Investment Summary

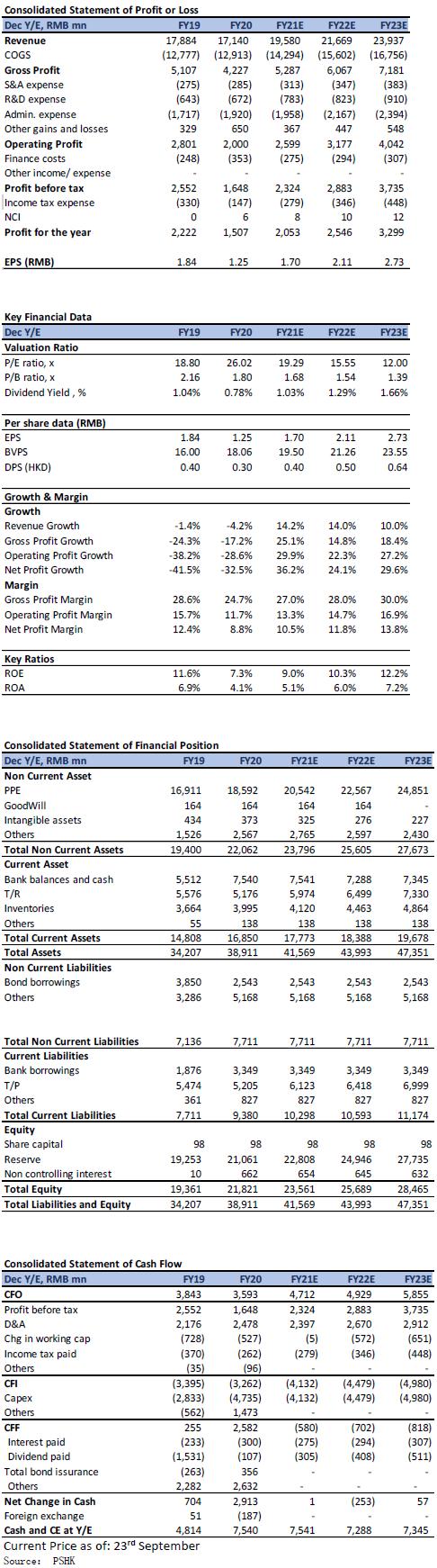

AAC Technology announced the company's interim results as of 30 June 2021. During the period, the Group's revenue was RMB 8.6 billion (+9.9% yoy and + 0.6% qoq). The gross profit was 2.4 billion (+32.8% yoy) and the gross profit margin was 28.1% (+4.9 ppts yoy). The Q2 gross profit margin was 25.0% (-6.1 ppts qoq). The net profit was RMB 921 million (+ 187.4% yoy and -26.9% qoq). The net profit margin was 10.7% (+6.6 ppts) and the Q2 profit margin was 9.0% (-3.4 ppts qoq). The company's performance in the second quarter was lower than expected, mainly due to: 1) the recurring epidemic in the second quarter, especially in Vietnam, 2) the shortage of upstream chips and insufficient capacity utilization of the company's overseas factories, 3) the average unit price of major customer products decreased.

The gross profit margin of acoustic products significantly dropped mom, the volume shipment of acoustic products on the Android client continued to increase

In 2Q21, the company's acoustic business revenue was RMB 2 billion (+7.0% yoy and -2.6% qoq). The gross profit was RMB 580 million (15.1% yoy and – 26.1 qoq) and the gross profit margin was 28.4% (+2.0 ppts yoy and – 0.9 ppts mom). The main reasons are: 1) The overseas epidemics have affected the normal production of Vietnamese factories and reduced the capacity utilization rate. It is expected that the unfavorable lagging impact on production will continue in the third quarter; 2) The peak sales season of major customer Apple has passed which leaded the unit price of acoustic products decreased seasonally. The outlook for the acoustic gross margin in the second half of the year remains cautiously optimistic, mainly due to: 1) it is expected that the epidemic in Vietnam, Malaysia and other regions will ease in the fourth quarter, and production capacity will return to normal; 2) The second half of the year is the peak season for the traditional mobile phone market. The launch of new models of Apple mobile is expected to increase the acoustic gross profit margin; 3) The gross profit margin of the acoustic products of the Android client continued to improve from the previous mouth. The company upgraded the standardized small cavity acoustic module, and has penetrated into the customer's mid-to-high-end models. It helps to extend the life cycle of the product production platform and reduce unit costs through economies of scale to increase gross profit margin.

Revenue is growing rapidly in optical business, WLG technology enters the automotive industry

In 2Q21, the company's optical business revenue was RMB 807 million (+ 112.3% yoy and +19.7% qoq). The gross profit was RMB 178 million (+ 235.8% yoy and -5.3% qoq) and the gross profit margin was 22.0% (+8.2 ppts yoy and -5.8 ppts qoq). The gross profit margin of 2Q20 was 13.8% while the gross profit margin of the optics for the whole year reached 21.4% in 2020. The company's continued increased in gross profit margin in the optical business was mainly due to: 1) the market share of plastic lenses continued to grow. In 2Q21, the shipment volume of plastic lenses reached 171 million (+67.6% yoy and +9.6% qoq). At the same time, due to the further improvement of the company's operation and production management level, the unit cost of plastic lenses continued to decrease compared with the previous quarter, offsetting the adverse effects of the decline in average unit prices. However, the gross profit margin of plastic lenses in the second quarter still fell slightly by 2.9% to 33.4%; 2) The group continued to optimize the product structure and shipment volume, leaning toward higher-end products, of which 6P lens shipments accounted for 13.0%; 3) The WLG glass-plastic hybrid lens product (1G5P) was launched on the market and received positive feedback from customers. It is expected to accelerate the introduction of glass-plastic hybrid lens in high-end flagship mobile phone projects. It helps to increase the company's market share in the optical lens industry, and has been actively discussing the application of 1G5P and 1G6P in high-end mobile phones with customers.

In June 2021, the company announced that it has completed its equity investment in Ibeo Automotive Systems GmbH (Ibeo) and have established a strategic partnership. Ibeo is a manufacturer with leading laser radar (LiDAR) technology. In 2020, it became the first company to be nominated by Great Wall Motors for mass production of solid-state LiDAR, and it has also become one of the major suppliers in the autonomous driving market. This transaction indicated the company has officially entered the automotive industry. The company is currently deploying new products such as in-cabin automotive lens development. It is also actively contacting mainstream (Tier 1) and new car manufacturers customers to improve the company's optical, especially proprietary wafer-level-glass (WLG) technology and its high-precision manufacturing platform and other processes can be better introduced into the automotive field.

Horizontal linear motor shipments increased for Android client's, the climbing stage of new product of metal frame

In 2Q21, the company's electromagnetic drives and precision mechanics, combined segment business achieved revenue of RMB 1.218 billion (-29.4% yoy and -0.8% qoq). The gross profit was RMB 270 million (-31.3% yoy and -13.7% qoq) and the gross profit margin was 22.1% (-0.6 ppts yoy and -3.4 ppts qoq). The market penetration rate of the company's haptic feedback solutions in 2Q21 has further increased. The Android client horizontal linear motor shipments have increased by more than 400 yoy. Through the integrated solution of “Hardware + algorithm”, it can realize short-term start and stop, superimposed vibration tactile feedback, and provide customers with a differentiated tactile experience. It is expected to promote the needs of customers for product upgrades and update iterations, which will help drive the annual growth of horizontal linear motor shipments for the company.

In terms of precision structural parts, as the new metal frame products are still in the climbing stage, the gross profit margin has declined. On the other hand, they have successfully expanded more customers portfolios and imported into the laptop and tablet computer structural parts market. With the increase in the penetration rate of metal structural parts in multiple markets, it is estimated that its laptop and tablet computer business revenue will exceed 10% of the revenue of precision structural parts, bringing further room for growth in the company's segment business.

Increased the installed capacity of MEMS microphones, expanding multiple vertical fields

In 2Q21, the company's micro-electromechanical system device (MEMS) business revenue was RMB 238 million (-7.9% yoy and -15.9% qoq). The gross profit was RMB 38 million (-7.3% yoy and 19.1 qoq) and the gross profit margin was 15.8% (-0.2 ppts yoy and -0.8 ppts qoq). With the increase in the number of MEMS microphones installed on a single smart phone, and the popularization of wearable devices and smart home products, the market scale is expected to continue to expand. The company will seize the market opportunities of the continuous development of IoT, and the trend of specification upgrade requirements such as true wireless Bluetooth (TWS) headsets and laptop computers, and increase the market penetration rate of the company's MEMS products.

Company valuation

We lowered our net profit forecast for 2021/ 2022/ 2023 to RMB 2.053/ 2.546/ 3.300 billion, and the compound annual growth rate for 21-23 is 26.8%. The main consideration is that the company's annual gross profit margin failed to remain in the first quarter, but most of its business has begun to import the Android customer market, and it has also entered the automotive market in the fast-developing optical business. Therefore, the company maintains its 2021 P/E ratio of 25x, and lowers the target price from 63.0 to HKD 49.95, which corresponds to a stock-earnings ratio of 25.0x/ 20.2x/ 15.6x in 2021/ 2022/ 2023, and is upgraded to a buy rating.

Financial

Click Here for PDF format...