|

MENGNIU DAIRY(2319)

Analysis:

Mengniu (2319) continues to promote product innovation and upgrade and expanded online and offline channels for omni-channel development, stimulating the strong growth in the sales of mid- and high-end products. The revenue of the Group amounted to RMB45,905.2 million for the six months ended 30 June 2021, representing a year-on-year increase of 22.3%. Due to the increase in revenue and increase in operating efficiency, profit attributable to shareholders increased by 143.2% year-on-year to RMB2,946.5 million. In July 2021, Mengniu became a substantial shareholder of Shanghai Milkground Food Tech Co., Ltd. (600882.SH), which is a leading cheese company in China and has the most excellent research and development team and largest production capacity in China. The Group aims to expand its business into the domestic and global cheese market with enormous potential together with Milkground through business cooperation. (I do not hold the above stock)

Strategy:

Buy-in Price: $46.00, Target Price: $50.00, Cut Loss Price: $43.00

|

ZHONGSHENG HLDG(881)

Analysis:

Zhongsheng issued the interim results of 2021, reporting RMB87.36 billion in revenue, up 50.1% yoy; the net profit attributable to the parent company stood at RMB3.7 billion, up 61% yoy, with an EPS of RMB1.609. In July, the Company announced the acquisition of Zung Fu China, which is one of the largest Mercedes-Benz dealers in South China and West China. After the completion of the acquisition, Zhongsheng`s market share in the Mercedes-Benz brand will significantly increase by 6 ppts to approximately 18%, further strengthening the Company`s market position as the second largest dealer of the Mercedes-Benz brand. The business synergy and cost-saving effects after the acquisition are worth expecting.

Strategy:

Buy-in Price: $64.50, Target Price: $99.00, Cut Loss Price: $46.00

|

|

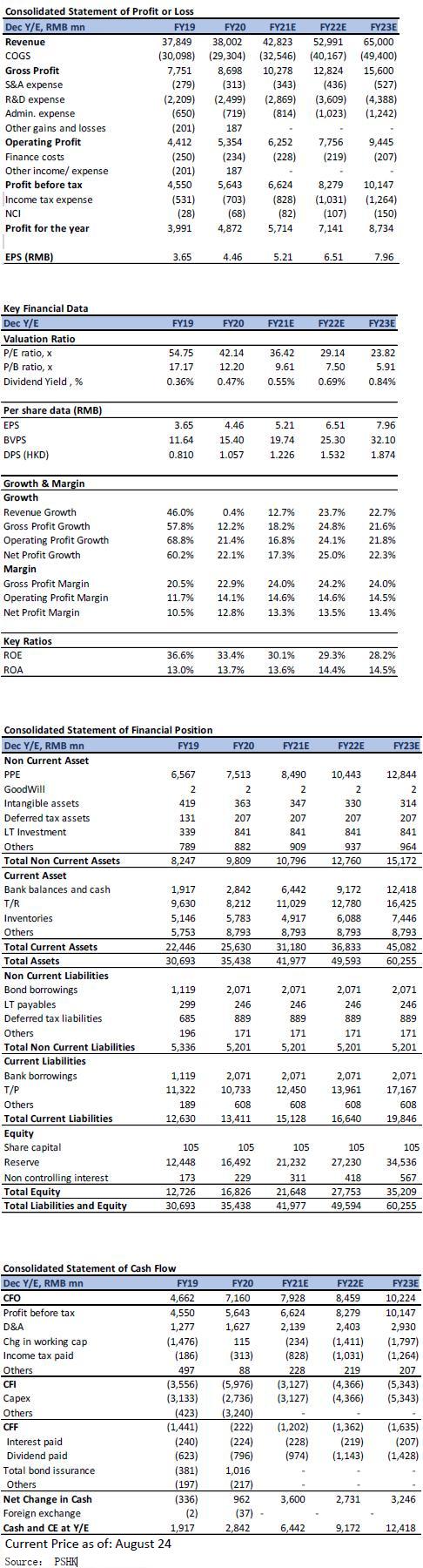

Sunny Optical Technology (2382.HK) - 1H21 GMP increase under downgraded specification of smartphone

Investment SummarySunny Optical announced the company's interim results as of 30 June 2021. During the period, the revenue was approximately RMB 19.833 billion (+5.1% yoy). The overall gross profit margin increased by 5.4 ppts yoy to 24.9% and the net profit attributable to the parent was approximately RMB 26.88 billion (+53.7% yoy). The company's revenue growth was lower than expected, mainly due to the downgraded specification of smartphone market landscape and unfavourable sales performance of high-end smartphone models, the average selling price of handset camera modules decreased significantly compared to the corresponding period of last year, which partially offset the revenue growth brought by the increased shipment volume. The company's net profit matches the market expectations, mainly benefited from the efficiency improvement and cost down of production brought by manufacturing optimisation and automation level improvement. Adjusted HLS shipment, short-term pressure on high-end products The company's shipment volume of HLS increased by approximately 11.1%, yoy in 1H21. The management has adjusted its guidance for HLS, from the expected annual growth rate of 15%-20% to 5%-10%. The shipment volume of HCM increased by approximately 34.5% yoy in 1H21, and the company maintains its forecast of 20%-25% yoy growth for the whole year. The trend of downgrading specification in the mobile phone market has caused short-term pressure on the company's high-end product market performance. The company's shipments volume of 6P and above HLS grew by only 2.9% yoy in 1H21. The overall shipment volume of periscope modules and large image size modules (chip surface at 1/1.7” and above) fell by 21.0% yoy in 1H21. At a result, the ASP of HLS dropped slightly yoy, while the ASP of HCM has dropped significantly. The company's management believes that the ASP in the second half of the year will still have a chance to be under pressure, but they are optimistic to the future business. In addition to the company's ability to optimize production lines, it has successfully digested the impact of changes in customer structure and gradually penetrates the Apple supply chain. It is believed that the mobile phone market will reappear in the trend of upgrading, and once it happens, the company will have an advantage. Automotive-related businesses exceed market expectation The company's automotive-related product revenue reached approximately RMB 1.614 billion in 1H21, a significant increase of 72.38% yoy, the shipment volume increased by 82% yoy, continuing to maintain its position with no.1 market shares. The company has raised its forecast for the shipment growth of VLS from 20%-25% to 30%-35%. In addition, the company has implemented mass production of light detection and ranging (LIDAR), transmitting and receiving modules and completed the R&D of the core optical engines for holographic AR HUD solutions. Company valuationConsidering the ASP of the HLS and HCM is expected to be under pressure in the second half of the year and the company's overall gross profit margin has increased, we slightly lowered the company's net profit attributable to the parent company for 2021/ 2022/ 2023 to RMB 5.714/ 7.141/ 8.734 billion, which 2021 – 2023 CAGR is 23.63%. We maintain the company's 2021 P/E ratio of 40x and slightly revise down the target price to HKD 245.1, corresponding to the PE ratio of 32.0x / 26.2x in 2022/ 2023. “Accumulate” grading is maintained. Financial

Click Here for PDF format...

| Recommendation on 30-8-2021 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 223.200 | | Suggested purchase price | N/A | | Target Price | $ 245.100 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2021 Phillip Securities (HK) Ltd. All Rights Reserved.

|