|

LEE & MAN PAPER(2314)

Analysis:

For the six months ended 30 June 2021, Lee & Man Paper`s (2314) total revenue increased by 37.1% to HK$15.2 billion as compared to the same period of last year. Resulted from the economies of scale and cost advantages, the profit for the period increased by 42.8% to HK$2.0 billion as compared to the same period of last year. In response to changes in the market, the Group has continued to consolidate upstream resources and develop a vertical business model covering pulp-making and waste paper recycling in order to integrate the industrial chain and ensure the supply of raw materials. At the same time, the Group has continued to expand its scale, control costs, and increase production capacity on the basis of its existing business. (I do not hold the above stock)

Strategy:

Buy-in Price: $6.90, Target Price: $8.00, Cut Loss Price: $6.40

|

SEMIR(002563.SZ)

Analysis:

Semir Garment (002563.SZ) is in a dual-leading position in the domestic casualwear clothing and children`s clothing industries. According to the China National Garment Association, the company ranks 8th in the national apparel industry based on 2019 operating income. In addition, according to euromonitor, balabala ranks first in the children`s clothing market with 6.9%, which is 5.3 pct higher than the second place, Anta Kid. The company announced its results for 1Q21. In 1Q21, it recorded revenue of CNY 3.31 billion, an increase of 20.9%; net profit attributable to parent was approximately CNY 353 million, an increase of 1916.8% Yoy, and a 1.7% increase from the same period in 2019. Excluding the impact of Kidiliz`s spin-off, the company`s revenue and net profit increased by 50% and 226% respectively Yoy. After spin off Kidiliz, the company has improved its cost control, and its overall revenue and profit performance are in line with our expectations.

Strategy:

Buy-in Price: RMB9.00, Target Price: RMB9.90, Cut Loss Price: RMB8.40

|

|

LI NING(2331.HK) - 1H21 results beat, core categories sell-through grew rapid

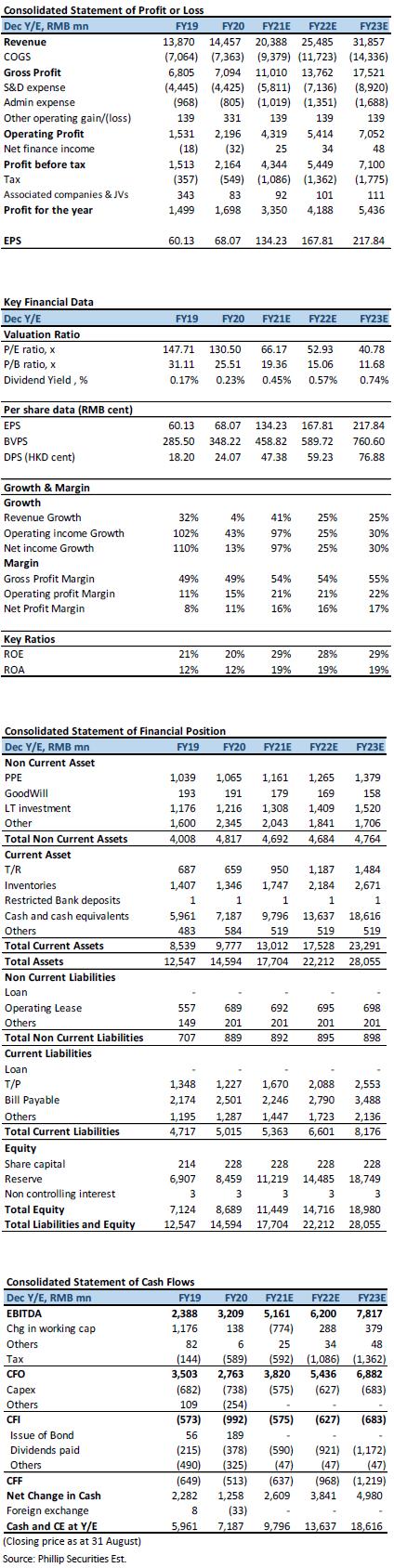

Investment summary Li Ning announced the company's interim results as of June 30, 2021. During the period, revenue increased by 65% Yoy to CNY 10.20 billion, overall GPM increased by 6.4 ppts to 55.9%, and net profit attributable to the parent recorded CNY 1.96 billion, a Yoy increase 187%, mainly due to the company's increased operating leverage, OPM increased by 10.4 ppts to 24.9%. The overall performance is better than the profit alert announcement. The company's operating performance continues to improve, and the cash cycle is further shortened by 17 days to 13 days. OPM improved significantly, and profit in 1H was better than expected From the perspective of retail sell-through growth, the company's overall sell-through (including online and offline) in 1H recorded a low-nineties growth, while offline channels recorded a high-eighties growth. The company's direct operating sell-through recorded an 88.5% growth, and the wholesale channel sell-through recorded a high-eighties. By category, the company's core category retail sell-through increased by 92% in total. Among the core categories, sports fashion/running/basketball category sell-through increased by 116%/87%/80% Yoy respectively. During the period, the company's revenue recorded CNY 10.20 billion, a Yoy increase of 65%, mainly due to the recovery of demand after the epidemic and the Xinjiang cotton incident to stimulate sales growth. Net profit increased by 187% Yoy to CNY 1.962 billion, mainly due to the company's significant Yoy increase in OPM by 10.4ppts to 24.9%; under operating leverage, NPM increased by 8.1 ppts to 19.2%. In terms of POS, the company's total number of POS decreased by 188 from the previous month to 6,745, among which Li-Ning brand POS decreased by 208, from 5,912 at the end of last year to 5,704 at the end of June. Li-Ning brand wholesale/direct-operated stores decreased by 147/61 respectively. Channels continued to optimize through opening large stores and closing low-efficiency stores, the overall store area still recorded a low double-digit increase despite the decrease in the total number of stores. During the period, the company's sales efficiency improved, and the overall inventory turnover months improved from 4.2 months at the end of last year to 3.1 months. In the inventory structure, new products with an age of 6 months or less accounted for 83% of the inventory at the end of the period. An increase of 5ppts from 78% at the end of last year; Among them, the proportion of inventories older than 12 months fell to 7%, an improvement of 2ppts from the end of last year, mainly due to the company's adjustment of new product handling policies, and the new products began to be cleared 3 months after they were put on the shelves. For promotion, the overall discount is controlled in the middle of 10%-20% off, and the 3-month sales rate of new products is mid-sixties. The management updated the FY21 guidance. The management raised the revenue growth to more than 40%. If calculated based on the revenue growth of 65% in the first half of the year, the revenue growth in the second half of the year is expected to be no less than 20%. The annual NPM was 16% to 17.5%. The revenue growth in the next 2 to 3 years is expected to exceed a CAGR of 20%. We believe that the updated guidelines are in line with our previous expectations. The excellent performance in the first half of the year is not expected to continue throughout the year, but the overall performance will still be improved compared to last year. Valuation and investment adviceThe company's revenue and profit side in the first half of the year were beat our expectations. The Xinjiang cotton incident brought opportunities to the company, brought short-term stimulus to product sales, and also brought opportunities for the company to upgrade its brand. In the first half of the year, due to the company's revenue growth and improved operating margins, the company recorded a high percentage increase in the profit side. As the company's revenue structure changes and brand image is established, the company's GPM is expected to further improve. The FY21/FY22/FY23 GPM is predicted to be 54%/54%/55%. In response to the first half of the performance, we adjusted the company's valuation model and raised the company's FY21/FY22 earnings per share forecast to CNY 134.23/167.81 cent (previously: CNY 130.08/146.26 cent). Move the target P/E one year later to FY2022 60x, and raise the target price to HK$118.45, which corresponds to 75.00/60.00 times the expected price-earnings ratio in 2021/2022, corresponding to the current price, and upgrade to Accumulate rating. Risk1) Another wave of epidemic 2) Weak consumer demand Financial

Click Here for PDF format...

| Recommendation on 3-9-2021 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 104.500 | | Suggested purchase price | N/A | | Target Price | $ 118.450 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2021 Phillip Securities (HK) Ltd. All Rights Reserved.

|