Company Profile

JD Logistics (JDL) is the leading technology-driven supply chain solutions and logistics services provider in China. Began with the establishment of JD Group's in-house logistics department in 2007, JDL have then opened up own solutions and services to external customers since 2017, and offer a full spectrum of supply chain solutions and high-quality logistics services enabled by technology, ranging from warehousing to distribution, spanning across manufacturing to end-customers, covering regular and specialized items. In 2020, JDL served more than 190,000 corporate customers across a wide array of industries, such as fast moving consumer goods (FMCG), apparel, home appliances, home furniture, 3C, automotive and fresh produce, among others.

2020 Interim & Third Quarter Business Performance

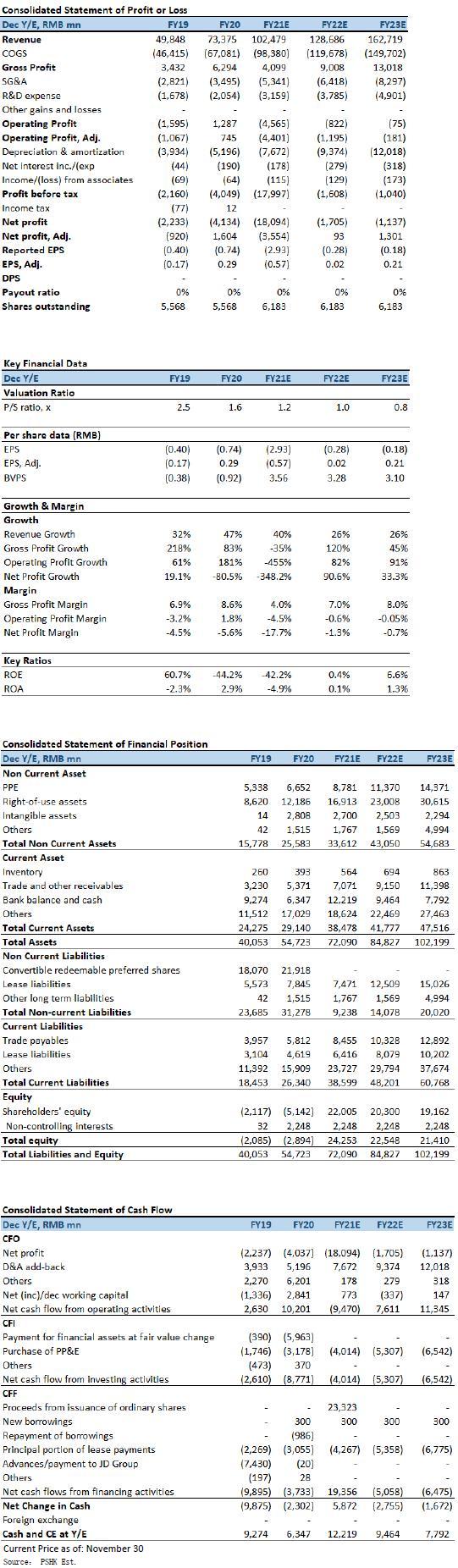

In 1H2021, JDL total revenue increased by 53.7% YoY to RMB48.5 billion, with gross profit dropped 56.4% YoY to RMB1.8 billion for the six months ended June 30, 2021. Gross profit margin to decrease to 3.7% (-9.2ppt) and primarily due to the reduction in benefits from COVID-19 related government support and in the second half of 2020 JDL's efforts in enhancing and expanding logistics networks including increases in headcount of operational personnel, warehouse space, line-haul routes and other logistics infrastructure. As a result of the foregoing, JDL generated a loss of RMB15.2 billion for the six months ended June 30, 2021. non-IFRS (loss) RMB1.5 billion for the period (profit RMB1.982 over a year ago), which is excluding share-based payments, listing expense, amortization of intangible assets resulting from acquisitions, fair value changes of financial assets at fair value through profit or loss, and fair value changes of convertible redeemable preferred shares. The results for the three months ended 30 September 2021, JDL recorded an operating loss of RMB727 million during the period, against the operating profit of RMB83.549 million over a year ago. 3Q21 revenue grew by 43.34% YoY to RMB25.75 billion.

Logistics network create moat

Logistics infrastructure and Networks is the foundation and core competitive advantage of JDL. As of June 30, 2021, JDL's warehouse network covered nearly all counties and districts in China, consisting of approximately 1,200 (vs. 900 in December 31, 2020) self-operated warehouses and over 1,600 (vs. 1400 in December 31, 2020) owner-operator cloud warehouses under JDL's Open Warehouse Platform. JDL's warehouse network has an aggregate GFA of approximately 23 million square meters (vs. 21 million square meters in December 31, 2020).

From the perspective of operational efficiency, JDL able to directly transport and store customers` inventory in the warehouses nearest to the end consumers, systematically shortening the fulfillment time to ensure speedy delivery. In 2020, approximately 90% of the total online retail orders processed for JD Group through JDL's network delivered on the same day or the day after the order was placed, with over 60% of the total online retail orders covered by the 211 program (deliver any orders received by the morning deadline 11:00 a.m. on the same day, and any orders received by the evening deadline 11:00 p.m. by 3:00 p.m. on the following day).

JDL employed approximately 200,000 in-house delivery personnel and operated approximately 7,800 delivery stations covering 32 provinces and municipalities and 445 districts in different cities and municipalities in China. The vast majority of JDL's delivery stations are self-operated to ensure high-quality service. During JD Group's 618 Grand Promotion, i.e. the shopping festival from June 1 to June 18, JDL provided outstanding delivery experiences to the customers, with delivery within minutes of order placement in over 200 cities across the country and same- or next-day delivery covering 92% of districts and counties and 84% of townships in China.

For cold chain logistics network, JDL had over 100 temperature-controlled cold storage warehouses designated for fresh, frozen and refrigerated products with an operation area of more than 600,000 square meters. In addition, as of June 30, 2021, JDL operated 23 warehouses designated for pharmaceuticals and medical instruments with an operation area of 160,000 square meters.

For cross-border logistics network, in the second quarter of 2021, JDL flew inaugural flights on two brand-new charter flight routes, from China to Thailand and from China to the U.S. The China-Thailand route enables next-day delivery from China to Thailand, deliveries within Thailand and from Thailand to China as fast as same-day, and door-to-door within 48 hours.

Integrated supply chain business model

JDL categorize their customers based on whether they have utilized the warehouse or inventory management related services, and customers who have utilized JDL warehouse or inventory management related services in the recent past are classified as integrated supply chain customers. In fact, JDL primarily serve corporate customers, including JD Group. JDL provides supply chain solutions and logistics services to customers across a wide range of industries, such as FMCG, apparel, home appliances, home furniture, 3C, automotive and fresh produce.

In 1H2021, JDL revenue from integrated supply chain customers grew 29.6% YoY to RMB33.6 billion, of which the revenue from external integrated supply chain customers reached to RMB11.7 billion, representing 65.6% YoY growth. The number of external integrated supply chain customers reached 59,067, expanding 58.7% YoY. ARPC was RMB197,339 in the 1H2021.

Revenue from other customers increased by 164.8% YoY in the 1H2021 to RMB14.9 billion, driven by an increase in the number of customers served. Standard products such as express delivery and freight delivery services not only help JDL expand customer pool but also serve as a gateway for integrated supply chain logistics services.

Integrated supply chain poised structural growth

China is the largest logistics market in the world in terms of logistics spending. China's total logistics spending reached RMB14.9 trillion in 2020, and is expected to grow at a CAGR of 5.3% from 2020 to 2025. China's logistics spending is generally in line with the growth in GDP, which is expected to grow at a rate of 6.2% from 2020 to 2025 as domestic consumption and trade activities continue to increase, leading to additional logistics demands.

As businesses grow, buyers or sellers face more sophisticated customer needs, making it more challenging for them to handle the increasing volume and complexity in customer demands. Also, due to constraints in logistics infrastructure and resources, 1PL often fail to achieve the same level of efficiency compared to the services offered by professional third-party logistics service providers who have best-in-class infrastructure and operational know-how. In addition, by outsourcing logistics services to third-party service providers, enterprises can focus on their core businesses without the need to deal with the complex and resource consuming logistics planning process. As a result, the outsourced logistics services market in China has grown rapidly and is expected to grow from RMB6.5 trillion in 2020 to RMB9.2 trillion in 2025, representing a CAGR of 7.1%, which is faster than the growth in total logistics spending during the same period, which is 5.3%.

Integrated supply chain logistics service providers possess the competencies of providing a full spectrum of logistics services, ranging from express delivery, full truckload and less-than-truckload transportation, last-mile delivery, warehousing, and other value-added services (such as home installation and aftersales services), which are offered to customers in the form of integrated solutions tailored to their varied needs. Despite the fact that the majority of demand for third-party logistics services comes from single logistics services, demands from enterprises for outsourced supply chain logistics services have gradually transitioned from homogeneous to manifold, leading to the integrated supply chain logistics services market outgrowing the outsourced logistics service market in general.

The market size of the integrated supply chain logistics services industry in China reached RMB2,026 billion in 2020, and is expected to further increase to RMB3,190 billion by 2025, growing at a CAGR of 9.5%. Integrated supply chain logistics services penetration, as defined by integrated supply chain logistics services spending divided by outsourced logistics services spending, is also expected to increase from 31.0% in 2020 to 34.6% in 2025.

Company valuation

JDL is one of the largest integrated supply chain logistics service providers in China. We forecast a revenue CAGR of 30% in 2020 - 2025 (while JDL past revenue growth was 42%), driven by: 1) the growth of China's logistics spending in line with GDP growth, which increase the penetration of outsourcing logistics service, and growing demand for outsourcing supply chain logistics services has led to the structural growth of the integrated supply chain logistics service; 2) JDL market-share gains continue through its highly integrated logistics infrastructure, technology capabilities, industry know-how, and significant revenue by serving JD Group and external customers.

We expect JDL to breakeven next year, and our PT of HK$41.55 is based on 2022E revenue and P/S multiple of 1.65x, which is basically in line with SF Holding (SZ.002352).

Risk factors

1) Slow down in domestic growth and consumer spending; 2) Unexpected drop in GMV growth of JD.com, in which significant revenue contribution for 54% of JDL's revenue in 2020; and 3) Higher than expected increase in staff and outsourcing costs, as these two cost factors have signicant impact on JDL's earnings.

Financial

Click Here for PDF format...