Investment Summary

Company Profile

Minth Group is a world-renowned supplier engaged in the design, manufacturing and sales of automotive interior and exterior trim and body structure parts. The domestic market share of its core products exceeds 30%. The company has production bases in China, the United States, Mexico, Thailand, Germany, Serbia and other countries, and its customers cover major vehicle companies in the market. Based on a variety of new materials and surface treatment technologies, in recent years the company has developed new electrified and smart product lines such as aluminum power battery boxes and smart front faces, forming a series of competitive terminal products.

Minth Group Reports Steady Profit Growth That Basically Meet Expectations

In H1 of 2021, Minth Group recorded a turnover of RMB6.66 billion, up 37.3% yoy; the net profit attributable to the parent company registered RMB901 million, up 143.7% yoy; the gross profit margin was 31.9%, up 5.3 ppts yoy. Major automobile markets in China, North America and Europe gradually recovered from the pandemic in the same period last year. In addition, the Company's main customers displayed good performance. In particular, in the domestic market, the production and sales of Japanese car companies was generally stable, and the market share of Chinese car companies has increased. In overseas markets, the growth rate of production and sales of luxury car brand companies was generally above the market average. Therefore, the Company has achieved strong growth in turnover. Meanwhile, benefiting from the scale effect brought by the increase in turnover and the rise in the proportion of aluminum products with a high gross profit margin, the gross profit margin increased significantly compared with the same period of the previous years. Besides, the net profit saw a triple-digit increase due to a gain of RMB190 million generated from the disposal of subsidiaries during the period under review.

Compared with H2 of 2020, the revenue and net profit fell by 12.6% and 12.1% mom, respectively. Mainly due to the global chip shortage in H2 and the month-on-month increase in raw materials and transportation and logistics costs, the gross profit margin also dropped by 1.9 ppts mom..

The Battery Housing Business Exerts Full Strength, and New Orders Continue to Rise

In H1, the Company's four major products, namely metal and trim products, plastic products, aluminium products and battery housings, reported operating revenue of RMB2.35 billion, RMB1.96 billion, RMB1.74 billion and RMB90 million, respectively, up 13.9%, 35.3%, 30.5% and 61.2% yoy, respectively. The battery housing business has exerted full strength: In H1, the Company obtained orders for all battery housings for Daimler and Groupe PSA's eVMP platform. In H2, the battery housings for ten models will be mass-produced, and the turnover will increase significantly. It is estimated that the revenue from the battery housing business will reach RMB400 million this year, exceed RMB2 billion next year, and outstrip RMB4 billion in the following year.In H2, the Company's new orders continued to hit a record high. The annual contract amount reached RMB5.9 billion, of which overseas markets accounted for 52%, innovative products occupied 35%, and new energy vehicles took up for 48%. In terms of intelligent products, the Company has obtained orders for radomes from Daimler, Toyota and Nissan, and orders for light-emitting products from GM and Geely. For the first time, the Company undertook variable spoiler products.

In terms of traditional products, Minth Group has obtained orders for aluminium trim products for most models on Daimler's MMA platform, orders for stainless steel trim products for all new dedicated models of Volkswagen and Skoda in Europe, and orders for aluminium trim products for Tesla Model Y in North America. In addition, the Company continuously penetrated into existing and new customers such as Toyota, Nissan, GM, Ford, Kia, Geely, and Xpeng to expand market share. The Company has increased its guidance on new orders throughout the year. It is expected that new orders will probably exceed RMB9.5 billion.

Minth Group Further Expands Overseas Markets, and its Relisting on the A-share Market Is Expected to Boost Development Prospects

In H1, the Company's revenue from the domestic market reached approximately RMB3.79 billion, an increase of approximately 33.9% over the same period; the turnover in overseas markets registered approximately RMB2.87 billion, a year-on-year increase of approximately 42.2%. Benefiting from the increase in orders from customers such as BMW, Audi, Daimler, GM, and Tesla, the Company's overseas business revenue will continue to increase.

The Company applied for the issuance of A shares and the listing on the Science and Technology Innovation Board of the Shanghai Stock Exchange. The initial funding amount is RMB6.5 billion, of which approximately 40% will be used for the capacity expansion and upgrading of the Company's main products, approximately 15% will be used for the capacity expansion of battery housings, and approximately 10% will be used for the technical development of intelligent exterior products and automotive battery housings. As the industrial chain of new energy vehicles are further well-developed, in the future, Europe, U.S., Japan, and China will accelerate the large-scale layout, driving a continuous upward boom of the battery housing industry. The Company has taken the lead in the layout of the battery housing business. The enhanced fundraising will help the Company further shape its product advantages and maintain a leading position.

Valuation

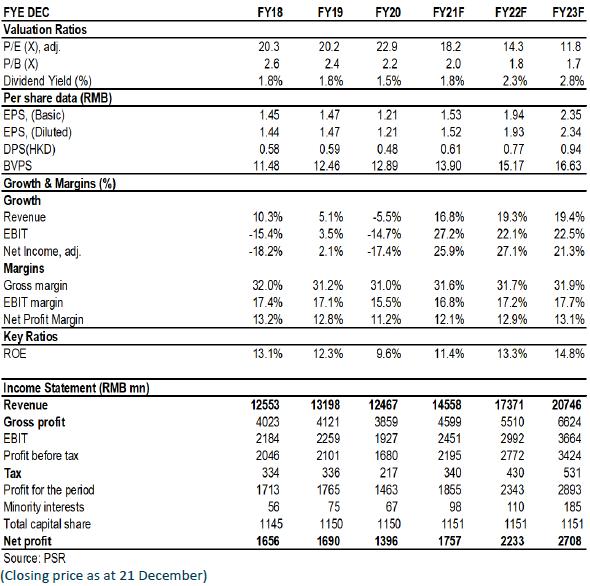

We revised the forecast of EPS of 2021/2022/2023 to be RMB1.53/1.94/2.35 yuan. And we believe that it is reasonable to give the company a valuation of 22.9/18.0/14.8x P/E and 2.5/2.3/2.1x P/B for 2021/2022/2023, equivalent to target price of HK$ 41.4 and BUY rating. (Closing price as at 21 December)

Financials

Click Here for PDF format...