Investment Summary

Xiaomi (1810.HK) is an internet company with smartphones and smart hardware connected by an IoT platform at its core. After ten years of development, the company's annual revenue has exceed RMB 240 billion, and its products were sold in more than 100 countries and regions around the world. In the second quarter of 2021, according to Canalys, the company became the world's second largest smartphone manufacturer for the first time. Besides, the company has also created many smart hardware products, many of which have the largest sales volume and built the world's largest consumer IoT platform. As of June 2021, MIUI's monthly active users have reached 454 million and it provides them with a series of innovative internet services.

Continuous increasing overseas market share, Entering the high-end market

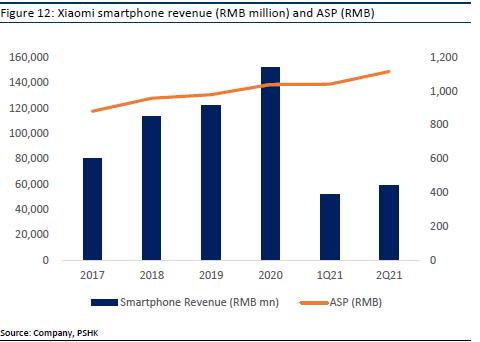

Xiaomi began its global expansion in 2014 and has accelerated its pace since 2016. In the fourth quarter of 2020, the company's smartphone shipments in 54 countries and regions around the world ranked in the top five. In the second quarter of 2021, accounting to Canalys data, Xiaomi's shipments in Latin America, Africa and Western Europe increased by 300%, 150% and 50% respectively. It is favorable for Xiaomi to hit the high-end market in the long-term and compete for more market share in the high-end market. Benefiting from the continuous increase in sales of mid-to-high-end products, the company's smartphone ASP has steadily increased. In 2020, the ASP will be approximately RMB 1,040 (+6.1% yoy). In the first half of 2021, the company's global shipments of smartphones with RMB 3,000 or above in mainland China and priced at 300 euros and above overseas exceed 12 million units, surpassing approximately 10 million units in 2020.

“Mobile phone + AIoT” core strategy

Xiaomi established “mobile phone + AIoT” as its core strategy. In the field of AI (artificial intelligence) + IoT, Xiaomi proposed “1+4+X”. Through a Xiaomi smart phone, connect its four important self-developed platforms: smart TVs, laptops, smart speakers, routers, and other smart products empowered by Xiaomi's ecological chain, that is, to create an ecological model of intelligent interconnection of all things. In terms of IoT business, the company's revenue in the second quarter was RMB 20.7 billion (+35.9% yoy). As the Internet of Things business accelerates into overseas markets, we expect IoT to be the company's key business in the future, copying the sales logic of smartphones, and we expect the company's IoT business to maintain a 30% year-on-year growth in 2021.

MIUI users continues to increase, an important engine for company's profitability

The company provides users with a complete mobile internet experience by providing internet services. As of 2020, the company's own operating system MIUI based on the Android native system has approximately 454 million monthly active users. MIUI is fully compatible with Android ecosystem. The application that has developed include Mi App Store, Mi Browser, Mi Music and Mi Video apps etc. Compared to other internet platforms that acquire new users at high costs, the company leverage the sale of hardware to acquire users at a profit.

Company valuation

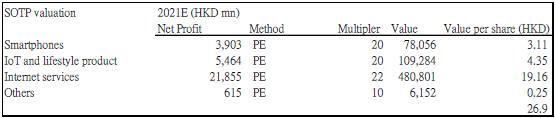

The three main business of Xiaomi Group are smartphones, IoT and consumer products, and Internet services. We use the segment valuation method (SOTP) to evaluate the company's three businesses separately and give the company's smartphone/ IoT/ internet services 20x/ 20x/ 22x of 2021 price-to-earnings ratio (P/E). The target price is HKD 26.90, which corresponds to the company's overall P/E ratio of 21x/ 19x/ 17x in 2021/ 2022/ 2023. The company is given a “Buy” rating (first coverage).

Company Profile

Xiaomi (1810.HK) is an internet company with smartphones and smart hardware connected by an IoT platform at its core. The company was established in 2010 and was listed on the main board of the HKEX in July 2018. After ten years of development, the company's annual revenue has exceed RMB 240 billion, and its products were sold in more than 100 countries and regions around the world. According to Canalys, in the forth quarter of 2020, the company's smartphone shipments in 54 countries and regions ranked the top five, especially in India's huge smartphone market, the company maintained its ranking for 13 consecutive quarters. The company has advocated a bold and innovative culture, from the “triathlon” business model, to one-of-a-kind ecosystem of companies; and from a unique engagement model with online users, to a highly efficient new retail strategy incorporating both online and offline. In the second quarter of 2021, according to Canalys, the company became the world's second largest smartphone manufacturer for the first time. Besides, the company has also created many smart hardware products, many of which have the largest sales volume and built the world's largest consumer IoT platform. As of June 2021, MIUI's monthly active users have reached 454 million and it provides them with a series of innovative internet services.

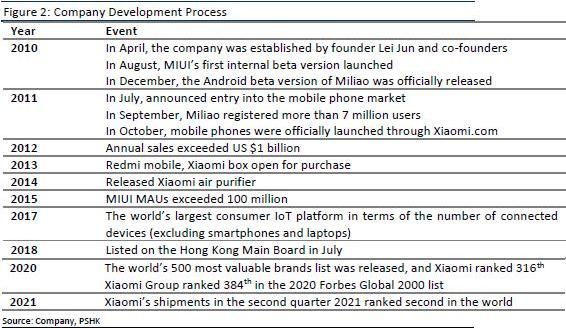

Company Development Process

Operating Condition

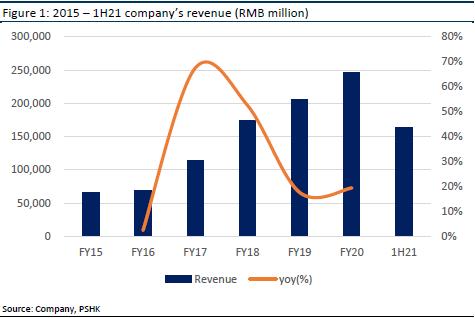

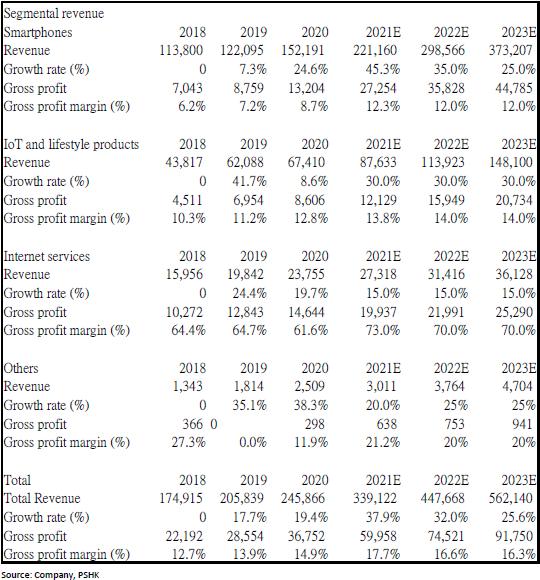

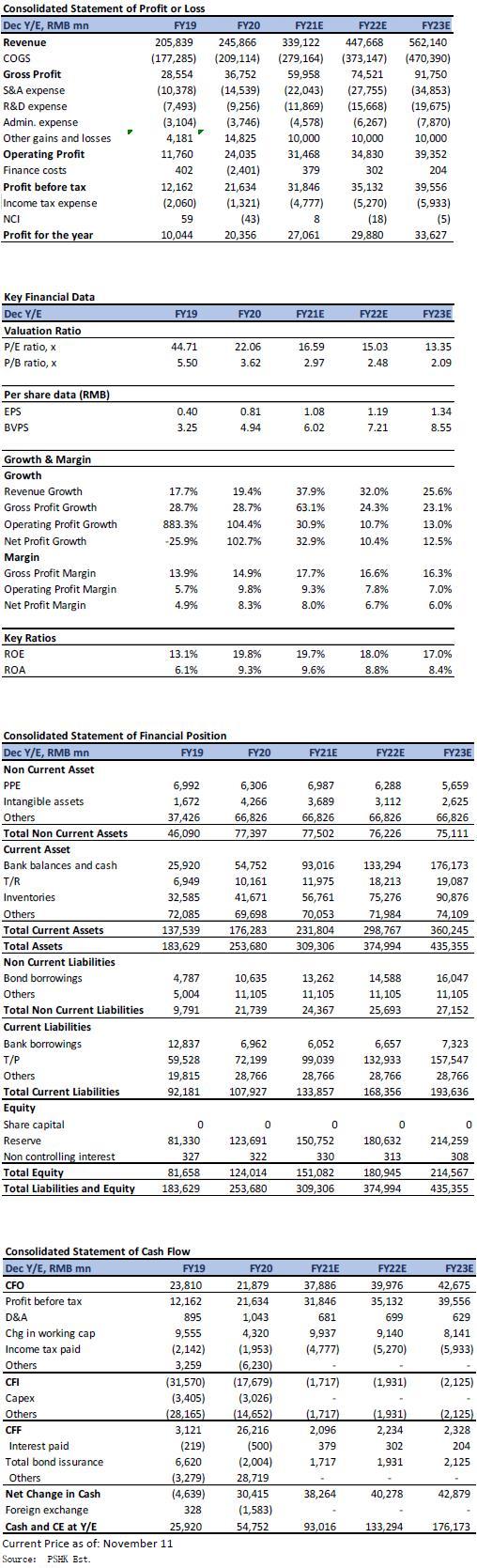

In 2020, the company achieved revenue of RMB 245.9 billion (+19.4% yoy) and gross profit reached approximately RMB 36.8 billion (+28.7% yoy) with the gross profit margin of 14.9% (+1.0 ppts yoy). The company's net profit reached RMB 20.3 billion (+103% yoy) and the net profit margin was 8% (+ 3.4ppts yoy).

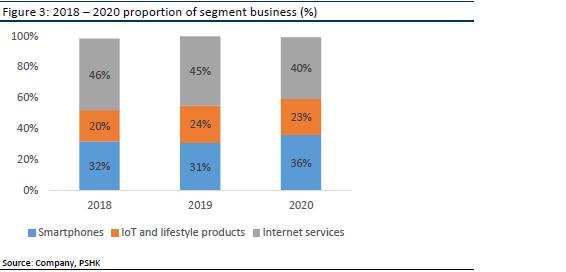

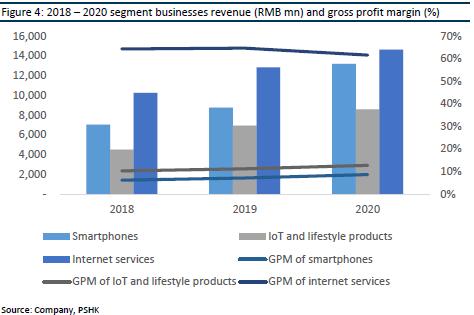

The company's business mainly includes smart phones, IoT and lifestyle products and Internet services. Among them, smart phones have been the company's largest source of income. In 2020, smartphone revenue reach RMB 152.2 billion (+24.6% yoy) and its revenue accounts for approximately 62% of total revenue. The global smartphone shipments for the year were 146.4 million units (+17.5% yoy). Gross profit was RMB 13.2 billion (+50.7% yoy) and fross profit margin was 8.7% (+1.5 ppts yoy), reflecting the improvement and optimization of the company's overall product portfolio.

The revenue of IoT and lifestyle products in 2020 reached RMB 67.4 billion (+8.6% yoy) and its revenue accounted for 27.4% of total revenue. Among them, it includes smart TVs, laptops, air purifiers, sweeping robots, smart cameras, smart speakers, routes, etc. Gross profit was RMB 8.6 billion (+23.8% yoy), and gross profit margin was 12.8% (+0.9 ppts yoy).

In terms of internet service business, the full-year revenue in 2020 reached RMB 23.8 billion (+19.7% yoy) and its revenue accounted for 9.7% of total revenue. Among them, the company's advertising business revenue was RMB 12.7 billion (+19.2% yoy). Based on focusing on improving user experience, the company continuously optimizes the accuracy of algorithms and content recommendations. The game business revenue was RMB 4.2 billion (+31.4%). The overall gross profit of the segment business was RMB 14.6 billion, (+14% yoy) and the gross profit argin was 61.6% (-3.1% ppts). The gorss profit margin of the internet service segment in the fourth quarter of 2020 was 68.4%, mainly due to the increase om the company's advertising and financial technology business gross profit margin.

From the perspective of the company's revenue structure and growth logic, the company's three major businesses have maintained rapid growth, but the gross profit margin of mobile phones and hardware has remained low due to Xiaomi's strategy. At the same time, although the company's internet service revenue only accounts for about 9.7% of the company's total revenue, its gross profit accounts for more than 40% of the total gross profit. In the long run, the company uses the sales of smart phones and hardware to divert traffic, and while maintaining high customer stickiness, it adopts internet services to realize the strategy of monetization.

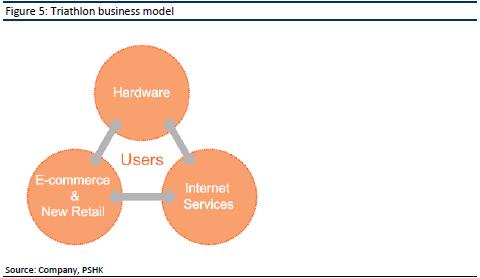

“Triathlon” business model

The “Triathlon” business model comprises three synergistic pillars of growth, 1). Innovative, high quality and well-designed hardware focused on exceptional user experience, 2). Highly efficient new retail allowing for the products to be priced accessibly, 3). Engaging internet services. As an internet company, the company initially used brand-new retail channels to sell various smart hardware products driven by its own operating system, MIUI to users so as to establish a huge own platform and provide users with a variety of internet services. The business is closely linked to each other and establish a group of very dedicated and highly loyal users, called “Mifen”.

Net profit margin of hardware business will not exceed 5%

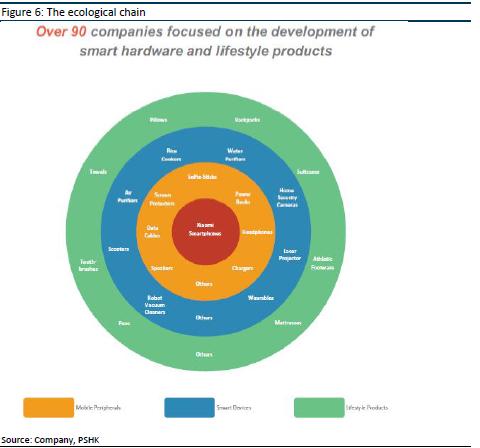

The company provides a series of hardware products jointly developed with the ecological chain enterprises and is committed to positioning the products at a price acceptable to the majority of users to ensure a wide range of acceptance and a high level of retention. Therefore, the company has promised since 2018 that the company's hardware comprehensive after-tax net profit margin will never exceed 5%. If it exceeds, the company will return more the excess above 5% to the users. The promise has been fulfilled and in 2020, the net profit margin of hardware is still less than 1%. In terms of core products, the company focuses on the design and development of a series of advanced hardware products, including smart phones, laptops, smart TVs, artificial intelligence speakers and smart routers. As of March 2018, the company has established an ecological chain of more than 210 companies through investment and management, of which more than 90 companies focus on the research and development o smart hardware and consumer products.

E-commerce and new retail, combined with online and offline sales channels

Having an efficient retail distribution platform is a core component of the company's growth strategy which enables the company to expand user coverage and enhance user experience. At the beginning of its establishment, the company has been focusing on online direct sales of products to achieve maximum efficiency and establish direct digital interaction with users. Mi Store and Youpin are the company's own direct sales e-commerce platforms. As of the first quarter of 2018, Mi Store has become the third largest 3C and home appliance online retail direct sales platform in Mainland China in terms of total product transactions. At the same time, the company also uses the localized sales and marketing expertise, logistics facilities and payment systems of third-party e-commerce platforms, such as JD.com, Tmall, Flipkart, TVS Electronics and Amazon to increase more online shopping channels.

Internet service ecology

The company provides users with a complete mobile internet experience by providing internet services. As of 2020, the company's own operating system MIUI based on the Android native system has approximately 454 million monthly active users. MIUI is fully compatible with Android ecosystem. All mobile applications on the Android ecosystem are included to form an open platform, which is beneficial for the company to provide a wide range of internet services, including content, entertainment, financial services and performance tools. As of 2018, the company has developed apps with more than 10 million active users in 38 months and apps with more than 50 million active users in 18 months, including Mi App Store, Mi Browser, Mi Music and Mi Video apps. Compared to other internet platforms that acquire new users at high costs, the company leverage the sale of hardware to acquire users at a profit.

Industry analysis

Global mobile phone shipments recover and enter the stock market

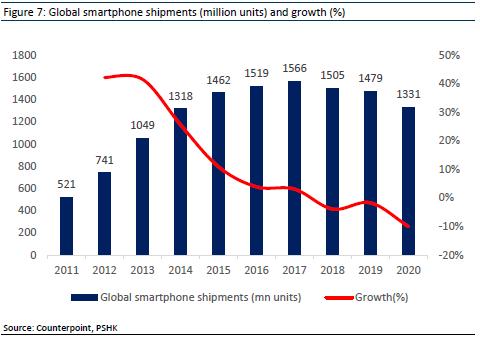

In 2020, due to the epidemic, Sino-US trade friction, and consumer demand for new equipment slowed down, the pattern of the smartphone market has changed. The poor performance of the smartphone terminal market, restricted sales channels and tight supply chain production have led to a decline in smartphone shipments. According to data released by the market research agency Counterpoint, global smartphone shipments will be 1.33 billion units in 2020 (- 10% yoy). Since 2021, the epidemic has eased, and global mobile phone shipments have begun to recover. According to data released by Canalys, global shipments reached approximately 350 million and 320 million units in the first and second quarters (+ 27% yoy and 11% yoy% respectively), but a 9% qoq drop in the second quarter, mainly due to chips shortage, such as the supply of key components is tight.

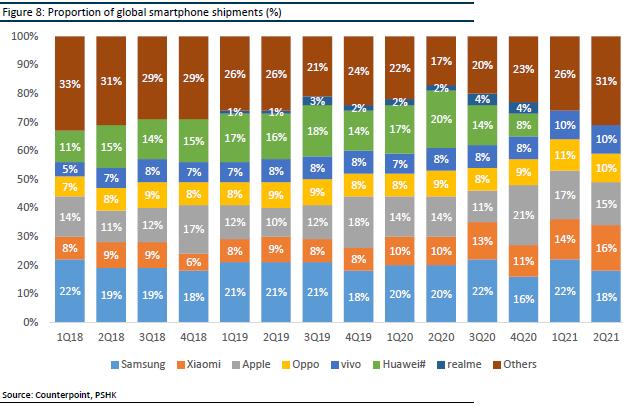

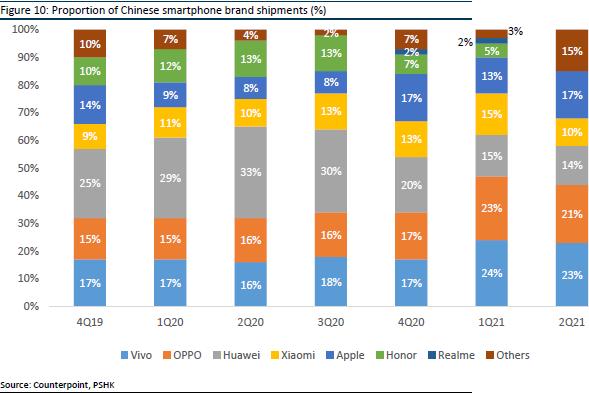

In recent years, with the rise of Chinese mobile phone manufacturers, the top competition in the smartphone market in China and overseas has become increasingly fierce. The main leading companies are Samsung, Apple, Xiaomi, OPPO, VIVO and Huawei. Since August 2020, after the United States announced chip sanctions against Huawei's mobile phone shipments have been significantly affected. With shipments including the divestiture of Huawei's Honor mobile phone brand, Huawei's overall shipments in the fourth quarter of 2020 and the first quarter of 2021 were 33 and 15 million units, down about 35% and 55% from the previous quarter. The global market share has dropped from 20% in the second quarter of 2020 at its peak which has dropped to 8% in the fourth quarter of 2020. At the same time, Xiaomi's smartphone business is expanding steadily. According to Counterpoint's data, Xiaomi ranked third in global mobile phone shipments in the fourth quarter of 2020, with a market share of 11%. In the second quarter of 2021, Xiaomi succeeded surpassing Apple and became the second largest shipment company in global mobile phone, with a market share of 16%, which is about two percentage points behind the share of the first Samsung company. Lei Jun, Xiaomi's board of directors held a 2021 speech and Xiaomi's autumn new product launch conference on August 2021 and pointed out that Xiaomi's goal is be the world's first place within three years.

Chinese smartphone market

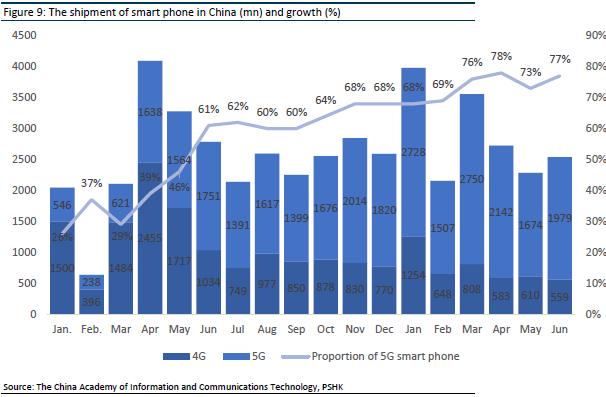

In the first half of 2021, the overall shipment volume of China's mobile phone market maintained rapid growth. According to the authoritative release of the China Academy of Information and Communications Technology, its shipment volume in the first half of the year was 174 million units (+13.7% yoy) of which 128 million 5G mobile phones (+101% yoy), accounting for approximately 74% of overall mobile phone shipments. In the second quarter of 2021, due to the early release of domestic mobile phone market demand (the first quarter shipments increased by 100% yoy), the shortage of mobile chips, the absence of Huawei and other factors, the second quarter caused a decline in April, May and June yoy. However, the decline has narrowed from more than 30% in April and May to 10% in June, and achieved an increase of 11.7% mom. In addition, accounting to Counterpoint's data, Huawei used to be the first in China's mobile phone market share, accounting for about 33% in the second quarter of 2020. Since Huawei was sanctioned by the US chip, Huawei's market share has begun to decline, and its market share has begun to decline, and its market share in the second quarter of 2021 is only 14%. VIVO and OPPO have become the major manufacturers and further seize shares in the Chinese market. Xiaomi's market share in China is relatively stable.

Global business expansion

Xiaomi began its global expansion in 2014 and has accelerated its pace since 2016. As of December 31, 2020, the company's products are sold in more than 100 markets around the world. According to Canalys` statistics, in the fourth quarter of 2020, the company's smartphone shipments in 54 countries and regions around the world ranked in the top five. In 2020, Xiaomi's overseas market revenue reached approximately RMB 122.4 billion (+34.1% yoy), accounting for 49.8% of total revenue (+5.5 ppts yoy) and an increase of 21.6 ppts from the proportion of overseas revenue in 2017. At present, the overseas market of Xiaomi mobile phones mainly depends on the three major global markets, namely the European market, European market, the Indian market and other emerging markets. In the second quarter of 2021, accounting to Canalys data, Xiaomi's shipments in Latin America, Africa and Western Europe increased by 300%, 150% and 50% respectively. Xiaomi has achieved significant business in-depth expansion in the global business landscape. In addition to relying on cost-effective products, formulating different strategies for different countries and region is also one of the keys Xiaomi's successes in overseas markets.

Indian smartphone market

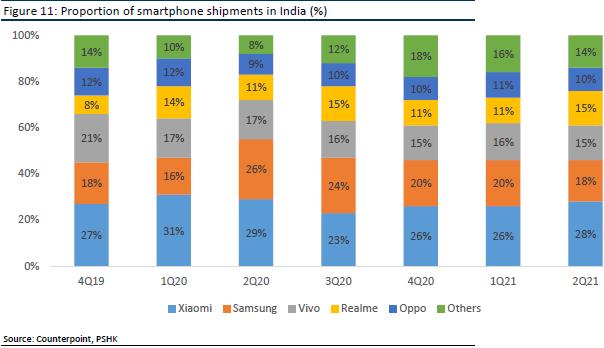

The Indian smart phone market is the second largest consumer market with the fastest growth rate in the world and having an average of more than 30,000 people joint to use smart phones every day. According to IDC data, the Indian smartphone market will shrink by 2% in 2020, with total sales reaching approximately 150 million units. According to Counterpoint data, Xiaomi ranked first in Indian sales in 2020 and accounted for approximately 28% of the market share in the second quarter of 2021. In addition, Samsung has the second largest market share in the Indian market, and its shipment volume in the third quarter of 2020 was slightly higher than that of Xiaomi, which had a market share of 24%.

The Indian market is the first place where Xiaomi has lived internationally. In 2014, Xiaomi officially entered the Indian market and began to sell mobile phones that support 4G network service Mi3, providing better mobile phone functions, while rivals such as Samsung and Micromax are still selling 3G mobile phones. At that time, Xiaomi insisted on its online sales strategy and cooperated with the local e-commerce company Flipkart to replicate the flash purchase strategy used in China to India to accelerate the penetration rate of Mi3 in the Indian market. However, in 2015, the Indian government doubled the import tariffs on smartphones in order to implement the made in India plan. For Xiaomi, this is both a challenge and a turning point for success. Xiaomi cooperated with Foxconn to quickly deploy its supply chain to India, build mobile phone factories, R&D centers, etc. and print labels made in India to avoid the impact of the Indian government's tariff policy which is five years ahead of Apple. In 2016, Xiaomi's market share in India increased from 3.3% in 2015 to 13.3% (+10 ppts yoy) and established Xiaomi's position in the Indian market. In addition to deploying its supply chain in India, Xiaomi also deployed its own retail stores. Previously, the Indian government stipulated that 30% of the purchase of goods must originate from India when opening a physical store in the local area. In 2017, Xiaomi chose to accept and adapt to local policies and open a Xiaomi store. As of 2020, Xiaomi already has 3000 brand stores in India, and Apple did not open its first physical store unit 2019.

European smartphone market

The European mobile phone market share used to be occupied by Samsung, Huawei and Apple for a long time, but then Huawei's position was gradually replaced by Xiaomi, and Xiaomi also began to challenge the number one position. Huawei entered the European market as early as 2012, and after 7 years of hard work, it won the second place in the European mobile phone market in the first quarter of 2019. At that time, Huawei's shipment growth rate has exceeded that of Samsung, which is the number one. However, in the beginning of the fourth quarter of 2019, Huawei and Google have encountered obstacles in cooperation and their mobile phones can no longer carry Google GMS services, which has greatly affected sales.

Xiaomi only began to deploy the European market in 2017. However, the style of the entire European mobile phone consumer market is not uniform, and Xiaomi also adopts different strategies based on market differences in Western Europe and Eastern Europe. According to statistics from GFK 2018, the average unit price of smartphones in the Western European market (the price that mobile phone manufacturers sell to operators and distributors) is US$446.7, which is the most expensive market outside of North America, while Eastern Europe and Central Europe have the average unit price of USD 249. Xiaomi has adopted a cost-effective strategy in Eastern Europe. As the mobile phone market in Western Europe is more mature, its mobile phone sales channels are mainly operators, accounting for about 50%, while other offline sales channels account for about 40%, and only online about 10%, the main reason is the preferential price brought by the operator's high subsidy. Therefore, in 2018, Xiaomi and Cheung Kong Hutchison Holding Limited formed a global strategic alliance to sell smartphones in Europe through the “3 Group” and strengthened the layout with other European leading operators, for example, Xiaomi reached the mobile phone sales agreement with the “big four”, Orange, SFR, Bouygues and Free in France.

According to Canalys data, in the fourth quarter of 2020, Xiaomi ranked first in the Central and Eastern European market for the first time, with a market share of 24.7% (+17.5% yoy). The shipment of smartphones in Western Europe increased by 57.3% yoy with a market share of 10.9%, maintaining the top three. Among them, in the Spanish market, the company ranked first in smartphone shipments for the fourth consecutive quarter, with a market share of 27.0%. In addition, in the fourth quarter of 2020, the company's smartphone shipments in France, Italy and Germany achieved a year-on-year growth of 86.2%, 61.6% and 139.8% respectively. Xiaomi has maintained strong growth in the European market. According to Strategy Analytics, in the second quarter of 2021, Xiaomi reached the top of the European smartphone market for the first time, surpassing Samsung and Apple in market share, and shipped approximately 12.7 million units (+67.1% yoy) and the market share reached 25.3%.

“Smratphone x AIoT” strategy

Since 2017, after more than 4 years of planning and verification, in August 2020, the company established the core strategy for the next ten years, “Smartphone x AIoT”. The company clearly affirmed the core position of the smart phone business, and built a smart life around the core business of the mobile phone through the AIoT business, and became an amplifier of Xiaomi's value. Finally, with the further integration of intelligent interconnection, the company emphasizes the multiplication effect and aims to penetrate more scenarios to win more users and become the moat of Xiaomi's business model. As of December 2020, the number of Xiaomi AIoT connected devices (excluding smartphones and laptops) reached 234.8 million (+38% yoy). The number of users with five or more devices connected to the Xiaomi AIoT platform (excluding smartphones and laptops) reached 6.2 million (+52.9% yoy). The number of monthly active users of the artificial intelligence assistant (“小愛同學”) increased by 43.5% year-on-year to 86.7 million. In order to enhance the synergy between Xiaomi mobile phones and IoT products, the company released the “Point to Connect” Ultra Wide Band (UWB) technology in October 2020, which can be controlled by pointing the mobile phone at the device. In November, the company released a technology which automatically recognized nearby IoT devices through mobile phones and automatically configures the network. At the same time, it also released the IoT software platform Xiaomi Vela based on the open-source embedded operating system NuttX to create fragmented IoT applications. In addition, the company released MIUI 12.5 system in December to launch MIUI+ Services, realizing seamless collaboration between mobile phones and laptops. In the future, it is expected that the company will continue to improve the interconnection capabilities between smartphones and IoT products, strengthen the “Smartphone x AIoT” strategy, and enhance the company's overall business competitive advantage.

Promoting a dual-brand strategy, Entering the high-end market

In order to grab the market share of each price layer, Xiaomi adopted a brand split strategy, mainly dividing the mobile phone business into 3 different sub-brands:

1). Positioning the mid-to-high-end Xiaomi, 2) Focusing on the low-end and cost-effective Redmi, 3). Locking in the gaming mobile phone segment Black Shark. Each of the sub-brands also launched a variety of series for the choice of Mifen.

In terms of high-end smartphone sales. In 2020, Xiaomi will sell approximately 10 million high-end smartphones priced at RMB3,000 in mainland China and 333 euros and above overseas. In December 2020, the company launched Xiaomi 11 in mainland China, the world's first Snapdragon 888 processor, priced at RMB 3,999, and sales exceeded 1 million units within 21 days of launch, reflecting the market's recognition of Xiaomi's products in the high-end market. It is favorable for Xiaomi to hit the high-end market in the long-term and compete for more market share in the high-end market. Benefiting from the continuous increase in sales of mid-to-high-end products, the company's smartphone ASP has steadily increased. In 2020, the ASP will be approximately RMB 1,040 (+6.1% yoy). In the first half of 2021, the company's global shipments of smartphones with RMB 3,000 or above in mainland China and priced at 300 euros and above overseas exceed 12 million units, surpassing approximately 10 million units in 2020.

Consumer IoT market

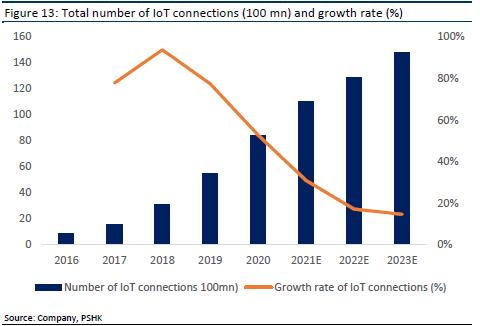

The Internet of Tings (IoT) is a network between devices that can communicate seamlessly through the internet. According to the “Mobile Economy 2021” report released by the Global System for Mobile Communications Association (GSMA), the total number of global IoT connections in 2020 will reach 13.1 billion (+9.2% yoy). It is estimated that by 2025, the total number of global IoT connections will be scaled up. It will reach 24 billion, with a compound growth rate of 12.9% in 2020-2025. The revenue of the global IoT in 2019 is 343 billion U.S. dollars, and it is expected that revenue will increase more than three times by 2025. According to the data of iResearch's “China Personal Internet of Things Industry Research White Paper 2021”, the number of IoT in China has grown rapidly. In 2019, the number of connection reached 5.5 billion (+75.6% yoy) and the compound growth rate from 2016 to 2019 was high as 82.4%, and it is expected to reach 14.8 billion in 2023, with a compound growth rate of 20.78% in 2020-2023.

The consumer-level IoT market refers to the sales of IoT devices and the provision of consumer-oriented IoT-driven services. Consumer-related IoT applications cover a wide range, including information and entertainment, healthcare, smart home, home security and safety, etc. As the target audience of the consumer IoT has a large customer base, a single user demand, and a large variety of products, it is easier to obtain a first-mover advantage when the supporting technology of sensors and device processors is improved. Suppliers provide users with a better experience by connecting various products under a single ecological chain. The introduction of 5G infrastructure, support for low-latency and high-data-density connections of devices, and continuous investment in software technology, cloud infrastructure and artificial intelligence will strengthen IoT services in applications, analysis, data sharing and storage functions, and will also conducive to the development of the number of peripheral IoT devices for consumers.

The business logic of personal consumption-level IoT

The development chain of personal consumption IoT is not just superficially relying on hardware sales to make profits. Instead, it obtains a full range of user data through smart devices. Therefore, in the long-term perspective of the industry's monetization logic, terminal product sales are only the first step to obtain data, and the real business logic lies in the value of its data. For example, 1) Manufacturers use data to charge customers for advertising push, cloud storage and internet value-added services, 2) the IoT cloud platform uses data for algorithm training and polishing technology, and empowers smart terminal manufacturers and developers with the technology, 3) mastering user data makes it easier to enrich personal IoT scenarios and explore ways of monetization.

Therefore, when some consumer-grade (IoT) manufacturers develop electronic products, in addition to considering factors such as quality and price, they have to also provide multiple types of integrated platforms that can be seamlessly interconnected through a single application, such as Xiaomi Mi Store, Huawei's Hilink, Apple's closed-loop ecosystem: iTunes ecosystem, iCloud ecosystem, IOS ecosystem, App Store ecosystem, etc. Manufacturers use their own hardware products to interconnect in their own ecosystems to create a platform ecosystem integrating hardware, software, and services to achieve a two-way and mutually beneficial layout. However, with current data security supervision and software services still being developed, tangible consumption and direct experience are more important for consumers. In the future, as consumer awareness and personal terminal connections increase, the business model of monetizing data and services will bring more benefits to users and enterprises.

Xiaomi IoT consumer market ecological chain

In 2019, Xiaomi established “mobile phone + AIoT” as its core strategy. In the field of AI (artificial intelligence) + IoT, Xiaomi proposed “1+4+X”. Through a Xiaomi smart phone, connect its four important self-developed platforms: smart TVs, laptops, smart speakers, routers, and other smart products empowered by Xiaomi's ecological chain, that is, to create an ecological model of intelligent interconnection of all things.

IoT and lifestyle products

Smart TV

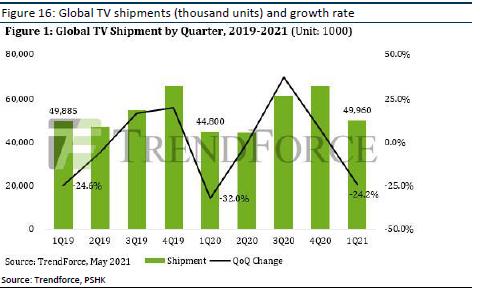

Due to the home economy driven by the epidemic, the global demand for TV will gradually increase in 2020. According to TrendForce's report, global TV shipments rebounded from the bottom of April 2020 to peak in October 2020. Since the fourth quarter, TV brands have delayed their shipments in the fourth quarter of 2020 due to the shortage of IC products from upstream semiconductor suppliers. In 2020, global TV shipments reached 217 million units (-0.3% yoy). Related supply chain shortages continued in the first quarter of 2021, leading to longer delivery times for TV sets.

In addition, according to TrendForce's report, in 2020, due to the decline in the production capacity of Korean panel makers and the slowdown in the growth of mass production of new panel makers in China, the supply of TV panels will decrease. Given the imbalance between supply and demand, the price of 40-inch and 55-inch TV panels has risen by more than 60% in six months, while the price of 32-inch panels has more than doubled. With the tightening of panel supply in the market, the shortage of IC product wafer production capacity, and the increasing choices of upstream supply chains such as foundries and panel manufacturers for customers, leading first-line TV brands are ensuring the wafer capacity of foundries due to their huge order volume. It has more advantages in other aspects.

As TV panel prices increase month by month in the second half of 2020, the profitability of mainstream 32-inch to 55-inch TVs in the market has also gradually declined. Therefore, TV brands have also begun to purchase larger-sized panels to cope with the declining profitability of low-priced products. In the second half of 2020, the shipments of 65-inch and 70-inch and above TV panels increased by 23.4% and 47.8% respectively.

According to data from industry research organization Omdia, in 2020, the total market share of the top five TV brands exceeded 60% for the first time. Among them, Samsung's sales revenue market share reached a record 31.9% (+1% yoy) and it has ranked first in global sales for 15 consecutive years. In 2020, Samsung sold about 7.79 million QLED TVs throughout the year (+46.43% yoy). At the same time, the high-end TV market and the large-screen TV market accounted for 45.4% and 50.8% respectively, far ahead of other brands, which LG and Sony's TV sales accounted for 16.5% and 9.1% respectively. According to data from AVC Revo, the top five are Samsung, LG, TCL, Hisense and Xiaomi in terms of global TV sales in 2020.

Xiaomi Smart TV

Xiaomi's smart TV was launched in September 2013 and defined it as “the first TV for young people”. In 2020, Xiaomi's global shipments of smart TVs reached 12 million units, a slight decrease of 6.25% yoy, mainly due to the epidemic and tight supply of major components. According to AVC Revo's statistics, as of the second quarter of 2021, Xiaomi TV's shipments in mainland China have been ranked first for the tenth consecutive quarter, and global smart TV shipments have ranked among the top five.

In addition, in terms of smart TVs, the company adheres to the strategy of promoting high-end, large-screen and international TVs. In terms of high-end, starting from July 2020, the company has launched the high-end flagship product Mi TV Master series, including the world's first mass-produced transparent TV, Mi Transparent TV, and Mi TV Master 82-inch commemorative edition, both priced at RMB 49,999. In terms of large-screen, after the launch of the Redmi Smart TV MAX 98”, Xiaomi released the Redmi MAX 86” ultra-large-screen TV in Feb 2021, with a starting price of RMB 7,999. According to statistics from AVC, in the fourth quarter of 2020, Xiaomi and Redmi brand TVs ranked first in the retail volume of large-screen TVs over 70 inches in mainland China, with a market share of 27.7%. In terms of internationalization, the company's smart TVs have entered India, Indonesia, Russia, etc., and will also begin to enter key markets such as France and Poland in 2020. It is expected that the penetration rate of the Xiaomi mobile phone brand in Europe and other places will gradually increase, which is beneficial to the sales of Xiaomi smart TVs in overseas markets. Among them, in the Indian market, according to data released by counterpoint, Xiaomi ranks first in the Indian TV market share with a market share of 27%, while LG and Samsung rank second and third respectively, with market shares of 14% and 10%.

Smart speaker

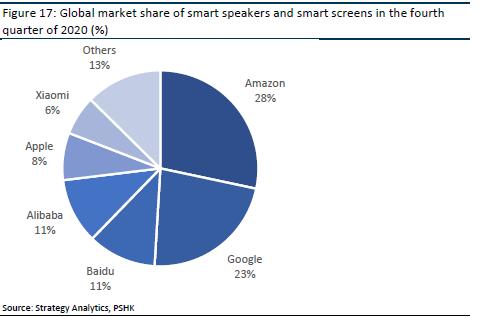

Smart speakers first emerged in 2014. Amazon's Echo speakers first combined voice interaction with speakers, enabling the speakers to implement functions such as calling, setting alarms, and querying the weather. Compared with Bluetooth speakers, smart speakers are better in terms of safety, transmission distance, and delay time. The main application scenarios of smart speakers are the living room, kitchen, bedroom, bathroom etc., and the main functions are voice interaction, content services, internet services, and smart home control. Smart speakers are currently in a stage of rapid development. According to Strategy Analytics, despite the severe market challenges caused by the Covid-19 epidemic, global smart speaker sales in 2020 have reached a record level. In the fourth quarter of 2020, smart screens accounted for 26% of the total smart speaker market, an increase of 4% yoy, mainly due to the increasing availability of models of different sizes and prices, which promoted the strong growth of smart screens and at the same time led to smart speaker's demand. At present, the smart speaker industry is relatively concentrated. The top six companies account for 87% of the total market share. Among them, Amazon has always occupied the largest market share in the smart speaker industry by virtue of its first entry advantage. In the fourth quarter of 2020, its smart speakers and smart screens accounted for 28%. In the future, smart speakers are expected to introduce more scenarios, and the industry prospects are good. According to iResearch consulting's data, it is estimated that the global smart speaker supply market will reach 2.78 billion in 2022, an increase of 135.6% over 2018.

Xiaomi Smart Speakers

Xiaomi smart speakers maintain its high cost-effective advantages among similar products. Users can connect to Xiaomi's voice-activated artificial intelligence speakers and other smart hardware products via Wi-Fi, and give personalized voice commands. Xiaomi's smart speakers are mainly divided into two models: Xiaomi AI speaker and Xiaomi AI speaker mini (小愛音箱). The Xiaomi smart speaker is equipped with voice-activated smart AI, which can respond to the user's Chinese commands, and adopts a high-quality audio system with a ring microphone to detect voice commands in all directions.

Smart Wearable Equipment

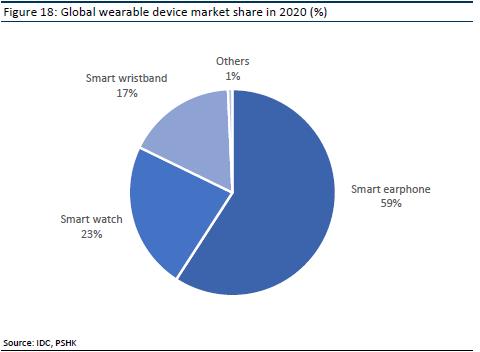

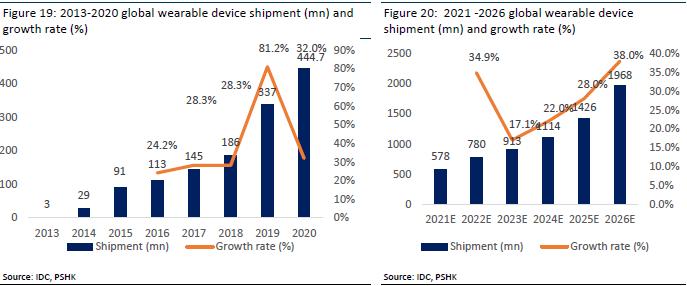

Smart wearable devices are smart devices that integrate various types of identification, sensing technologies, cloud services and other interaction and storage technologies to achieve user interaction, life entertainment, human body monitoring and other functions. Currently, they mainly include smart headphones, smart bracelets, smart watches, smart glasses, etc. In recent years, the artificial intelligence industry has become a number of national key development projects, with broad industrial prospects. According to data released IDC, from 2013 to 2020, global wearable device shipments have shown a clear upward trend, but the initial growth rate is relatively fast, and the growth rate has declined in recent years. In 2020, the shipment of wearable devices was 337 million. In 2020, the global wearable devices are mainly ear-worn devices, with a market share of approximately 59.14%, while the market shares of smart watches and smart bracelets will be 23.08% and 17.08%, respectively. Wearable devices continue to refurbish consumer technology products. Currently, the market generally expects that the market size of wearable devices will grow faster than mobile phones and tablets. According to IDC data, the global wearable device market is expected to be about US$578 million in 2021, and it is expected that the global wearable device market will reach approximately US$1.968 billion in 2026, with a 27.8% annual growth in the recurring cooperation from 21 to26.

Competitors in the wearable device industry are relatively concentrated. According to IDC data, in the fourth quarter of 2020, the world's top four manufacturers accounted for approximately 60% of global wearable device shipments. The volume reached 5.56 billion units (+27.2% yoy), accounting for approximately 36.2% of the global market share. Xiaomi ranked second, with shipments of 1.35 billion units in the fourth quarter of 2020 (+5.5% yoy), accounting for approximately 8.8% of the global market share. Samsung and Huawei ranked third and fourth, with 1.3 billion and 1.02 billion shipments in the fourth quarter of 2020 (+20.4% and 7.4% yoy, with market shares of 8.5% and 6.7% respectively).

Internet service

In 2020, under the influence of the epidemic, internet services have become one of the world's major economies that have achieved positive economic growth. The internet service market covers a wide range, including internet retail, online advertising, online games, internet finance, application stores and other internet services. The electronic devices, especially smart phones, are the main medium for users to connect to the internet. With the popularity of smart phones and greatly increasing the time users spend on the internet, the potential market for internet services has been expanded.

At the same time, due to fierce competition in the internet service market. The internet service market is highly competitive, and companies generally need to spend a lot of marketing expenses to establish and retain user groups. Therefore, companies that acquire and retain users through the sale of hardware equipment can reduce the cost of customer acquisition, increase the frequency of user participation, and increase the ability to collect data to strengthen the competitiveness of internet services.

By providing internet services, Xiaomi allows users to have a complete mobile internet experience. It has its own operating system MIUI based on the Android native system and is fully compatible with the Android ecosystem. It includes all mobile applications on the Android ecosystem, forming an open platform to provide a wide range of internet services, including content, entertainment, financial services, and performance tools. All Xiaomi smartphones are pre-installed with MIUI, and other Android smartphone users can also install MIUI for free. Xiaomi has maintained a high-speed growth of internet users worldwide. As of December 2020, global MIUI monthly active users reached 396.3 million (+28.0% yoy). Among them, the number of MIUI monthly active users in mainland China is 111 million. At the same time, the number of internet users of Xiaomi TV has also maintained growth. As of December 31, 2020, Xiaomi TV's paid users reached 4.3 million (+14.4% yoy).

In terms of monetization of internet services, the company is currently concentrated in mainland China currently, with its focus on internet advertising and value-added services. In terms of advertising, Xiaomi's advertising distribution channels mainly include Xiaomi App Store, Xiaomi Browser, Xiaomi Music and Xiaomi Video. The company provides advertisers with a variety of advertising forms such as display and effect to meet the business needs and marketing goals of customers. For display advertising services, companies generally charge advertisers based on the length of time the ads are displayed on the Xiaomi Internet platform; On the other hand, performance advertising services charge advertisers on a per-click basis when users click on advertising content, a per-display basis when advertising content is displayed to users, or a per-download basis when users download third-party applications.

In terms of Internet value-added services, most of the current revenue comes from online games. Most games on the Xiaomi platform are free. The company mainly obtains revenue through the sale of virtual currency recharged in the game, and the revenue is divided according to the revenue arrangement entered with third-party game developers. The income of other Internet value-added services also includes users paying to subscribe to premium entertainment content (such as online video, literature and music), live streaming and Internet financial services.

Financial Forecast

Xiaomi's total revenue in the first half of 2021 was RMB 164.7 billion (+59.5% yoy) and the gross profit was RMB 29.31 billion (+92.1% yoy) and the total profit was RMB 16.05 billion (+141.3% yoy). The total revenue in the second quarter reached a record high of RMB 87.8 billion in a single quarter, mainly due to the strong growth of mobile phone shipments. The company's smartphone revenue in the second quarter reached RMB 59.1 billion (+86.8% yoy). We expect that due to the weakening of global smartphone terminal sales in the second half of 2021 and the release of new mobile phones by other mobile phone manufacturers, the market for smartphone terminals will be fiercely competitive, and Xiaomi's overall mobile phone revenue growth in the second half of the year will slow down compared with the first half of the year.

In terms of IoT business, the company's revenue in the second quarter was RMB 20.7 billion (+35.9% yoy). As the Internet of Things business accelerates into overseas markets, we expect IoT to be the company's key business in the future, copying the sales logic of smartphones, and we expect the company's IoT business to maintain a 30% year-on-year growth in 2021. In terms of Internet services, the company's revenue in the second quarter reached RMB 7 billion, setting a record quarterly revenue, with revenue increasing by 19.1% year-on-year. The company's global Internet users continue to maintain rapid growth. As of June 2021, the number of MIUI monthly active users increased by 32.1% year-on-year to 453.8 million. At the same time, the company's advertising business and overseas Internet service revenue reached RMB 4.5 billion and RMB 1.1 billion, respectively, an increase of 46.2% and 96.8% year-on-year. We expect Internet services to maintain stable growth, but we still need to pay attention to the stickiness of the company's users. We conservatively estimate that Internet service revenue can maintain a 15% revenue growth and benefit from the high gross profit margin of the Internet service business which Can bring strong profit growth to the company.

Company valuation

The three main business of Xiaomi Group are smartphones, IoT and consumer products, and Internet services. We use the segment valuation method (SOTP) to evaluate the company's three businesses separately and give the company's smartphone/ IoT/ internet services 20x/ 20x/ 22x of 2021 price-to-earnings ratio (P/E). The target price is HKD 29.9, which corresponds to the company's overall P/E ratio of 21x/ 19x/ 17x in 2021/ 2022/ 2023. The company is given a “Buy” rating (first coverage).

Financial

Click Here for PDF format...