Investment Summary

CRP aims to build 40GW renewable power capacity during the 14th fifth five year planning period, around 3.57x times of the 11.2GW attributable capacity in operation at the end of 2020. Renewable segment would contribute over 75% of the earning by 2025E, a meaningful transformation to renewable energy from just 38.9% contribution in 2020. We issue a price target of $33.4 HKD for CRP, with the consideration of 1) Earning growth forecast of 13.6% CAGR during the 14th fifth period 2). P/E rerating as renewable companies listed in the HKEX market have a higher multiple. Positive factors not reflected into our target price include 1) Potential pricing premium on renewable electricity through the Green Energy Trading Pilot Scheme, 2). Electricity price differential widening during peak demand hours potentially drive higher revenue on thermal power electricity, & 3). A-share listing prospect.

40GW Renewable Energy Installation Target during 2020-2025, a Meaningful Roadmap toward Renewable Energy that deserve a higher multiple.

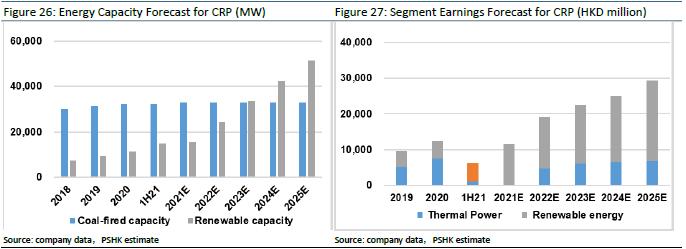

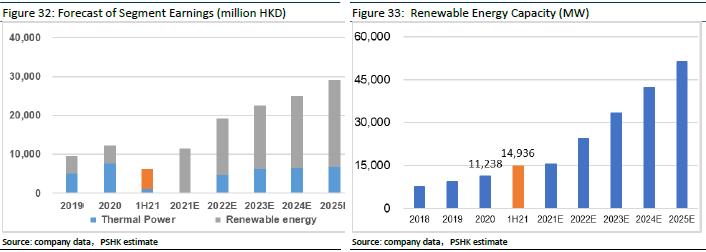

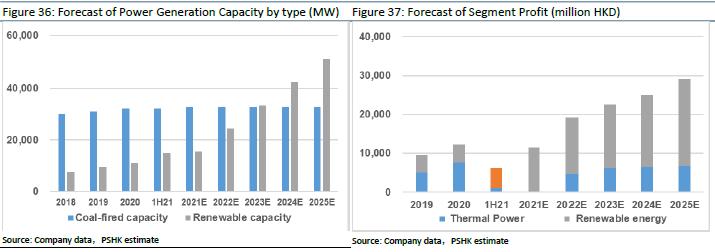

Profit from renewable segment increase 70.5% yoy from $3b HKD in 1H20 to $5.11b HKD in 1H21, mainly from the increase on new capacity. Factoring in the 14th fifth planning period target of 40GW, we expect renewable segment profit to print a 36.5% CAGR during 2020-2025. We forecast renewable segment profit to contribute over 75% of total profit by 2025, drive an upward revision on trading multiple closer to the renewable energy companies listed in the HK market. We view CRP's current financial position is sufficient to meet an estimated 30-35 billion HKD CAPEX spending per annum, risk of equity financing in the HK market is remote.

Power Electricity Giant absent from the A-share Market. Heavy Spending on Renewable Projects present a Perfect Timing for A-Share Listing.

We expect CRP to spend over $150 - $175 billion HKD during the 14th fifth period to meet the 40GW renewable target, an estimated 43% to 67% increase over $104.9 billion HKD spending during the 13th fifth period. We view the amount of spending is achievable without equity funding, an A-share listing is still possible if CRP plan to invest more aggressively. Equity financing in the HK market is unlikely in my view, given 1). A-share listing could raise fund with much lower share dilution. Peers listed on both HK and A shares market, Datang, Huaneng and Huadian, their average A/H share premium is 1.16x times based on close price on Sep 15, 2021. 2). CRP current P/B ratio is still just slightly above 1 even with the recent outperformance compare to the market of 157.32% return in the last 1-year. If the norm for equity funding at P/B > 1 do applied, share price fluctuation could be a big uncertainty. We view a HK market equity funding is not as practical as an A-share listing.

Rising Coal Price could tamper with Thermal Power Profitability this year, but Solid Renewable Energy Prospects still remain during the 14th Fifth Period.

Coal prices rises sharply, we expect thermal power segment to have near-zero profit in 2021. We view thermal power profits to partially recover in 2022, because part of coal electricity supply is sold under a direct purchase arrangement with pricing adjustment mechanism by the end of the year to reflect rising coal price. Over the 14th fifth period, thermal power segment expects to grow modestly with rising utilization hours, while renewable segment expected to record a profit CAGR of 36.5% over that period. We recommend to look through the near-term challenge of rising coal price while focus on the positive prospect of aggressive transformation to renewables.

Earning Forecast and Investment Recommendation

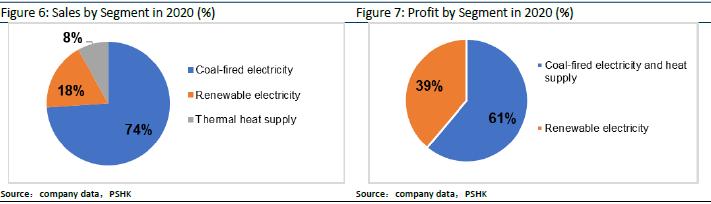

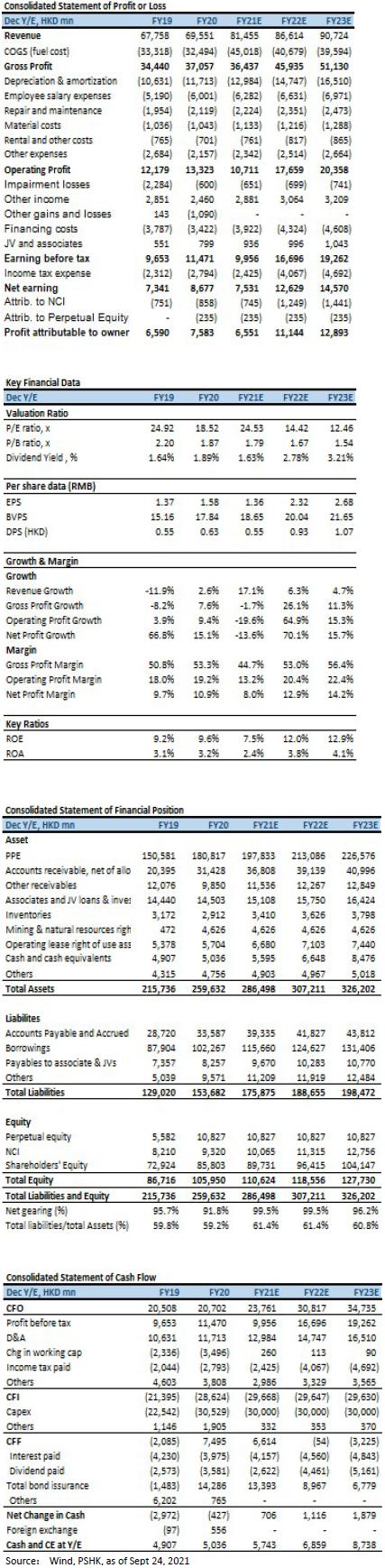

The three major segments: traditional thermal power, heat supply and renewable power generation accounted for 74%/8%/18% of total revenue respectively in 2020. Operating income in 1H21 was 42.23 billion HKD, a yoy increase of 35.4%. We expected thermal power will grow modestly, except for the short-term negative impact caused by the sharp spike on coal price. CAPEX spending on renewable projects will accelerate profit growth and reduce the impact of coal price movement on earnings. Our target price for CRP in 2021 is at $33.4 HKD, which corresponds to a P/E ratio of 24.5x/14.4x/ 12.5x for 2021/2022/2023 EPS. It is covered for the first time and is given a BUY rating.

Company Profile

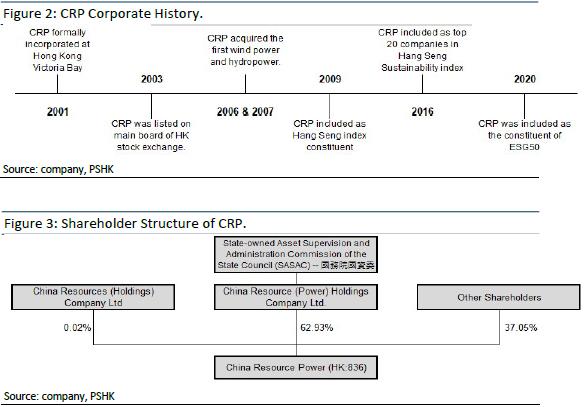

China Resources Power was incorporated in 2001, and it was listed on the Hong Kong Stock Exchange in 2003. CRP revenue mainly comes from thermal power, wind power, hydropower, and photovoltaic power generation. CRP power plants are located across the country. CRP exited the majority of its coal mining business in 2018 and begin to meaningfully increase investment on renewable energy started from 2019.

Company History:

CRP was incorporated in Hong Kong in 2001. In 2002, through the acquisition of three power plants located in Wenzhou, Hubei and Guangdong, the company became an independent power generator in China. In 2003, CRP was listed on the Hong Kong Stock Exchange. In 2006 and 2007, the first wind power and hydropower projects were established through acquisition and in-house R&D development respectively. In 2009, the Hunan branch was established, marking the first step in the reform of China Resources Power's regional branch. In the same year, CRP become the first Mainland China power company eligible for the inclusion into Hang Seng Index In 2010, the company first achieved a supply of power generation, steam, hot water, and refrigeration through technological transformation, becoming a regional distributed energy project. In 2018, the company established power sales and integrated energy services " "Lingxi" brand.

Key Operational Metrics:

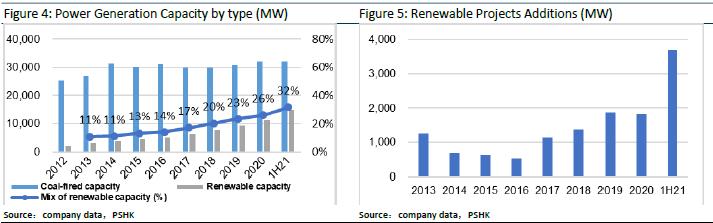

CRP operates thermal coal power and renewable power generation businesses. Heat supply business is to utilize the residual heat from thermal power plants. As of June 30, 2021, CRP's attributable capacity amount to 47,063 MW. Thermal power capacity is at 32,127 MW, accounting for approximately 68.3%; wind power, hydropower and photovoltaic power capacity totaled 14,936 MW, accounting for 31.7%. CRP planned to increase CAPEX investment on renewable projects to meet its 14th fifth development target of 40GW and to align with the policy direction of carbon neutrality and de-carbonization in China. In terms of geological exposure, it is mainly concentrated in East China, Central China and South China.

Renewable Capacity accounts for a Rising Proportion of CRP Total Capacity.

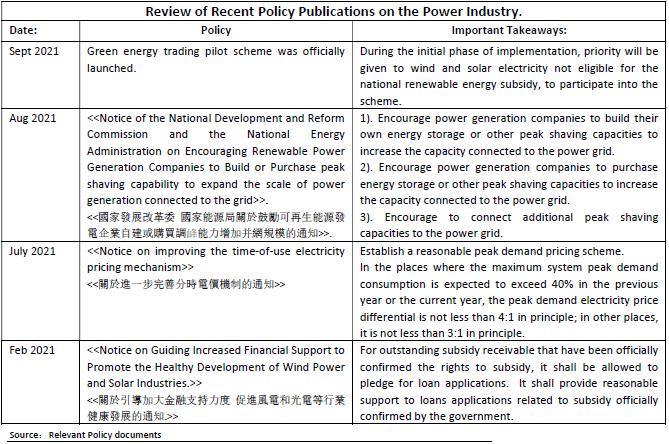

CRP plans to add 40GW of renewable capacity within 2025. Renewables will account for more than half of the total capacity at the end of 2025 from just 32% of total capacity at the end of 2020. Proportion of renewable capacity have increased from 23% in 2019 to 26% in 2020, and the mix shift have further accelerated to 32% in 1H21 just half a year. We expect during the 14th fifth period, CRP would incur a CAPEX spending of $30-35 billion HKD per annum. Debt ratio expect to increase slightly during that time but remain within a controllable range.

CRP begin Expanding Investment on Renewables in 2019 and exited Majority of Coal Mining Business in 2018. It improve Earning Growth Visibility and reduce Earning Impact from Rising Coal Price.

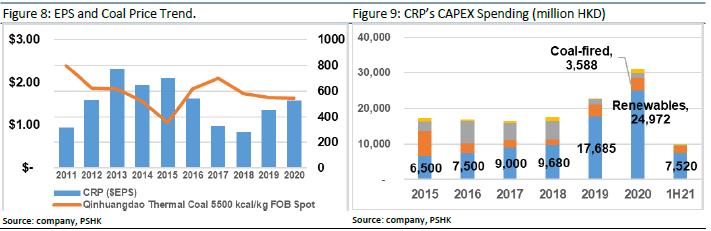

From 2011 to 2017 (figure 8), coal price movement is one of the primary drivers on CRP earning per shares. Breaking it down into rising and falling coal price periods; From 2011 to 2015, decline on coal prices led to a decline on fuel costs and rising profit. From 2015 to 2017, rising coal prices brought pressure on the cost side and led to a decline in profit. In 2018, a significant decline in (accounting) net profit was mainly due to the one-time impairment loss recognized from the disposal of coal mine assets. From 2018 to 2020, although coal prices remain at a similar level, more solar and wind capacity begin operation contributing to a stable growth on earning.

About 50% of the total electricity generated is sold through a direct-supply contract, and we assume a similar proportion of direct supply contract for coal-fired electricity. Under direct power supply contract, electricity price for the next year will be reset at the end year of this year to reflect current level of coal price. If coal prices record a significant increase during a year, thermal power companies generally are unable to pass on the rising cost to end users. Increasing the mix of profit contribution from renewables will be able to smooth out the earning uncertainties caused by the fluctuation on coal price.

Increase CAPEX Investment on Renewables expect to drive Earning Growth during the 14th Fifth Planning Period.

CRP expects to build 40GW renewables by 2025, in which renewables capacity is expected to surpass thermal capacity. 40GW renewables capacity is about 3.51 times of current capacity of 11.2GW from the end of 2020, we believe it will reduce the earning uncertainties of CRP related to coal price and potentially entice a P/E rerating. In the past, CRP have used a minimum IRR threshold of about 8-9% for investment.

Relevant Government Policies on the Power Industry

We view the policy direction is friendly toward renewable energy, while the existing stock of thermal capacity will also grow modestly. Hydro, solar and wind are weaker reliability of supply, in terms of intermittence and adjustability, than thermal coal power. During the transitional phase toward renewable energy, while battery storage solution is still a costly option, thermal coal power remains an important role in peak demand shaving to ensure stability of the power grid supply. For example: the policy to reasonably widen the electricity price differential between peak demand and regular time <<政策合理拉大𡶶谷電價價差, 將會利好火電作為調𡶶能源角色>>, which will benefit thermal power operator providing peak shaving capability. Green power trading scheme platform allows electricity companies to directly supply their renewable electricity at a premium to the end users. Recent policy statement encourage financial institutions to increase their financing support to renewables energy companies.

Green Energy Trading Pilot Scheme launched on Sept 2021. Renewable Electricity can be sold at a Premium through Direct Transaction with the End Users, to reduce the Interest Burden on Subsidy Delays.

Green power trading scheme at the current phase only include renewable projects not eligible for renewable subsidy from the government development fund. According to Xinhua News Agency data, pricing of the first batch of green power trading on September 7 is about 0.03 yuan-0.05 yuan/kWh higher than the mid-to-long-term transaction price, that represent an 8-10% pricing premium compared to the benchmark electricity price of desulfurized coal in their local areas. Large corporations are willing to switch onto renewable energy consumption to fulfill their corporate social responsibility (CSR) at a premium to standard coal-fired electricity. The trading scheme is currently under pilot testing, therefore positive contribution from the scheme is limited.

Policy statement is to Reasonably widen the Pricing Differential during Electricity Peak Demand, and it is expected to slightly improve profitability on thermal coal unit through higher pricing during peak demand.

During the 14th fifth period, policy goal is to increase the proportion of renewable electricity from about 11% to about 16.5% mix by 2025. Reliability of power supply from solar and wind power generation is weaker, and thus it will cost more to ensure stability of supply from the power grid. Electricity consumption is relatively concentrated on several timeslots, intra-day fluctuation of power demand is high. Establishing time-of-use electricity pricing mechanism will enable power grid companies to pass on the higher operating cost to end users, that is to entice a power consumption habit to reduce the overall cost of power generation. For thermal power operators, widening price differential during peak hours is expected to be positive as it is lifting the floor price on peak demand electricity.

Thermal Power Capacity could adjust to the Shortfall and Surplus of Electricity Supply allowing more Renewable Capacity to be connected to the Power Grid.

Thermal power and renewables are not mutually exclusive, power grid cannot solely rely on renewables with low adjustability on power output. If power supply is insufficient at a certain point in time, solar and wind energy is not able to react with increased electricity output that would leads to blackout. Government encourages simultaneous construction of 1). Backup power and 2). Power storage capacity to address this issue. According to << Notice of the National Development and Reform Commission and the National Energy Administration on Encouraging Renewable Energy Power Generation Companies to Build or Purchase peak shaving capacity to increase the Scale of Grid Connection >> The document encourage renewable players to build peaking shaving capacity equivalent to 15% output (duration of 4 hours or more) of the renewables capacity they intend to build, more than 20% peaking shaving capacity will be given priority for grid connection. Thermal coal backup capacity is needed to ensure reliable power supply if more renewable capacity need to connect to the grid. In 2021, the guaranteed amount of renewable capacity quota eligible to be connected to power grid will no less than 90 million kW that is below 120 million kW new capacity connection in 2020. Access to coal-fired back up capacity is important for renewable companies to ensure priority access to the grid connection beyond the guaranteed amount of quota. That will likely benefit power companies with thermal coal capacity over renewable-only players.

Demand and supply on electricity industry during 14th fifth period.

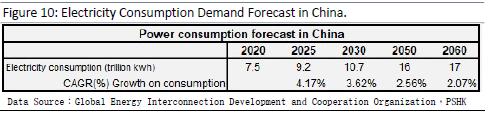

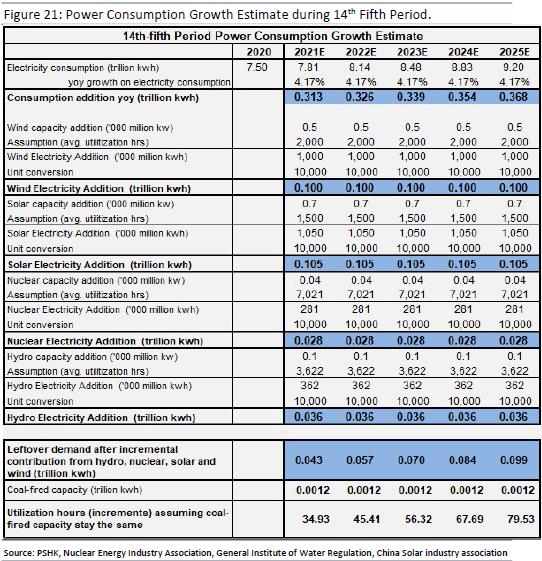

During the 14th Fifth Period, Electricity Consumption expect to grow at 4.17% CAGR.

Global Energy Interconnection Development and Cooperation Organization estimate during the 14th fifth period, electricity consumption growth in China will be at 4.17% CAGR. Electrification of automobiles will bring new growth momentum on power consumption. According to forecast from the Global Energy Internet Development Cooperation Organization, electricity consumption in China will increase from 7.5 trillion kilowatt-hours in 2020 to approximately 9.2 trillion and 10.7 trillion kilowatt-hours respectively in 2025 and 2030. By 2050 and 2060, total electricity consumption will reach approximately 16 trillion and 17. Trillions of kilowatt hours.

2025 Outlook on Renewable Energy.

New build of renewable capacity expects to contribute most of the incremental power consumption during the 14th fifth period. From our own calculation based on growth forecast from relevant industry associations, new construction of solar and wind energy projects will be able to provide about 2/3 of the incremental power consumption per annum during 14th fifth period. Coal-fired electricity would be one of the energy sources to fill the electricity consumption growth.

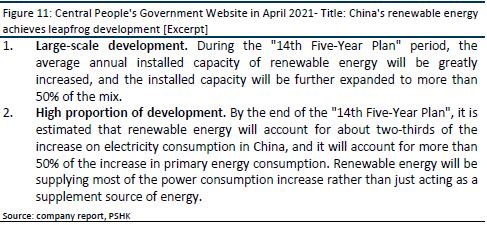

China's Renewable Energy Power Generation Capacity is expected to reach more than 50% of the Total Mix by the end of 2025.

China's total installed renewable capacity accounts for 42.4% of the total energy capacity, which increased by about 14.6% compare to 2012. According to statements issued by the National Development and Reform Commission on April 2, 2021 "To achieve leapfrog development for China's renewable energy", it is estimated that by the end of 2025, the proportion of renewable energy power installed capacity in China's power generation capacity will exceed 50%. Electricity consumption in China continues to shift toward wind and solar, which provide positive outlook for the renewable space. However, installed base of renewable capacity > 50% of the mix is not the same as power generation exceeding 50% of the total power generation. The main reason is average utilization hours of solar and wind energy are much lower than that of thermal power. The actual power generation shall be formulated by = Utilization hours x equipment scale (ex: 500MW).

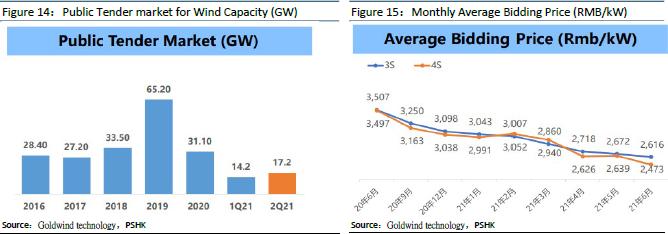

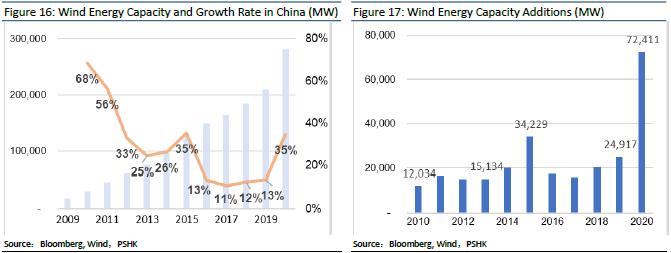

Industry Representative predict Installed Base of Wind Energy to reach at least 800 million Kilowatts (800GW) by 2030.

According to the "Beijing Declaration on Wind Energy" jointly issued by representatives from wind energy companies in October 2020, during the 14th Five-Year Plan period, they guarantee to build an at least 50 million KW of wind energy capacity per annum. After 2025, China's average new installed capacity of wind power should not be Less than 60 million kilowatts per annum. By 2030, the total installed base of wind power capacity will be no less than 800 million kilowatts, and by 2060, no less than 3 billion kilowatts. According to the public data published by GoldWind Technology, the national public bidding of wind power capacity amount to Q1-14.2 GW, Q2 — 17.2 GW, which is roughly in line with the 50 GW annual target from wind energy industry representative.

Total Cost of Wind Power Capacity is more expensive than Solar. However, if adjusted for Difference in Utilitization Hour, the Investment Cost per Kilowatt-Hour Electricity is about the Same.

According to relevant data from the industry peers, total CAPEX spending on wind power and solar power generation capacity [including installation, construction, etc.] is approximately $6,000 and $3,000-$4,500 per kilowatt. The higher pricing of wind capacity per KW is not necessarily worse than solar, considering solar capacity utilization hours are much lower than wind power. Using their respective national average utilization hours of 1,160 hours and 2,097 hours for solar and wind capacity, the investment cost per kWh electricity is competitive between wind and solar energy. We view the short-term factors affecting the amount of investment depend on 1). The availability of wind resources across the country. 2). the regional government's planning for renewable energy.

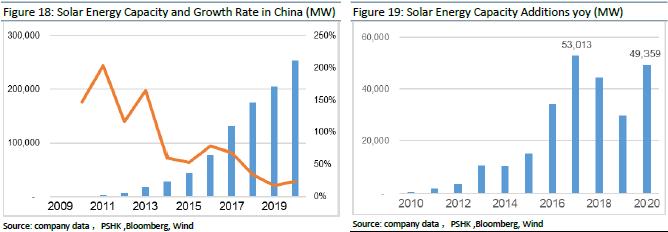

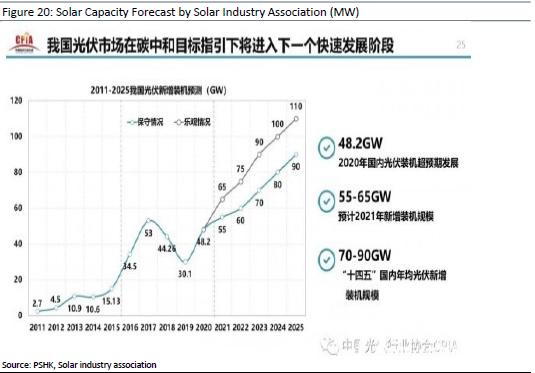

Installation Rate of Solar Capacity expect to accelerate during 14th fifth Period.

The China Photovoltaic Industry Association predicts that during the ൖth Five-Year Plan" period, the average annual installation rate of domestic photovoltaic capacity is about 70-90GW. According to <>, the national wind power and photovoltaic power electricity generation is expected to increase from about 11% in 2021 to about 16.5% in 2025.

Solar Energy Installation include from both Distributed and Centralized Projects, Distributed Projects will no longer eligible to Subsidy.

According to data from the National Energy Administration, solar capacity installation in the first half of 2021 was 13.01GW, of which, centralized photovoltaic projects was 5.36GW, and that of distributed photovoltaic projects was 7.65GW, accounting for approximately 41.2% and 58.85%, respectively. Beginning on August 1, 2021, the <> will be implemented in 2021 for newly filed centralized photovoltaic power plants, industrial and commercial distributed photovoltaic projects, in which the central government will no longer subsidize new projects. This will likely have downward pressure on capacity pricing.

Forecast of Thermal Power Demand Growth during the 14th Five-Year Plan Period,:

Limited increase on nuclear power and hydropower generation is expected during the 14-fifth period due to long construction cycle.

A. According to the Blue Book of the China Nuclear Energy Development Report (2021) issued by the Nuclear Energy Industry Association, the operating capacity of nuclear power units will reach 70 million kilowatts by 2025. Compared with the 50 million kilowatts capacity at the end of 2020, it represents an increase of 20 million kilowatts.

B. According to the data of the China Renewable Energy Development Report released by the General Institute of Water Regulation in June 2021, the scale of hydropower under construction in China is about 48 million kilowatts. A typical hydropower unit will take 5-7 years of construction. Therefore, we believe that the capacity growth during the 14-fifth period will not exceed 50 million kilowatts.

Future Development of Thermal Power Energy expected to remain Stable.

Market is concerned with the future development of thermal power; that is due to a misconception on solar and wind energy to replace coal-fired plants, and do not recognize the installation of solar and wind energy capacity per annum is insufficient to meet the incremental electricity consumption demand in China. Power companies are increasing investment in renewable energy power generation especially during the 14th fifth five-year planning period, it expects to only meet 2/3 of the demand increment per annum. Thermal power will fulfill part of the new consumption demand on top of existing electricity output. Therefore, the utilization hours of the existing thermal power assets would remain stable to some extent a small increase. The projection shall clear investor concern on coal-fired plants utilization as renewable energy will be given a priority in the case of electricity surplus. According to < 2016-In the case of limited power demand, the supply of renewable energy (non-fossil energy) power generation projects will be given priority. We view the investor concerns are unnecessarily given renewable energy alone is unable to fulfill incremental consumption demand.

Supply of New Coal Power Plants is expected to be Relatively Limited

Our view is during 14th fifth period will extend tightening policy measures on thermal power capacity during the 13th fifth period; 1) Eliminate outdated or inefficient production capacity and 2). Optimize existing production capacity. In the future, new thermal projects will likely come in more complex form combining with other energy sources, such as solar, wind and energy storage rather than just as a standalone thermal power plants. During 13th fifth period, policies have been relatively strict on new thermal power projects. For example: Since 2017, policy statement released "Opinions on Promoting Supply-Side Structural Reforms to Prevent and Resolve the Risk of Overcapacity of Coal Power", "Government Issues Risks in Coal Power Planning and Construction Early warning, the principle is to provide appropriate and orderly reception, classification and guidance of the approval and construction of self-use coal power projects in various regions." To reduce the construction of new coal power production capacity. In 2019, the National Development and Reform Commission and the Energy Administration jointly issued <>, including the elimination and shutdown of 1) coal-fired units that cannot be retrofitted for heating distribution supply. 2). Units which coal or water thermal efficiency is still not up to the standard after upgrade. Our view is new construction of coal-fired power plants in the future will be limited, and thus will slightly increase the utilization hours of the existing thermal power.

Factors that moved Share Price:

Renewable energy sector has entered a phase with zero subsidy (grid parity) started from 2021, and new construction projects will no longer be eligible for subsidy. Existing capacity connected to the grid under subsidy scheme will remain eligible for subsidy. Because grid-parity projects have no subsidies, and thus will not be affected by the delay on subsidies collection. Shortfall on China's renewable energy development fund continues to widen, companies with outstanding subsidy receivable begin to seek different financing channels (for example: ABS, ABN issuance to speed up the cash inflow of renewable projects). Coal prices continue to rise, putting cost pressure on the thermal power plants. Companies actively request local governments to allow electricity price hike to partially compensate the higher cost of thermal power generation.

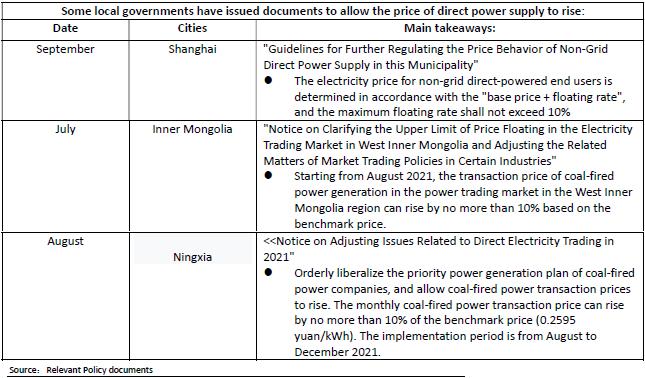

Rise on Coal Prices Negatively affects Thermal Power Profitability in the Near-Term, Industry Participants request for Price Increases to improve Operations.

Coal prices rise sharply in recent months, many thermal power companies operate at a loss. Some local governments allow upward adjustment on electricity pricing for direct supply contract by not more than 5%/10%/15% respectively. A pricing adjustment require permission from the local government, and in some provinces may not allow to increase price because of the added cost pressure to the local area. Power companies including Datang International, Beijing Guodian Power, Jingneng Power, Huaneng Group and other 11 coal-burning companies have jointly issue statement, < "Request for re-signing the long-term agreement for the October-December 2021 annual long-term agreement for direct electricity trading in the Beijing area" to reduce the loss incurred by the sharp increase in coal prices. We view thermal coal segment profitability to recover in next year as around 50% of the total electricity generated is sold through a direct-supply contract, and we assume the similar mix of direct supply contract for coal-fired electricity, which the contract price for electricity for 2022 will be renegotiated according to the coal price by the year end of 2021.

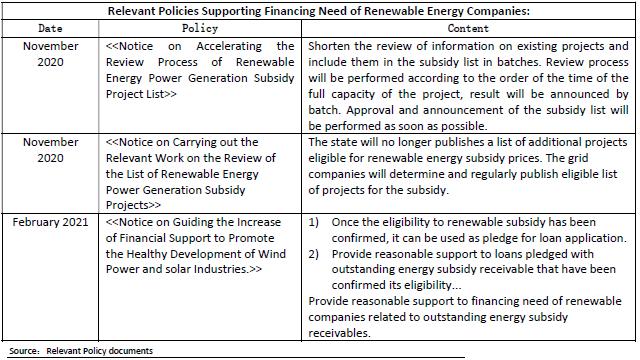

Policy Statement encourage to provide Financing on Confirmed Right of Renewable Subsidy Receivables.

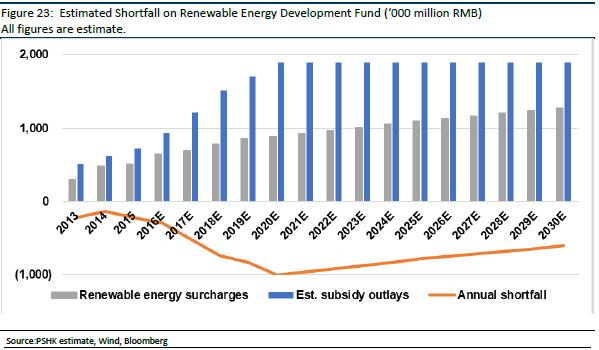

Due to the large amount of funding shortfall on the China renewable development fund, we estimate to reach an accumulated shortfall of about 315.8 billion yuan as of the end of 2019. As the funding shortage continues to widen in 2020, payback period is expected to further extend. Government is addressing the cash flow burden on subsidy funding delay, for example: policy statement released at the end of 2020, <>. The review process on outstanding subsidy receivable is expected to shorten, thus companies would be able to use that legal entitlement to subsidy as a pledge to access financing. Recent government policy issued on February 2021 encourage renewable energy companies to use various financing methods, such as securitization of renewable energy receivable, etc., which would speed up the cash flow conversion and reinvestment for the industry.

Renewable Energy Development Fund Shortfall expects to remain with the Amount of Shortfall shrinking year by year as New Projects not eligible for Subsidy.

With the current 1.9 cents/kWh renewable energy tariff surcharge, we estimate the national energy subsidy shortfall will continue to exist. We view government will avoid increasing the renewables energy surcharge, as it will cause unnecessary burden on society. As it will no longer provide subsidy on new onshore wind and solar projects, the expense outlay on the fund shall remain stable and declining as projects mature. Existing project subsidy will at maximum last for 20 years, we view the current shortfall still remain healthy. Policy statements include <> and <> 1). Encourage financial institutions to provide loan support to renewables companies, 2). Shorten the review process of renewable projects subsidy entitlement, to relieve pressure on cash flow caused by the delay in subsidies. Many power companies begin to issue subsidy receivable ABS to improve its cash flow problems. Visibility to funding is improved for the renewable companies with outstanding subsidy receivables.

Company business analysis:

CRP plans to build 40GW Renewable Capacity during the 14th Five-Year Plan Period.

CPR management plans to add 40GW additional renewable capacity during period between 2021 and 2025. The proportion mix of renewable energy capacity expect to exceed thermal power. CAPEX spending will remain at an elevated level of 30-35 billion HKD per year, management view that 1) business organic cash flow growth, 2) loan financing and 3) securitization of outstanding renewable subsidy shall be sufficient to fund the required capital expenditure, as CRP liabilities remains below its peers. As of the end of the first half of 2021, CRP has approved or registered about 0.6GW MW of wind power and 22.3GW of photovoltaic projects, a total of about 22.9GW. The current project backlog provides adequate visibility to the future 40GW new construction target by 2025.

Issuing ABS for Outstanding Subsidy Receivable could speed up Cash Inflows and support Future Capital Expenditures.

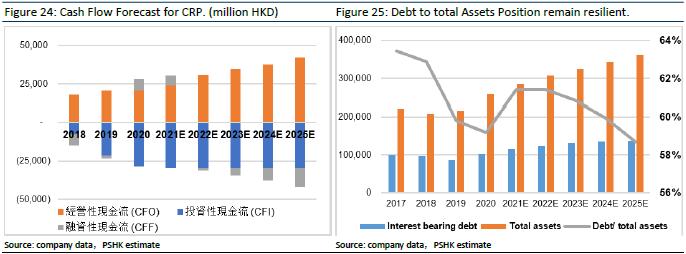

Total debt-to-asset ratio will expect to increase in the period between 2021 and 2022 but it expects to remain in an acceptable range. As more renewable projects contribute to additional revenue, it will reduce cash flow pressure on CAPEX spending. Debt to asset ratio will increase year by year and is expected to reach the peak and start falling by 2023. Free cash flow is expected to turn positive in 2023. Renewable energy will become the core earnings contributor by 2023-2025.

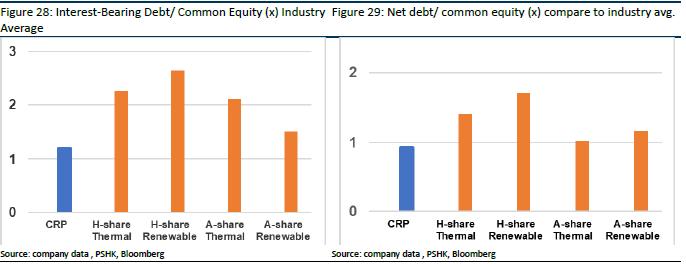

Debt Ratio is currently below Industry Average, Sufficient Buffer for further CAPEX Investment.

CRP expects to increase investment on renewable energy projects during the 14th fifth period, it will slightly increase its debt ratio. CRP's debt ratio will still be lower than the industry average. Therefore, the impact of increasing debt ratio shall be minimal. Pressure on equity financing is small. But we believe that 40GW of renewable investment (about 30-35 billion annual investment) present a potential opportunity for CRP to seek A-share listing. Meaningful transformation to renewable energy would act as a trigger for P/E multiple rerating on CRP.

CRP Thermal Power Assets are of High Utiliziation Hours and can provide Cash Flow to invest in Renewable energy.

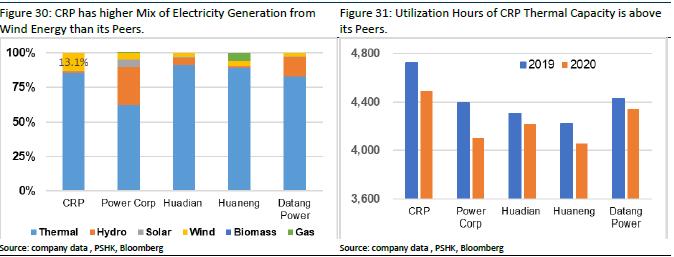

Investors are concerned thermal power to have reduced level of utilization, because many investments are pouring into renewable projects during the 14th fifth period that might adversely affect utilization rate for coal power. We view this concern is unnecessary as the additional renewable power production is unable to meet the incremental demand on power consumption. According to the industry forecast that the electricity consumption in China will be grow at 4.17% CAGR, increase on wind and solar power generation is expected to only meet about 2/3 of the increase in electricity consumption. Although the proportion of renewable electricity as of total electricity generation will continue to rise over time, it should have minimal impact on the existing stock of coal power capacity as renewables will be responsible for the incremental consumption demand. In the first half of 2021, the company's thermal power utilization hours still recorded an increase of approximately 10.5% year-on-year to 2,254 hours. CRP's average coal-fired capacity utilization hours is higher than major peers, it shows that the company's thermal power assets are in areas with strong power demand. Its thermal power operations utilization expects to remain stable or slightly increasing, that would provide cash flow for renewable projects investment.

Recent Sharp Rise on Coal Prices impact Profitability for Thermal Power, which may be Good Buying Opportunities.

Sharp rise in coal prices in the second half of 2021 put strong cost pressure on thermal power operations. Thermal power segment may incur losses in the second half of the year. For this time, CRP profitability expect to be different than the last cycle of coal price increase during 2016-2017. CRP have increased CAPEX spending on renewables will contribute to earning growth to meaningfully offset imapct on lower profitability from coal power. If the rise in coal prices from September to December has a negative impact on the company's stock price, it will be a good time to enter the market. Mainly because 1). About 50% of CRP's electricity generated is sold through a direct supply contract, if we assume 50% of the thermal electricity is sold through a direct supply contract, about 50% of the thermal electricity pricing will be reset by year end of 2021 to reflect higher coal price. Therefore, profitability of thermal power is expected to start to improve in 2022. 2). CRP is in the progress of transforming into renewable companies, which the reliance and influence of coal power will decline over time. We veiw the impact of coal prices to be only a short-term negative factor. It shall not affect the company's long-term investment recommendation.

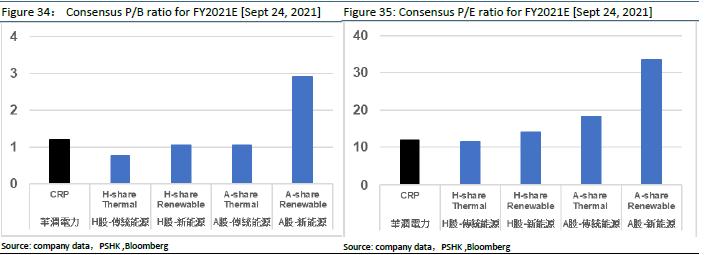

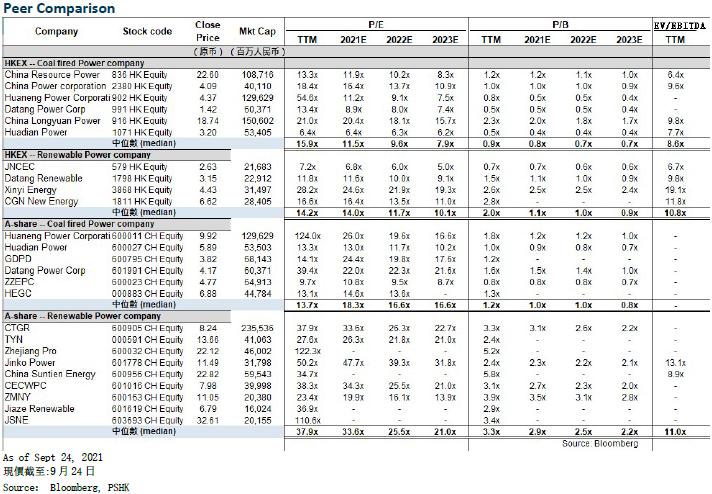

Valuation for renewable companies are higher, we view the renewable transformation during 14th fifth period as an opportunity for P/E rerating.

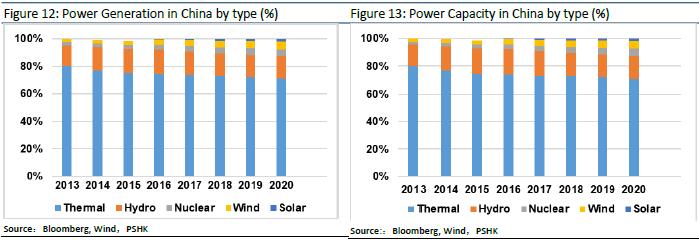

We view CRP will be a different beast coming into 14th fifth period as it 1) has A-share listing potential prospect, 2) transform into renewable energy giant with estimated renewable energy contribution of over 75% profit by 2025. As of 2020, the company's wind power generation accounted for 13.1%, which is a relatively high for a coal power dominant company. A-share listed renewable energy companies have an average forward 2021E P/E of about 33.6 times, and A-share traditional coal power companies also have a P/E valuation of about 18.3 times. We view that a valuation revision would happen as the market is pricing in the possibility of CRP A-share listing. We view investor of CRP would expect return from both 1). Organic growth on earnings coming from CAPEX investment during 14th fifth period and 2). Potential revision on multiple as CRP gradually transform itself into a renewable play in the electrictiy space.

Collection Delay on Renewable Subsidies is manageable for CRP.

The market is concerned with the shortfall on renewable energy development fund will affect cash flow position of CRP. We view the concern is unnecessary, as CRP is acceelerating the cash inflow on outstanding subsidy A/R through ABS issuance. In the first half of 2021, CRP issued about 2 billion of subsidy receivable securitization ABS at a financing cost of approximately 3.25% per annum, which is lower than the financing cost of CRP. CRP expects to issue another batch of ABS again in the second half of the year to speed up cash flow collection.

Earning Forecast:

2021 earnings expect to slightly decline yoy, mainly due to the strong rise in coal prices in the second half of the year, which will affect the profitability of the thermal power segment. About 50% of CRP's electricity generated is sold through a direct supply contract, if we assume 50% of the thermal electricity is sold through a direct supply contract, about 50% of the thermal electricity pricing will be adjusted by year end of 2021 to reflect higher coal price. Thermal power profitability is expected to recover in 2022. Renewable energy profit scale is expected to be approximately 4.7 times in 2025 compare to 2020, mainly due to the contribution of the company's 40GW new project planning.

Valuation Summary:

The recent outperformance compare Hang Seng index is justified, and we view there shall be further upside ahead from 1). Expanding investment in renewable projects, speeding up profit growth, and 2) closing the valuation gap with renewable companies once the renewable transformation gather wider recognition on the market. We issue CRP a target price of $33.4 HKD ($160.8 billion market capitalization).

- Implied valuation of renewable segment is derived with earning forecast for 2022 to reach 14.42 billion HKD. The average 2022 forward P/E ratio of HK-listed renewable companies is 11.7 times. From that, we issues a valuation at $168.7 billion for renewable segment.

- Implied valuation of thermal power segment is derived from the segment earning forecast of 4.76 billion HKD in 2022, and the average 2022 forward P/E ratio of coal power giants traded at 9.6 times. The coal power segment is valued at $45.7 billion.

- Assume the long-term tax rate is 25% to arrive at the SOTP valuation.

Risk factors

1) The illness is not controlled as expected

2) Coal prices continue to rise sharply.

3) The scale of new energy installed capacity is less than expected.

4) The price of photovoltaic/wind power equipment has risen more than expected.

5) The subsidy collection rate is slower than expected.

Financial Forecast:

Click Here for PDF format...