Investment Summary

Efforts in battery parts M&A to ensure future battery supply for long-term and stable electrification

The Company recently announced that its subsidiary Jirun Automobile will establish a company with Sunwoda (300207.SZ) and Geely Auto Group, with a registered capital of RMB100 million. The contribution of the three companies is RMB41.5 million, RMB30 million and RMB28.5 million, respectively, accounting for 41.50%, 30% and 28.5%, respectively, of the total. The joint venture will produce HEV (including 48V) power battery packs to meet the demand of Zhejiang Jirun, Geely Group and their related parties for power battery products for all their HEV vehicles. After mass production is achieved, the peak annual production capacity in the first phase shall be at least 600,000 HEV (including 48V) power battery packs, and that in the second phase shall be at least 800,000 packs.

Sunwoda is a global leader in consumer battery packs, and it engaged in power battery business early. Up to now, Sunwoda has mass-produced BEV power cell energy density of 244Wh/kg and leading technologies, and has already owned new energy vehicle customers including Geely, Dongfeng Liuzhou Motor, Renault Nissan, Volvo, EJET, SAIC-GM-Wuling and XPeng, as well as electric bicycle customers including NIU, Hulong, Meierdun and Aima.

In the first half of 2021, 1206 thousand new energy vehicles were sold in China, a two-fold yoy increase, flat with that throughout 2019 and accounting for nearly 88% of the 1367 thousand vehicles in 2020. With the increasingly obvious trend of new energy vehicles, the demand for high-quality power batteries will continue to increase. Geely cooperating with Sunwoda, put efforts into the power battery sector to guarantee the supply while effectively reducing the cost of battery in the future.

New vehicle effect to drive beyond-expectation sales in H2

Due to chip shortage, a high base in the same period last year and fewer new models in the first half of this year, Geely sold 99275 vehicles ((including LYNK&CO) in July, down by 5.65% yoy and 0.9% mom, with a growth rate lower than the industry average. In particular, 18225 LYNK&CO were sold, up by 19% yoy and 6.7% mom, 7794 new energy vehicles were sold, up by 22% yoy and by 3.7% mom, and 7054 vehicles were exported overseas, up by 56% yoy and 0.2% mom.

In the first 7 months of this year, Geely sold 729.5 thousand vehicles in total, reaching 47.7% of its full-year target of 1.53 million. Specifically, it sold 38 thousand new energy vehicles and exported 60 thousand vehicles.

In the second half, Geely's sales volume is expected to grow beyond expectations with the launch of a series of blockbuster models including Preface Space-time Edition in mid-June, Binrui in early July, CMA-based Xingyue S and Xingyue L in late July and Binyue, New Emgrand in August, as well as the delivery of ZEEKR 001 from October. The new models are largely reserved. In 48 hours, over 10,000 Geely Xingyue L were ordered, and till now, this number reached about 30,000. Deliverable ZEEKR 001 in 2021 have been sold out, and over 60% of the customers ordered nigh-configuration models. We believe that the brand strategy integrating Xingyue and Xingrui and the high-end ZEEKR will contribute to the Company's product mix re-upgrading.

Investment Thesis

We still believe that the trend of automobile intellectualization and global automobile electrification led by consumption upgrading is in the ascendant, and Geely, with efforts in chips, software/algorithms, high-precision maps and power batteries and possible capital integration in the future, is expected to boost its valuation.

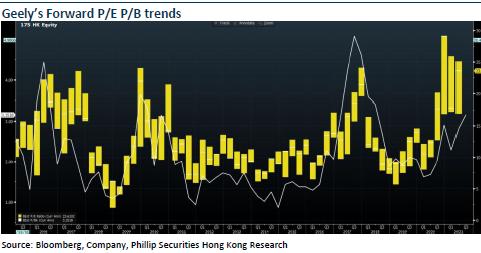

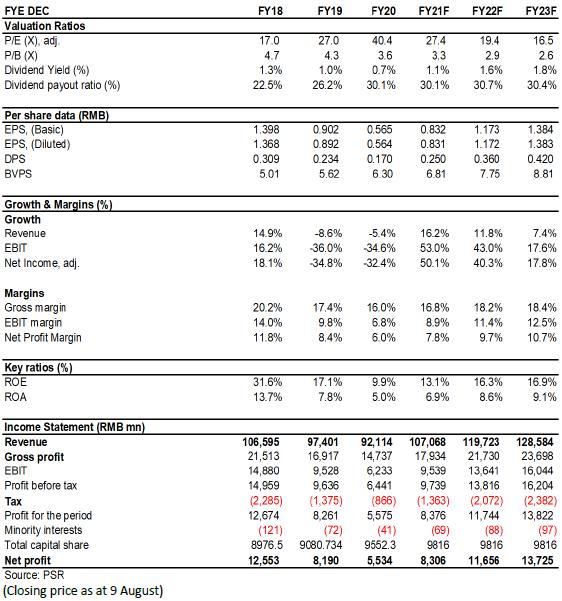

We revised our financial forecast and target price to HK$30.6, equivalent to 31/22/18.6x P/E ratio in 2021/2022/2023, and we give the rating of Accumulate. (Closing price as at 9 August)

Financials

Click Here for PDF format...