Investment summary

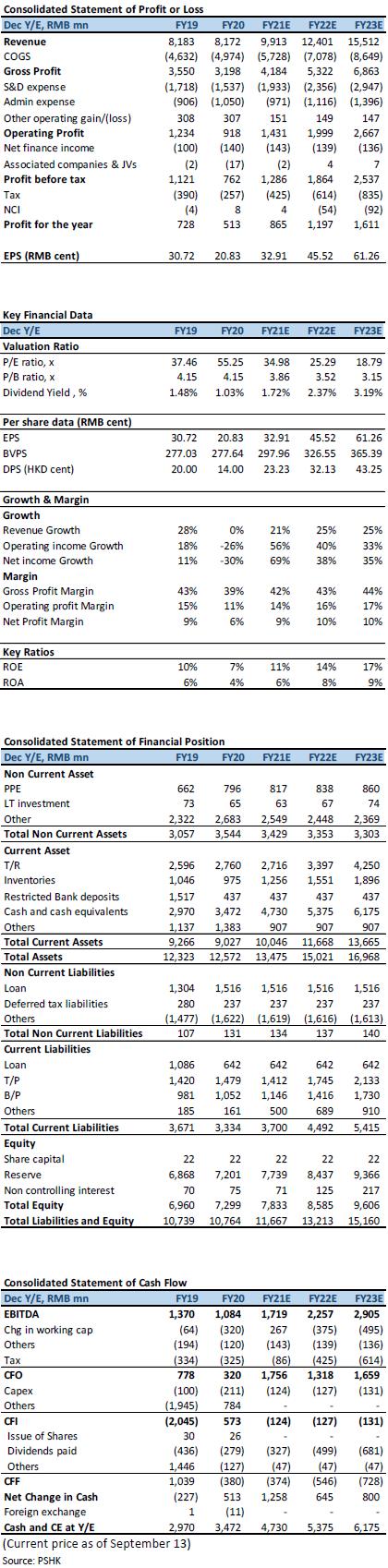

In1H21, the company's revenue recorded CNY 4.14 billion, an increase of 12.4% Yoy; net profit attributable to the parent company was CNY 427 million, an increase of 72.0% Yoy. The net profit margin for 1H was 10.3%, an improvement of 3.6 ppts Yoy, mainly due to 1) the improvement in GPM, and 2) the Xinjiang cotton incident brought organic traffic to the company's products and improved the expense ratio during the period. EPS recorded CNY 17.1 cent, an increase of 69.2% Yoy. Declared an interim dividend of HKD 11.5 cents per share, maintaining a dividend payout ratio of 60.0%.

The main brand's performance in 2021 further improves

The company's revenue in 1H was CNY 4.14 billion, an increase of 12.4% Yoy. In terms of brand groups, Xtep's main brand revenue recorded CNY 3.597 billion, an increase of 12.4% Yoy, accounting for approximately 87.0% of the group's total revenue. Driven by the Xinjiang cotton incident in 1H, the company's main brand turnover recorded a Yoy growth of 40%-45%, retail discounts were further changed to 7.5-8% (1Q21: 7-7.5%), and retail inventory turnover was further improved to the 4-month level ; Athleisure brands Palladium and K-Swiss recorded revenue of CNY 460 million, an increase of 0.7% Yoy, accounting for 11.2% of the group's total revenue, mainly due to the fact that overseas businesses are still affected by the epidemic and need time to deal with the uncertainty of the business environment; Professional Sports brands Saucony and Merrell recorded CNY 75.9 million in revenue, a significant increase of 289.5% Yoy, accounting for 1.8% of the group's total revenue, mainly due to the good progress of the company's channel expansion in the Mainland.

Improved profitability, new brands showing scale effect

In 1H, the Group's overall GPM improved by 1.3 ppts to 41.8% Yoy. By brand group, the GPM of Xtep's main brands increased by 1 ppts to 41.5% Yoy, mainly due to the inventory repurchase of wholesalers in the same period last year and no repurchase this year. ; The GPM of Athleisure brands Palladium and K-Swiss improved by 3ppts to 43.5% Yoy, mainly due to the increase in the proportion of direct e-commerce; while the GPM of professional sports brands Saucony and Merrell improved by 6.7 ppts to 45.4% Yoy, mainly due to increased sales , showing the scale effect. As of June 30, 2021, the company had a total of 6,015 Xtep main brand stores in mainland China and overseas, a decrease of 6 HoH , of which 428 were 9th-generation stores; during the period, Palladium and K-Swiss opened 3 stores respectively K-swiss` new products and new store image will be launched in China at the beginning of 2022. Saucony and Merrell have made good progress in opening stores during the period. As 30th June 2021, Saucony and Merrell have 36 and 6 stores respectively. It is expected to open about 10 stores in 2H, mainly in first- and second-tier cities.

The company's sales performance in 1H will be reflected in its revenue in 2H

The offline business of the company's main brand is operated in a wholesale mode. There is a 6 to 9-month delay in revenue recognition and retail sell-though. The main brand revenue in 1H mainly reflects the revenue of goods shipments in 2Q21 and 3Q21. It was carried out in December and January of this year. Due to the repeated of the epidemic, the dealers` ordering performance was relatively conservative at that time. The sales performance of 1H is expected to be reflected in the revenue of 2H. In the 4Q21 and 1Q22 order fairs held in April and July, dealers responded enthusiastically. The revenue and profit growth in 2H will increase significantly, which is expected to exceed 30%. The main brand Annual revenue will record a Yoy growth of more than 20%.

Athleisure brands Palladium and K-Swiss are currently mainly operating in Europe, America, Hong Kong and Taiwan, and related regions are still affected by the epidemic. The focus in 2H is to reorganize sales channels. The annual sales target for this year is approximately CNY 1 billion, and the expected loss is approximately CNY 100 million, which is narrower than the same period last year. K-Swiss has not yet generated revenue in China. It is expected that the situation will improve after the store opens next year, and the goal is to start to record profits in 3-4 years. Professional sports brands Saucony and Merrell expect annual sales targets of approximately CNY 170-180 million and a loss of CNY 40-50 million, mainly due to the failure to cover back-end expenditures due to low revenue generated. As the scale increases, profitability will improve in the future.

The five-year plan has clear guidelines, with channel expansion and product upgrade as the main goal

The company announced its fifth five-year plan. The management guides Xtep brand sales to grow at a CAGR of 23%. The goal is to reach CNY 20 billion by 2025. In terms of category, adult/child income will reach CNY 16.5 billion /3.5 billion by 2025, accounting for 83%/17%, with CAGR 21% and 37% growth respectively. The main driver for growth comes from product price increases and channel optimization. The number of offline stores increased by 30%, and the area of single stores increased by 40%. The average store efficiency will increase by CAGR 9%+. The new brand will grow at a CAGR of 30%, and the goal is to reach CNY 4 billion in 2025. If differentiated by brand, K-Swiss/ Palladium/ Saucony/ Merrell is expected to have revenue of CNY 1.6 billion/1.2 billion/10 billion/0.2 billion in 2025, respectively, corresponding to CAGRs of 25%/20%/70%/70%, and the main growth driver is the expansion of product channels.

Valuation and investment advice

The company's performance in 1H was outstanding, and it also announced a new five-year plan, which is in line with our expectations in terms of revenue targets. The main brand maintains its growth rate, while other brands have more aggressive growth targets. The growth driver mainly comes from the company's main brand product upgrades and channel expansion with other brands. At present, the company's new brand is still at a loss stage. Due to the impact of the epidemic, the expansion of the company's new brand stores was delayed. It is expected that the burden of the new brand development will be reduced after the epidemic situation is further eased. The company has continued to deepen the running field in the past years, and it has been recognized by users in the actual use environment. The company plans to deepen in the professional field and launch the main brand's Athleisure series. Driven by the national trend, we think it can improve The company's brand image improves the profitability of the company's main brand in the long run. We adjusted our previous revenue expectations. The revenue expectations for 2021/2022/2023 were raised to CNY 9.91/12.40/15.51 billion (previously: CNY 9.43/11.99/15.90 billion), and the company's EPS for FY21/FY22/ FY23 is expected to be CNY 32.91/ 45.52/61.26 cents (previously: 26.50/35.49/54.66 cents). Considering the company's future product development potential, the target P/E is increased to 35x FY2022, and the company's target price is raised to HKD 18.75 (previously HKD 7.79), corresponding to FY21E/FY22E/FY23E P/E of 48.43x /35.00x/26.01x, Upgrade to BUY rating.

(Current price as of September 13)

Financial

Click Here for PDF format...