Sectors:

Air & Automobiles (Zhang Jing),

TMT (Samuel Sung)

Automobile & Air (ZhangJing)

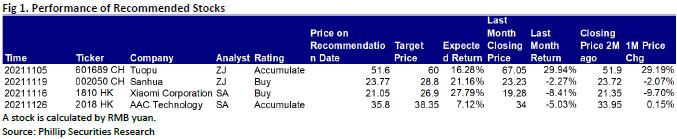

This month I released 2 updated reports of Tuopu (601689.CH), and Sanhua (002050.CH) which got success by their unique Competitive edge. Among them, we highly recommend Tuopu .

n the first three quarters of 2021, Tuopu Group recorded an operating revenue of RMB7,823 million, up 81.14% yoy; net profit attributable to the parent company of RMB753 million, up 94.44% yoy; net profit attributable to the parent company excluding non-recurring items of RMB731 million, up 103.47% yoy. The basic EPS was RMB0.69, a year-on-year growth of 86.49%. Specifically, in the third quarter, the Company reported a revenue of RMB2,906 million, up 65.44% yoy or 16.70% qoq; net profit attributable to the parent company of RMB294 million, up 71.26% yoy or 37.43% qoq.

Since this year, recovery in the global auto market has been hit by chip shortages. In this context, Tuopu Group bucked the trend with substantial growth that is significantly better than the industry level. The main reason is that the Company has actively expanded to the NEV lightweight chassis and automotive electronics over the years, and has gradually seen effect in its transformation. Besides, thanks to its forward-looking layout, it has received a great number of orders, with the localized Tesla project making significant contribution in order increment. Also, the rising sales in the supporting models of other core customers have brought rapid growth in operating results.

With its excellent vehicle synchronous R&D capability, strategic forward-looking layout, the Company fixed its partnership with downstream customers in advance and has begun to harvest orders. In terms of lightweight chassis, the Company's aluminum alloy integrated vacuum cast chassis has been recognized by Ford, RIVIAN and other customers and mass production has started. The value of single vehicle in cooperation with RIVIAN has reached RMB11,000. As for thermal management system, the integrated heat pump assembly and electronic expansion valve, electronic water valve, electronic water pump developed by the Company have been recognized by customers, and the Company is expected to become the overall solution provider in new energy thermal management, with the overall value of single vehicle up to RMB6,000 to RMB9,000. With respect to intelligent driving control system, IBS products, as the two core executors of ADAS, are making efforts to match with intelligent steering system EPS, which are expected to be a new growth point for the Company in the future.

Meanwhile, the Company has implemented the Tier0.5 business model by which it has gradually gained the recognition of intelligent electric vehicle enterprises. In this model, the Company can get more orders with more supporting products for single vehicle and higher sales amount.

TMT (Samuel Sung)

This month I released 2 updated reports of Xiaomi (1810.HK) and AAC Technology (2018.HK). Among them, we highly recommend AAC Technologies.

AAC Technology announced the company's interim results as of 30 September 2021. During the period, the Group's revenue was RMB 12.9 billion (+4.0% yoy). The Gross profit margin is 26.3% (+3.0% yoy) and the net profit is RMB 1.1 billion (+47.1% yoy). The performance of the third quarter of 2021 was under pressure. Major domestic customers (such as OPPO, Vivo) delayed or cancelled some models due to the chip shortages, which led to weaker demand and the impact of overseas epidemics, resulting in a decline in the gross profit margin of Android's acoustics business. In 3Q21, the revenue was RMB 4.25 billion (-6.1% yoy) and the gross profit margin was 22.7% (-0.9 ppts yoy), while net profit and net profit margin are RMB 180 million and 4.3% (-57.4% and -5.2 ppts yoy respectively). Looking ahead to the fourth quarter, the company's performance is expected to increase qoq, and the year-on-year growth in net profit for the full-year net profit forecast is revised down by approximately 23% (previous estimation: RMB 2.05 billion)

In 3Q21, the company's acoustic business revenue was RMB 2.20 billion (+1.9% yoy and +7.8% qoq). The gross profit margin was 26.3% (-0.3ppts yoy and -2.1 ppts qoq). Mainly due to the impact of the overseas epidemic that continued into the third quarter, the gross profit margin of Android acoustic products dropped by 7.4ppts. As the Vietnam factory has fully resumed normal production in the fourth quarter, the production capacity and yield have been improved, and the company's standardized small-cavity acoustic modules accounted for close to 10% of Android acoustic products, and continued to improve. The increase in shipments of standardized products us expected to further increase the gross profit margin of Android acoustic products and by gradually penetrating the low-end smart phone market to increase the company's customer base. In addition, the company is cooperating with a well-known Chinese domestic automotive OEM to co-develop an audio system in smart cockpit for its new concept car. At the same time, the company is also cooperating with a leading Chinese electric vehicles manufacturer to co-develop mass-produced products. It is expected that the company's in-vehicle acoustic system products will be installed on new models in the future.

In 3Q21, the company's optical business revenue was RMB 390 million (-17.6% yoy and -51.6% qoq). The gross profit margin was 15.0% (-9.6ppts yoy and -7.0 ppts qoq) Mainly due to the shortage of upstream chips and raw materials, domestic customers postponed and cancelled some models of mobile phone, resulting in weaker demand. After excluding in the shipments of self-supplied modules, the company's plastic lens shipments dropped by 56.6% qoq, and 6P shipments remained at about 11%. Due to the lower capacity utilization level and average unit price, the gross profit margin of plastic lenses in the third quarter fell by 8.7 ppts from the previous quarter to 24.7%. It is expected that the shortage of upstream chips in the the fourth quarter will be alleviated, and the company's customers` orders will resume. Shipments and gross profit margin will pick up. The monthly shipments of optical modules decreased by 21.3% qoq and shipments were about 5 million. It is expected that shipments of optical modules will resume in the fourth quarter.

Click Here for PDF format...