Sectors:

Air & Automobiles (Zhang Jing),

Logistics (Eric Li)

Soft Beverage (Chloe Chan)

Automobile & Air

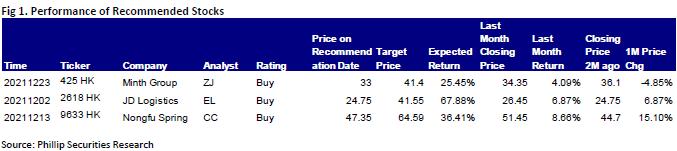

This month I released updated reports of Minth Group (425.HK).

Looking back at 2021, the growth rate of China's automobile market experienced great ups and downs. In Q1, due to the continued sales enthusiasm and the low base of the epidemic in the same period last year, it increased significantly year-on-year; since the second and third quarters, the chip supply collapsed due to the severe epidemic especially in Southeast Asia, and the raw material prices surged to a record high, the growth rate has fallen sharply; as these headwinds gradually subsided, car sales began to improve in the fourth quarter, and continued to increase month-on-month, but they still did not turn positive year-on-year. In the first eleven months of 2021, the cumulative vehicle sales volume was 23.489 million, an increase of 4.5% year-on-year. On the other hand, multiple positive factors have resonated. New energy vehicles have been favored by the market. Production and sales have increased significantly year-on-year. In the first eleven months, the cumulative sales of new energy vehicles nationwide reached 2.99 million units, an increase of 1.7 times year-on-year. We believe that the intelligentization and electrification of the automobile market is the general trend. Among them, the localized substitution of high-end parts is a bright spot, and attention should be focused on those high-quality parts suppliers, such as Minth Group.

In H1 of 2021, Minth Group recorded a turnover of RMB6.66 billion, up 37.3% yoy; the net profit attributable to the parent company registered RMB901 million, up 143.7% yoy; the gross profit margin was 31.9%, up 5.3 ppts yoy. Major automobile markets in China, North America and Europe gradually recovered from the pandemic in the same period last year. In addition, the Company's main customers displayed good performance. In particular, in the domestic market, the production and sales of Japanese car companies was generally stable, and the market share of Chinese car companies has increased. In overseas markets, the growth rate of production and sales of luxury car brand companies was generally above the market average. Therefore, the Company has achieved strong growth in turnover. Meanwhile, benefiting from the scale effect brought by the increase in turnover and the rise in the proportion of aluminum products with a high gross profit margin, the gross profit margin increased significantly compared with the same period of the previous years.

The battery housing business has exerted full strength: In H1, the Company obtained orders for all battery housings for Daimler and Groupe PSA's eVMP platform. In H2, the battery housings for ten models will be mass-produced, and the turnover will increase significantly. It is estimated that the revenue from the battery housing business will reach RMB400 million this year, exceed RMB2 billion next year, and outstrip RMB4 billion in the following year. The Company has increased its guidance on new orders throughout the year. It is expected that new orders will probably exceed RMB9.5 billion.

We believe that it is reasonable to give the company a valuation of 22.9/18.0/14.8x P/E and 2.5/2.3/2.1x P/B for 2021/2022/2023, as it is assured that there will be a strong result momentum because the Company has abundant orders, high-quality customer structure, gradual mass production of new models and huge improvement prospects in overseas business, equivalent to target price of HK$ 41.4 and BUY rating.

Logistics

This month I have released 1 report on JD Logistics (2618.HK).

JD Logistics (JDL) is the leading technology-driven supply chain solutions and logistics services provider in China. Began with the establishment of JD Group's in-house logistics department in 2007, JDL have then opened up own solutions and services to external customers since 2017, and offer a full spectrum of supply chain solutions and high-quality logistics services enabled by technology, ranging from warehousing to distribution, spanning across manufacturing to end-customers, covering regular and specialized items. In 2020, JDL served more than 190,000 corporate customers across a wide array of industries, such as fast moving consumer goods (FMCG), apparel, home appliances, home furniture, 3C, automotive and fresh produce, among others.

In 1H2021, JDL total revenue increased by 53.7% YoY to RMB48.5 billion, with gross profit dropped 56.4% YoY to RMB1.8 billion for the six months ended June 30, 2021. Gross profit margin to decrease to 3.7% (-9.2ppt) and primarily due to the reduction in benefits from COVID-19 related government support and in the second half of 2020 JDL's efforts in enhancing and expanding logistics networks including increases in headcount of operational personnel, warehouse space, line-haul routes and other logistics infrastructure. As a result of the foregoing, JDL generated a loss of RMB15.2 billion for the six months ended June 30, 2021. non-IFRS (loss) RMB1.5 billion for the period (profit RMB1.982 over a year ago), which is excluding share-based payments, listing expense, amortization of intangible assets resulting from acquisitions, fair value changes of financial assets at fair value through profit or loss, and fair value changes of convertible redeemable preferred shares.

In 1H2021, JDL revenue from integrated supply chain customers grew 29.6% YoY to RMB33.6 billion, of which the revenue from external integrated supply chain customers reached to RMB11.7 billion, representing 65.6% YoY growth. The number of external integrated supply chain customers reached 59,067, expanding 58.7% YoY. ARPC was RMB197,339 in the 1H2021.Revenue from other customers increased by 164.8% YoY in the 1H2021 to RMB14.9 billion, driven by an increase in the number of customers served. Standard products such as express delivery and freight delivery services not only help JDL expand customer pool but also serve as a gateway for integrated supply chain logistics services.

The results for the three months ended 30 September 2021, JDL recorded an operating loss of RMB727 million during the period, against the operating profit of RMB83.549 million over a year ago. 3Q21 revenue grew by 43.34% YoY to RMB25.75 billion.

JDL is one of the largest integrated supply chain logistics service providers in China. We forecast a revenue CAGR of 30% in 2020 - 2025 (while JDL past revenue growth was 42%), We expect JDL to breakeven next year, and our PT of HK$41.55 is based on 2022E revenue and P/S multiple of 1.65x, which is basically in line with SF Holding (SZ.002352).

Soft Beverage

This month I have released 1 report on Nongfu Spring Co., Ltd. (2618.HK).

Nongfu Spring has been pursuing the “dual-engine” development of drinking water and beverages. On one hand, it meets the daily drinking needs of consumers and on the other hand, it satisfies the diverse and personalized drinking demands of consumers. Diversified product varieties enhancing flexible product mixes has enabled companies and distributors to achieve differentiating advantages in different markets and channels, to improve scale of business, distribution efficiency and profitability.

Nongfu Spring's packaged drinking water products include natural drinking water and natural mineral water. The company is the second largest packaged drinking water company in the world in terms of sales volume. It is also the only company, among the top 5 PRC packaged drinking water companies, that uses solely natural water to produce packaged drinking water, pledging "Every drop of Nongfu Spring has its source". In 2020, the company's market share of packaged drinking water in China reached 20.9% (in terms of retail sales value), which is 1.5 times that of the second largest player. In 2018, 2019 and 2020, the revenue generated from packaged drinking water products accounted for 57.5%, 59.7% and 61% of the company's total revenue, respectively.

Nongfu Spring's gross margin of 59.1% in 2020 is well ahead of its peers, Tingyi Holding Corp.(33.2%) and Uni-President(34.4%); and is comparable to Coca-Cola(59.3%), the No. 1 soft drink company in the global soft beverage industry. Net profit levels were also much higher than the average in the soft beverage industry in China and also globally over the same period, reaching 17.6%, 20.6% and 23% in 2018, 2019 and 2020. High profitability levels are expected to remain stable in the long term.

Nongfu Spring's sales network is nationwide, accounting for approximately 11% of the 22 million retail points of sale in China, covering a wide area and not limited to first and second tier cities. The Company has partnered with local distributors who have extensive experience in the distribution of soft beverage products, leveraging their financial strength, professional teams and facilities to penetrate the local retail network. Besides, the "Nongfu Spring" branded refrigerators installed at nearly 500,000 retail points of sale have particularly enhanced the Company's brand display and share of shelf, thereby boosting sales volume. The Company's annual evaluation and screening of distributors has helped the distributors to improve their business capabilities, so that the overall quality and business capabilities of the cooperating distributors have gradually stabilized and matured.

Nongfu Spring is the leader in the soft beverage industry, with a significantly faster growth rate than the industry average in all its product categories. In addition, fruit juice, tea beverage and functional beverage products are bringing new development focus to the company. With reference to the average valuation of the company in the past year, we give the company a minus 1 standard deviation target P/E ratio of 63x for 2022, and estimate the company's EPS for 2021/2022/2023 to be RMB 0.7/0.8/1.0. The target price forecast for 2022 is HK$64.59, which corresponds to PE ratio of 74.1x/ 63x/ 53.5x for 2021/2022/2023 respectively. The Company is given a “Buy” rating (initial coverage).

Click Here for PDF format...