Company Profile

Currently, GAC's major segments cover R&D, vehicle (automobiles and motorcycles), parts, commerce services, financial services, and mobile travel service, developing a complete cycle of the automotive industry chain. By adhering to the strategy of "joint ventures + self-owned brands", the Company owns six major brands including GAC Honda, GAC Toyota, GAC Motor, GAC Aion, GAC FCA, and GAC Mitsubishi, as well as many best-selling models. GAC currently has a market share of 8.1% in China, ranking first in the market share of mid-to-high-end sedans.

Investment Summary

FY20 Profit Decreases by 10% yoy, Mainly Due to Impairment

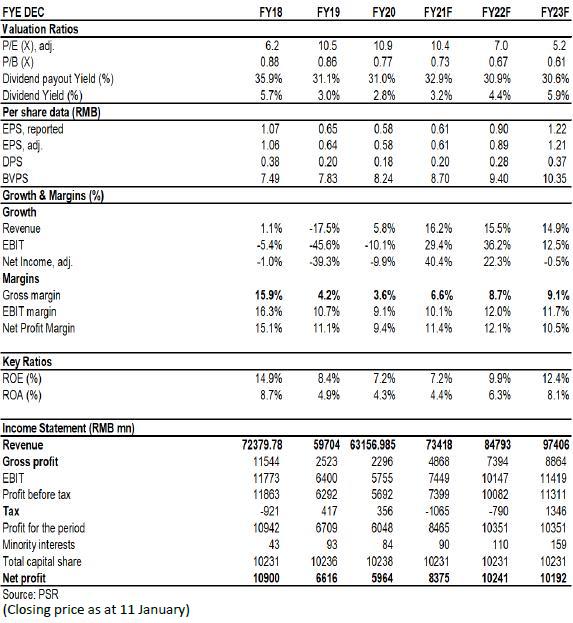

In 2020, GAC recorded operating revenue of RMB63,157 million, up by 5.78% Y-o-Y; net profit attributable to the parent company was RMB5,966 million, down by 9.85% Y-o-Y; in addition to the impact of COVID-19 pandemic, the decline in results was mainly due to the large accrued expenses in the fourth quarter (provision for asset impairment of RMB720 million in a lump sum). After deducting non-recurring gains and losses, net profit attributable to the parent company was RMB4,807 million, up by 25.17% Y-o-Y. Self-owned brands achieved loss reduction. After deducting non-recurring gains and losses and return on investment, net loss attributable to the parent company was RMB5.1 billion, down by 12% Y-o-Y. EPS was RMB0.58, down by 11% Y-o-Y. The final dividend was RMB0.15 per share. Combined with the interim dividend of RMB 0.03 per share, the dividend payout ratio was 31%.

Gross margin decreased by 0.38 ppts Y-o-Y, mainly due to the negative effect of scale caused by the decline in sales volume of self-owned brands. The period expense ratio for the whole year decreased by 2.1 ppts Y-o-Y, mainly because the sales expense ratio fell by 1.86 ppts, and other expense ratios remained flat Y-o-Y. The R&D expenses totaled RMB5.1 billion, of which 17% was expensed. Joint ventures had a good profitability. The annual return on investment was RMB9,911 million, up by 2.96% Y-o-Y. Specifically, the return on investment in associates and joint ventures was RMB9,571 million, up by 1.83% Y-o-Y. At the end of 2020, monetary funds were RMB28.5 billion and interest-bearing liabilities were RMB14.8 billion.

Japanese JVs Remain Strong Momentum While Self-owned Brands Make Continuous Improvement

In 2020, China's automobile market demonstrated a fall-rise pattern, with an overall decline of 1.9%, which is narrower than the previous year. GAC outperformed the industry relying on its strong Japanese brands. It achieved an annual sales volume of 2,043,800 units, down by approximately 0.9% Y-o-Y. Its market share increased to 8.07%. Specifically, Honda and Toyota still remained a strong momentum of growth. GAC Honda sold 805,800 units, up by 2.65% Y-o-Y; GAC Toyota reported an annual sales volume of 765,000 units, up by 12.2% Y-o-Y, far higher than the industry average.

GAC Honda and GAC Toyota Gradually Increase Q4 Sales Volume, and New Energy Vehicles Accelerate the Development

According to the latest sales data, since the fourth quarter, the sales volume of major automotive joint ventures has climbed month by month, reflecting that the chip shortage dilemma has been eased month by month. In Oct/Nov/Dec, GAC Honda sold 75.4/77.7/78.4 thousand units, +4.7%/+3.04%/+0.9% mom and -13.94%/-9.97%/-3.5% yoy respectively; As for GAC Toyota, it sold 61/85/99 thousand units, +26.29%/+39.34%/+15.9% mom and -15.3%/+9.82%/36.5% yoy. There was an obvious trend of recovery. Key models, such as Accord, Vezel, Levin, and Highlander, recorded good sales volume. Automotive joint ventures are starting a strong product cycle and speeding up the layout of new energy vehicles. The profitability is expected to rebound with the successive launch of new models, such as GAC Honda's Integra and e:NP1, and GAC Toyota's Sienna, Fenglanda, Venza, and bZ4X.

In terms of self-owned brands, GAC's self-owned brands sold 47/50.6/32.2 thousand units in Oct/Nov/Dec, +29.8%/+6.8%/-9.6% mom and +25.4%/+24.7%/+2.2% yoy. Specifically, the sales volume of Trumpchi Empow has exceeded 10 thousand units for two consecutive months. GAC Aion, a new energy vehicle brand, had strong terminal demand. Its shipments were second only to that of Tesla and BYD, and the sales volume has exceeded 10 thousand units for seven consecutive months. The new second-generation GS8 equipped with THS was launched in December. Aion LX Plus, which has a super miles range of over 1,000 km, is expected to be launched early 2022. In 2022, GAC Aion will have a new production capacity of 100 thousand units per year. The proportion of new energy vehicles is expected to be further increased. Recently, the asset reorganization and capital increase plan of GAC Aion has been determined, which will accelerate the launch process. In the future, GAC Aion's net assets will exceed RMB10 billion, and it will have complete R&D capabilities of new energy pure electrically-powered vehicles, independent production plant and its own pipelines. The accumulation of funds and technology and the improvement of efficiency will help GAC Aion store energy for the development of new energy vehicles.

Investment Thesis

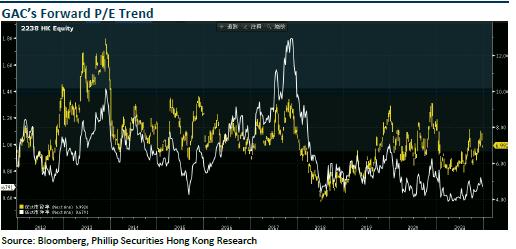

We expect that under the trend of accelerating the electric and intelligent layout, the Company's joint venture brands with Japanese companies will continue to expand their advantages. Self-owned brands are also expected to open up room for growth. We revised the Company's 2021/2022 and introduced 2023 earnings forecast. We maintain the "Buy" rating with the target price to HKD 10.3, equivalent to 14.2/9.6/7.1x P/E and1.0/0.9/0.8x P/B ratio in 2021/2022/2023. (Closing price as at 11 January)

Financials

Click Here for PDF format...