Investment Summary

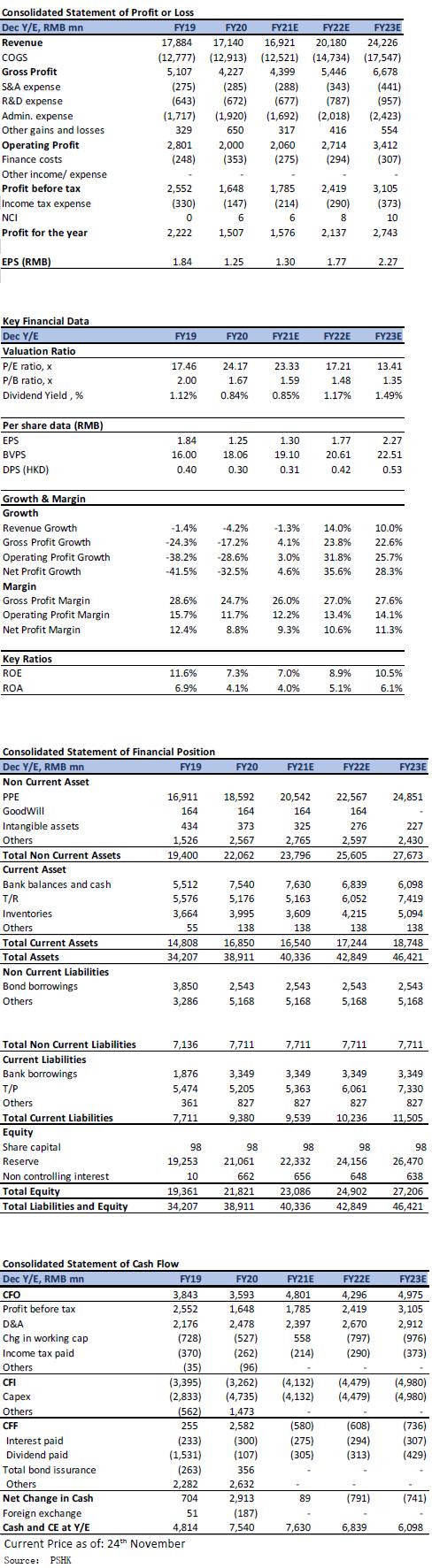

AAC Technology announced the company's interim results as of 30 September 2021. During the period, the Group's revenue was RMB 12.9 billion (+4.0% yoy). The Gross profit margin is 26.3% (+3.0% yoy) and the net profit is RMB 1.1 billion (+47.1% yoy). The performance of the third quarter of 2021 was under pressure. Major domestic customers (such as OPPO, Vivo) delayed or cancelled some models due to the chip shortages, which led to weaker demand and the impact of overseas epidemics, resulting in a decline in the gross profit margin of Android's acoustics business. In 3Q21, the revenue was RMB 4.25 billion (-6.1% yoy) and the gross profit margin was 22.7% (-0.9 ppts yoy), while net profit and net profit margin are RMB 180 million and 4.3% (-57.4% and -5.2 ppts yoy respectively). Looking ahead to the fourth quarter, the company's performance is expected to increase qoq, and the year-on-year growth in net profit for the full-year net profit forecast is revised down by approximately 23% (previous estimation: RMB 2.05 billion)

Increased proportion of Android acoustic products, the gross profit margin in 4Q21 is expected to rebound from 3Q21

In 3Q21, the company's acoustic business revenue was RMB 2.20 billion (+1.9% yoy and +7.8% qoq). The gross profit margin was 26.3% (-0.3ppts yoy and -2.1 ppts qoq). Mainly due to the impact of the overseas epidemic that continued into the third quarter, the gross profit margin of Android acoustic products dropped by 7.4ppts. As the Vietnam factory has fully resumed normal production in the fourth quarter, the production capacity and yield have been improved, and the company's standardized small-cavity acoustic modules accounted for close to 10% of Android acoustic products, and continued to improve. The increase in shipments of standardized products us expected to further increase the gross profit margin of Android acoustic products and by gradually penetrating the low-end smart phone market to increase the company's customer base. In addition, the company is cooperating with a well-known Chinese domestic automotive OEM to co-develop an audio system in smart cockpit for its new concept car. At the same time, the company is also cooperating with a leading Chinese electric vehicles manufacturer to co-develop mass-produced products. It is expected that the company's in-vehicle acoustic system products will be installed on new models in the future.

Performance of optical business under pressure in the third quarter

In 3Q21, the company's optical business revenue was RMB 390 million (-17.6% yoy and -51.6% qoq). The gross profit margin was 15.0% (-9.6ppts yoy and -7.0 ppts qoq) Mainly due to the shortage of upstream chips and raw materials, domestic customers postponed and cancelled some models of mobile phone, resulting in weaker demand. After excluding in the shipments of self-supplied modules, the company's plastic lens shipments dropped by 56.6% qoq, and 6P shipments remained at about 11%. Due to the lower capacity utilization level and average unit price, the gross profit margin of plastic lenses in the third quarter fell by 8.7 ppts from the previous quarter to 24.7%. It is expected that the shortage of upstream chips in the the fourth quarter will be alleviated, and the company's customers` orders will resume. Shipments and gross profit margin will pick up. The monthly shipments of optical modules decreased by 21.3% qoq and shipments were about 5 million. It is expected that shipments of optical modules will resume in the fourth quarter.

Non-smart phone business of precision structural parts improves

In 3Q21, the company's electromagnetic drives and precision mechanics business revenue was RMB 1.4 billion (-7.9% yoy and 14.5% qoq). The gross profit margin was 20.3% (+0.2% yoy and -1.9% qoq). In terms of precision structural parts business, its shipment volume increased by 33.8%. At the same time, the company has accelerated its entry into the notebook computer and tablet computer market. The company's acquisition on Toyo Precision is expected to bring synergies to the existing precision mechanics business. It is expected that the non-smart phone business revenue will account for more than 15% of the precision structural parts in the end of 2021. In terms of electromagnetic drives business, 3Q21 Android client horizontal linear motor shipments doubled yoy. Through the launch of an integrated “hardware+ software” customer's upgrade and increase market share, it is meeting the needs and promotion of high-, middle- and low-end Android customers` mobile phones. With customer product upgrades, the market penetration rate of the company's products will be increased.

Multi-dimensional expansion of the MEMS market

In 3Q21, the company's revenue from the MEMS business was RMB 254 million (-31.1% yoy and +6.5% qoq). The gross profit margin was 15.3% (-3.7 ppts and -0.6 ppts qoq). Mainly due to the rise in the price of upstream chips, the production cost has risen, and the prices of major customers` products have fallen. With the gradual increase in the proportion of self-made MEMS microphone chips, the production cost will be reduced. It is expected that the company's MEMS microphones will expand to TWS headsets, smart speakers, tablets, vehicles, and other markets while maintaining a high market share in the smartphone market.

Company valuation

We lowered the net profit forecast for 2021/ 2022/ 2023 to RMB 1.58/ 2.14/ 2.74 billion, and the compounded annual growth rate for 21-23 is 31.9%. The main consideration is that the shortage of the mobile phone industry supply chain in the fourth quarter will be alleviated, the company's gross profit margin will increase in the fourth quarter, and the proportion of the Android customer base will gradually increase. The new WLG glass-plastic hybrid lens project will start in the fourth quarter. Therefore, the company maintains its P/E ratio of 25.0x, and the target price is lowered to HKD 38.35 which corresponds to the stock P/E ratio of 25.0x/ 18.4x/ 14.4x in 2021/ 2022/ 2023, which is downgraded to an “Accumulate” rating.

Financial

Click Here for PDF format...