Sectors:

Air & Automobiles (Zhang Jing),

Consumer & Property Management (Timothy Chong)

TMT (Samuel Sung)

Automobile & Air (ZhangJing)

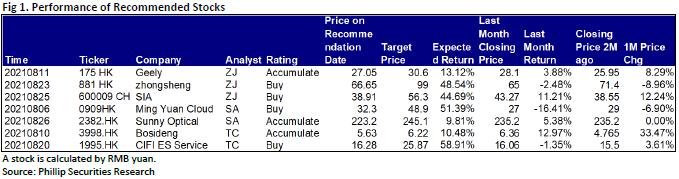

This month I released 3 updated reports of Geely (175.HK), Zhongsheng (881.HK) and Shanghai International Airport(600009.CH) which got success by their unique Competitive edge. Among them, we highly recommend Zhongsheng .

The pandemic's impact on China's car market had substantially reduced,but chip supply shortage was getting worse. As a result, monthly sales volume growth rate rose at the beginning and then gradually declined. Chip tightness puts pressure on the capacity utilization rate of OEMs, but it can also allow OEMs to recoup discounts and produce more models with high prices and high margins, which will benefit those car dealer group with platform advantages (such as Zhongsheng Holdings). Zhongsheng issued the interim results of 2021, reporting RMB87.36 billion in revenue, up 50.1% yoy; the net profit attributable to the parent company stood at RMB3.7 billion, up 61% yoy, with an EPS of RMB1.609. The main reasons of the increase in H1 are 1) The gross margin of new car sales increased due to the increase in the trading volume of new cars, especially that of the new brand premium cars, as well as the favorable supply and demand conditions. 2) The after-sales service admissions grew steadily, and the gross margin of after-sales service climbed. 3) Value-added service saw a growth driven by the increase in commissions for auto finance and second-hand car transaction business. Revenue from new car sales and after-sales business increased by 46% and 34% to RMB72,556 million and RMB11,302 million, respectively, from the same period last year. Second-hand car sales made a contribution of RMB3,503 million. Their respective proportions changed to 83.1%, 12.9% and 4% from 85.5%, 14.5% and 0, respectively, in the same period last year. The rapid development of the second-hand car business was supported by the Company's customer base of more than 6 million. In H1, the Company's transaction volume of second-hand cars reached 66,735 units, a yoy increase of 64.1%. In the future, the growth rate of value-added service and aftermarket business of second-hand cars will further accelerate with the gradual implementation of the policies on value-added tax reduction on second-hand cars, the complete removal of migration restrictions, and cross-provincial registration of second-hand car transactions in various places.

Consumer & Property Management (Timothy Chong)

I have released two update reports covering Bosideng (3998.HK) and CIFI EverSunshine Services (1995.HK) this month. Among them, we highly recommend Bosideng (3998.HK).

The company announced its annual report for the FY20/21 on July 21. Revenue increased by 10.9% Yoy to CNY 13.52 billion, which was lower than our expectation. The net profit attributable to the parent for the year was CNY 1.71 billion, an increase of approximately 42.1%, beat our expectations. It mainly due to the decrease in the company's expense ratio during the period and the increase in profitability. The company declared a final dividend of HKD 10.0 cents per share. The total dividend for the year was HKD 13.5 cents, with a dividend payout ratio of 70.8%.

During 2020, the company will mainly focus on handling inventory issues in FY2019/2020. During FY21, the company strategically reduced wholesale sales and actively adopted destocking measures. In addition, China was affected by the early winter and other climates last year. Solving inventory problems within the scope of controlled discounts has limited impact on profitability. The company's inventory level at the end of FY21 was CNY 2.65 billion, a Yoy decrease of 2.9%. The inventory turnover days increased by about 20 days to 175 days compared with last year. This was mainly due to the fact that the beginning inventory was affected by the epidemic, which was at a relatively high level, and the impact was about 12 days. In addition, in order to cooperate with the company's new replenishment measures, the proportion of raw materials in the inventory has risen sharply, accounting for 30% of the total inventory (16% in the same period last year), which will affect the inventory turnover days of about 8 days; if excluding raw materials, the company's inventory turnover days are about 127 days, and the company's long-term goal is 100-110 days (excluding raw materials).

The company will carry out product integration reforms in 2020 to improve the company's supply chain and inventory issues in the long run. It was mainly implemented in self-operated stores last year. In terms of distributing goods, in the first batch of distributing goods, for different stores and users, distributing goods according to their store status, and the quantity is also controlled below 30% of the expected sales; the implementation of quick return and replenishment, the products in store sold every day will be replenished the next day, quick sell and quick replenishment; further improve pull production, from the previous quick return to production 20-25 days to 5-7 days production, to achieve 10-day pull return orders; strengthen O2O ecology, both online and offline channels share the same inventory to further improve the efficiency of goods. The company plans to further implement the product integration policy to franchisees in FY22. In the future, franchisees only need to order the first batch when they place an order, and replenish the goods when the product is sold. In addition, the franchisee is also allowed to exchange new products before the specified period. It helps improve product efficiency on the one hand, and effectively improve terminal inventory levels on the other.

TMT (Samuel Sung)

This month, I have released 1 initiation report of Ming Yuan Cloud Group (0909.HK) and updated reports of Sunny Optical (02382.HK).

Sunny Optical announced the company's interim results as of 30 June 2021. During the period, the revenue was approximately RMB 19.833 billion (+5.1% yoy). The overall gross profit margin increased by 5.4 ppts yoy to 24.9% and the net profit attributable to the parent was approximately RMB 26.88 billion (+53.7% yoy). The company's revenue growth was lower than expected, mainly due to the downgraded specification of smartphone market landscape and unfavourable sales performance of high-end smartphone models, the average selling price of handset camera modules decreased significantly compared to the corresponding period of last year, which partially offset the revenue growth brought by the increased shipment volume. The company's net profit matches the market expectations, mainly benefited from the efficiency improvement and cost down of production brought by manufacturing optimisation and automation level improvement.

The company's shipment volume of HLS increased by approximately 11.1%, yoy in 1H21. The management has adjusted its guidance for HLS, from the expected annual growth rate of 15%-20% to 5%-10%. The shipment volume of HCM increased by approximately 34.5% yoy in 1H21, and the company maintains its forecast of 20%-25% yoy growth for the whole year. The trend of downgrading specification in the mobile phone market has caused short-term pressure on the company's high-end product market performance. The company's management believes that the ASP in the second half of the year will still have a chance to be under pressure, but they are optimistic to the future business. In addition to the company's ability to optimize production lines, it has successfully digested the impact of changes in customer structure and gradually penetrates the Apple supply chain. It is believed that the mobile phone market will reappear in the trend of upgrading, and once it happens, the company will have an advantage.

Considering the ASP of the HLS and HCM is expected to be under pressure in the second half of the year and the company's overall gross profit margin has increased, we slightly lowered the company's net profit attributable to the parent company for 2021/ 2022/ 2023 to RMB 5.714/ 7.141/ 8.734 billion, which 2021 – 2023 CAGR is 23.63%. We maintain the company's 2021 P/E ratio of 40x and slightly revise down the target price to HKD 245.1, corresponding to the PE ratio of 32.0x / 26.2x in 2022/ 2023. “Accumulate” grading is maintained.

Click Here for PDF format...