Investment Summary

Company Profile

Sanhua is the world's largest manufacturer of HVACR controls and components, focusing on heat management business with heat pump technology as the core. It operates the domestic and commercial air conditioning business as well as automotive heat management fields, establishing a leading position in the industry. The products of the Company such as electronic expansion valves of air conditioning, four-way reversing valves, solenoid valves, micro-channel heat exchangers, automotive electronic expansion valves, new energy vehicle heat management integrated components and omega pumps have the highest market share across the world. The market proportion of service valves, thermostatic expansion valves for vehicles and receivers rank top among the world.

Downstream Demand Continues Increasing, but the Raw Material Price Increases Lead to Slight Decline in Gross Margin

In recent years, the Company's downstream industry demand has been increasing, driving the Company's revenue to achieve continuous steady and rapid growth. According to the Company's 2021 Q3 report disclosed, in the first three quarters, Sanhua recorded a revenue of RMB11.72 billion, up 36.39% yoy; a net profit attributable to shareholders of the listed company of RMB1,293 million, up 18.4% yoy; a net profit attributable to the parent company excluding non-recurring items of RMB1,166 million, up 21.87% yoy. Among them, in the third quarter, it recorded a revenue of RMB4,046 million, up 23.53% yoy, a net profit attributable to shareholders of the listed company of RMB469 million, up 4.57% yoy; a net profit attributable to the parent company excluding non-recurring items of RMB447 million, up 19.12% yoy.

In terms of segment business, the revenue of refrigeration and air-conditioning electrical components business was RMB2.82 billion, up 7.6% yoy, with a net profit of RMB330 million, down 10.8% yoy; the new energy business maintained high prosperity, driving the Company's auto components business to record a revenue of RMB1.22 billion, up 88% yoy, with a net profit of RMB140 million, up 67.2% yoy.

In terms of profitability, the Company's gross margin was negatively impacted to some extent due to the continued price hike of bulk raw materials such as copper and aluminum in 2021 and the lag in price adjustment by downstream customers. The gross margin for the first three quarters was 27.16%, down 1.5 ppts yoy. Specially, the gross margin for the third quarter was 27.46%, down 2.68 ppts yoy and up 0.64 ppts qoq.

Under cost pressure, the Company's period expenses were well controlled, with a period expense ratio of 14.02% in the third quarter, down by 1.69 ppts yoy, of which the selling, management, R&D and finance expense ratios were 5.24%, 5.24%, 4.12% and -0.58%, respectively, a change of +1.16, -0.39, +0.27 and -2.72 ppts yoy; the net margin was 11.75%, -2.2 ppts yoy and +0.67 ppts qoq. The increase in R&D expenses was due to an increase in R&D staff salaries, the decrease in finance expenses was mainly due to an increase in interest income, and the increase in selling expenses was mainly due to an increase in shipping costs.

Negative Factors Are Gradually Dissipating and Profitability Is Expected to Recover from the Beginning of the Fourth Quarter

According to industry data, China produced 120 million residential air conditioners in the first three quarters of 2021, up 8% yoy, reflecting that industry demand has resumed positive yoy growth due to downstream inventory replenishment, and is expected to maintain growth in the fourth quarter. With the popular application of high-end home appliances and the rapid advancement of commercial refrigeration business (2025 revenue target of RMB4 billion, a CAGR of more than 30%), HVACR electrical component business is expected to achieve higher growth in the future.

In addition, the arrival of the peak season of automobile sales at the end of the year, coupled with the gradual improvement of the chip shortage, will promote the rapid growth of the Company's auto components business revenue in the fourth quarter, and the Company is expected to will record a revenue of RMB5 billion in the auto components segment in 2021. At the same time, among the Company's main customers, the expansion of the vehicle production capacity of Tesla, BYD and other enterprises will support the Company's future performance growth.

In terms of costs, the prices of bulk raw materials have fallen in the fourth quarter and the Company's profitability is expected to recover..

Investment Thesis

Sanhua is the leading company of refrigeration parts and components with obvious technical advantages in its products. The thermal management of new energy vehicles, dishwashers and cold-chain logistics are all promising business areas in line with the general direction of social development in the future. We expect that the Company's home appliance business will benefit from the market share increase year by year. There is a broad market for the thermal management of new energy vehicles in the future.

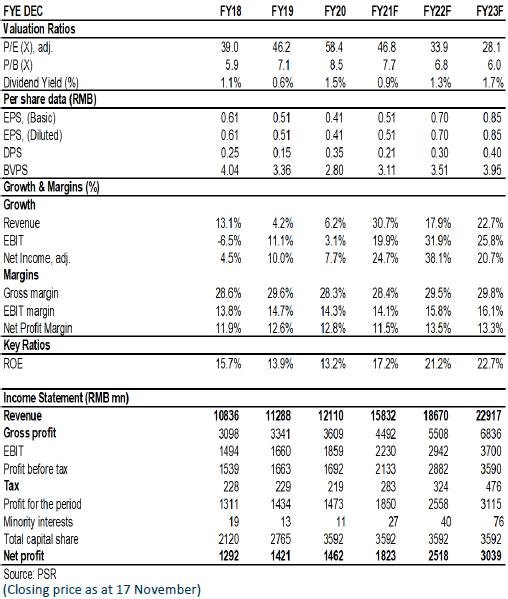

As for valuation, taking into account the negative impact of the increase in raw material prices and the increase in ocean freight, we adjusted the company's 2021/2022 earnings per share to 0.51/0.70 yuan (previously 0.58/0.70 yuan), and introduced a 2023 earnings per share forecast ( 0.85 yuan), a year-on-year increase of 25%/38%/21%,. And we accordingly gave the target price to RMB28.8, respectively 57/41/34x P/E for 2021/2022/2023. "BUY" rating. (Closing price as at 17 November)

Risk

Progress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices

Financials

Click Here for PDF format...