate its transformation in commercial real estate. At the same time, it maintains the development of Cloud Asset Management and Cloud Property Management in the sub-product line. The company's cloud space revenue in 2021 is expected to grow by about 50% yoy. On the whole , SaaS products are expected to grow rapidly, and the proportion of SaaS products in total revenue will continue to increase. In 2021/ 2022/ 2023, the proportion of SaaS products will be expected to be 58%/ 65%/ 72%.

We expected that in 2021/ 2022/ 2023, the company's total revenue will be RMB 2.32/ 3.22/ 4.54 billion, the revenue of ERP solution are RMB 984/ 1,132/ 1,279 million and SaaS products are RMB 1,332/ 2,087/ 3,263 million respectively. The company's attributable profit is expected to be RMB 313/ 519/ 894 million, and the EPS are RMB 0.16/ 0.28/ 0.48.

Company valuation

As of July 16, the closing price was HKD 29.0. The company is a SaaS company, and ERP solutions provide stable revenue and growth. Therefore, we will use the segment valuation method to evaluate the company's two businesses separately. Based on the 25x target P/E on 2022 ERP solution net profit and 35x target P/S on 2022 SaaS products revenue which adopting a higher P/S valuation in the industry, the target price given to the company is HKD 48.92, which corresponds to a P/S of 41.6x/ 29.9x/ 21.2x, corresponding to 2021/ 2022/ 2023. The company is given an “Buy” rating (first coverage).

Risk factors

1) Market competition in SaaS product

2) The market has lowered the overall valuation premium of the SaaS industry

Financial

Click Here for PDF format...