|

JIANGXI COPPER(358)

Analysis:

Jiangxi Copper (358) is the largest integrated copper production enterprise in the PRC and has established its industrial chain with core businesses in mining, ore dressing, smelting and processing of gold and copper, as well as sulphuric chemistry and extraction and processing of precious and rare metals. The Group recently announced the proposed investment in construction projects for annual productions of 100,000 tonnes of lithium copper foil, 220,000 tonnes of copper rod and 30,000 tonnes of casting material. After completion of the Investment and with its capacity reached, the Group`s position in the copper processing industry will be further consolidated and the Group`s market share in the copper processing field will be further expanded. (I do not hold the above stock)

Strategy:

Buy-in Price: $16.80, Target Price: $18.80, Cut Loss Price: $15.80

|

GDS(9698)

Analysis:

GDS (9698.HK) is the largest carrier-neutral data center service provider in China. The Company recently announced its unaudited financial results for the second quarter ended June 30, 2021. In the second quarter of 2021, net revenue increased by 38.9% year-over-year (“Y-o-Y”) to RMB1,863.9 million; net loss was RMB298.5 million, compared with a net loss of RMB101.0 million in the second quarter of 2020. The operating highlights indicated that the total area committed and pre-committed by customers increased by 44,848 square meters (“sqm”) in the second quarter of 2021 to 470,125 sqm as of June 30, 2021, an increase of 41.0% Y-o-Y (June 30, 2020: 333,461 sqm). Since the Company got several first-time orders with new strategic hyperscale customers, it will enhance the Company's customer base.

Strategy:

Buy-in Price: $54.00, Target Price: $64.00, Cut Loss Price: $49.00

|

|

Q Technology (1478.HK) - 1H21 profits exceed expectations, Future upgrade logic remains unchanged

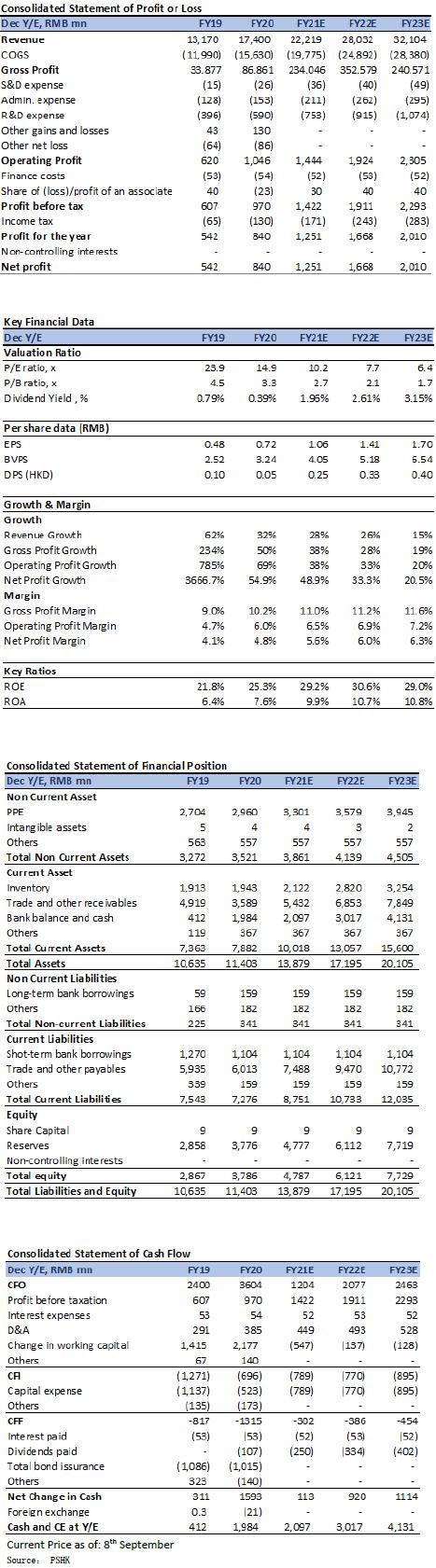

Investment SummaryQ Technology announced the company's interim results as of 30 June 2021. During the period, the revenue was approximately RMB 9.336 billion (+6.1% yoy), the gross profit was approximately RMB 1.083 billion (+47.9%), the gross profit margin was approximately 11.6%, an increase of about 3.3 ppts compared with about 8.3% in the same period. The company's net profit was about RMB 571 million (+70.1% yoy), which was higher than the 40%-60% guidance range of the company's positive profit forecast. In addition, excluding the company's initiative to impair the goodwill of Newmax Technology and the asset restructuring costs arising from the spon-off of Kunshan Q Technology China to A- share listing, the company's net profit will increase by 82.9% yoy. The company's net profit growth was mainly attributable to steady growth in the company's camera module sales, continuous improvement of its customer structure and the optimization of its camera module product structure. 1H21 Camera module shipments are lower than the company's expectations, Increasing proportion of high-end products The company's 1H21 camera module shipments were approximately 224 million units (+24.2% yoy). The company lowered the camera shipment target for 2021 given at the beginning of the year, from a yoy growth of not less than 30% to 25%, mainly due to insufficient supply of key components in the smartphone supply chain. For 2H21, the company remains optimistic, given camera module shipments a growth rate of 25.7% yoy and 19.2% mom growth. In terms of production capacity, the company maintains its monthly production target of 65kk at the end of 2021. In terms of product structure, the company's sales of 32 megapixel and above camera module products accounted for an increase of about 4.2 ppts to 32.4% of the total sales, which was slightly higher than the company's target of its shipment volume for the year not less than 30% of the total sales. However, the sales ratio of camera module products with 10 megapixel and above dropped by about 2.7 ppts yoy to about 70.8%. As a result, the company's average unit price of camera modules in the first half of the year fell by approximately 12.4% yoy from approximately RMB 42.8 in the same period to RMB 37.5 but it has increased by 6.5% from the average unit price of RMB 35.2 in the second half of 2020, reflecting a mom increase of camera module products. The unit price has returned to the upgrade track. We believe that the trend of lowering regulations and allocations of mobile phones in the second half of the year still exists, and the company is still under pressure to increase unit prices. However, the second half of the year is expected to enter the peak season of the traditional mobile phone supply chain and drive the sales of camera module products to increase mom. In addition, the unit price of the module continues to be close to the average unit price of the industry leader Sunny Optical (approximately RMB 39.2) and the industry recognition has been verified. Towards three strategic objectives for five-year For the next five-year plan, the company has put forward three strategic goals in terms of industry positioning, new segments and vertical integration: 1) To rank top 2 in terms of sales volume of CCm and FPM as well as top 5 in terms of sales volume in automotive CCM. 2) To pursue progress in the new segments such as automotive, AR/VR, smart home and target a quarter of revenue contribution coming from these new segments. 3) With module packaging and testing as the cornerstone, reach out and further integrate with upstream supply chain for the purpose to provide leading total intelligent vision system solution. We believe that the company's short-, medium-, and long-term customer marketing goals are clear. In addition, the smart phone camera upgrade logic remains unchanged, and the company continues to optimize the camera module product structure. Car cameras with high ASP are in the incremental market and are expected to replicate the mobile phone sales logic. Car camera modules have been certified by many car companies, including Geely automobile, BGMW, XPENG Motors. The company is also actively deploying in the IoT field and cultivating 6 types of segmented application, including drones, wearables, smart home, smart panel, laptop, AR/VR. Company valuationWe raise our net profit forecast for 2021/2022/2023 to RMB 1.251/ 1.668/ 2.009 billion, and the CAGR for 21-23 is 26.75%, mainly considering the trend of future mobile phone upgrades, the company's continuous optimization of product portfolio which the product mix leads to an increase in gross profit margin, and the layout of emerging business. We maintain the company's 2021 price-earnings ratio of 17.0x and raise the target price to HK$21.20, which corresponds to 17.0x/ 12.7x/ 10.6x per stock market in 2021/ 2022/ 2023, upgraded to “Buy”. (Current Price as of: 8th September) Financial

Click Here for PDF format...

| Recommendation on 13-9-2021 | | Recommendation | Buy | | Price on Recommendation Date | $ 12.720 | | Suggested purchase price | N/A | | Target Price | $ 21.200 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2021 Phillip Securities (HK) Ltd. All Rights Reserved.

|