Company Profile

Established in 2003, 361 Degrees International Limited (361 Degrees) is an integrated sportswear enterprise which principally engages in brand management, research and development, design, manufacturing and distribution in China and across the globe. Its comprehensive product portfolio comprises footwear, apparel, accessories under the 361° Core brand, 361° kids brand, and ONE WAY, an authentic Finnish brand focuses on higher functional and more specialized outdoor products. operates a distributorship business model through the first-tier exclusive distributors and second-tier authorized retailers to manage an extensive distribution network of over 6,000 retail stores across China and the world. It has established a leading position in third-tier and lower-tier cities in China.

4Q2021 Recorded High Teens Growth

The retail sales (in terms of the retail value) of 361 Degrees core branded products for the 4Q21 recorded high teens growth compared to the same period of 2020. The retail sales (in terms of the retail value) of kids branded products for the 4Q21 recorded 25 to 30% growth compared to the same period of 2020. Compared with the 3Q21, the retail sales core branded products and kids branded products for the 3Q21 recorded low teens and 15 to 20% YoY growth respectively, reflecting a further improvement in operations in the Q4. Meanwhile, the overall retail sales of E-commerce products for the 4Q21 recorded 35 to 40% growth compared to the same period of 2020.

1H2021 results summary

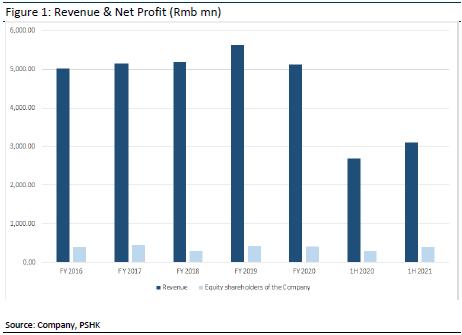

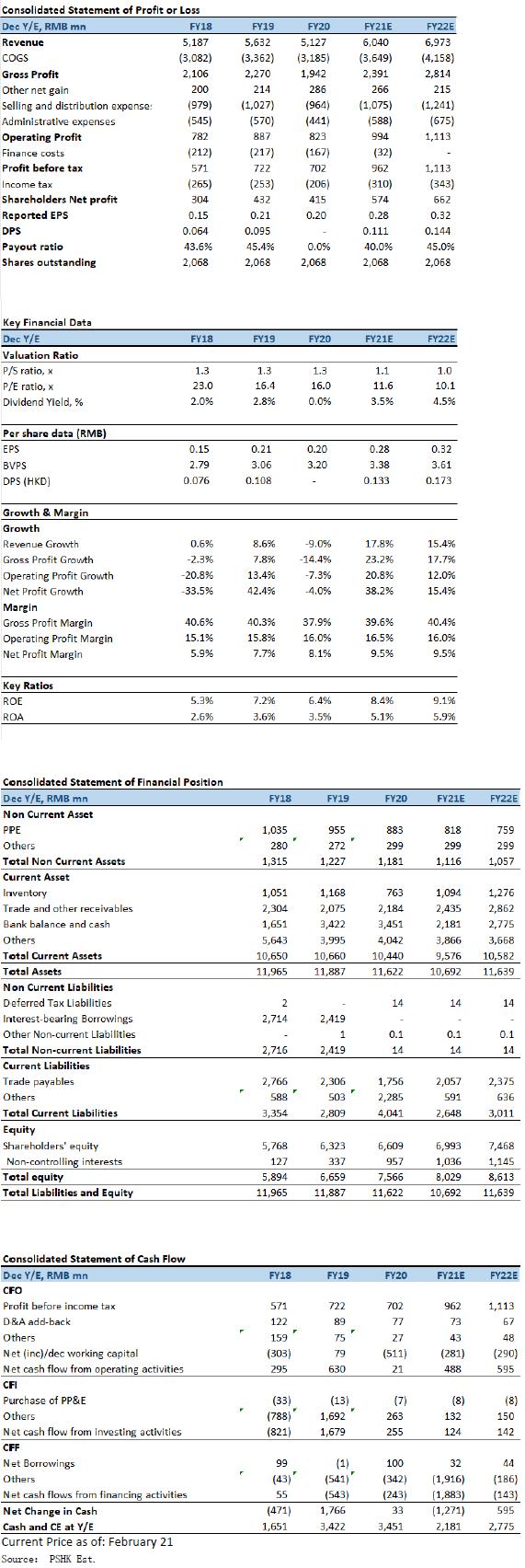

361 Degrees recorded a yoy increase of 15.7% in revenue to RMB3107.1million for the 1H2020. Net profit increased by 32.9% yoy to RMB401 million, which has exceeded the level of the same period before the epidemic in 2018 and 2019.

Revenue of the core brand business of 361 Degrees increased by 14.5% yoy; the revenue of footwear products was RMB1.381 billion, an increase of 22.5% yoy, and the proportion of revenue rose to 44.4%; the revenue of clothing products was RMB1.168 billion, increased by 6.1% yoy, and the proportion of revenue fell to 37.6%. In terms of sales volume, footwear and apparel products increased by 24.3% and 25.1% respectively yoy. In addition, the sales volume and average wholesale selling price of accessories increased by 10.9% and 9.9% yoy respectively, resulting in a 21.1% yoy increase in revenue from accessories sales.

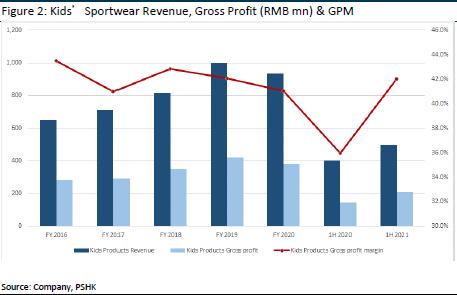

Kids' segment continues to grow faster

The Kids' segment grew the fastest, with revenue of RMB498 million during the period, an increase of 23.9% yoy, accounting for 16.0% of the total revenue. The increase was mainly due to a 22.9% yoy increase in sales volume and a 0.8% yoy increase in average wholesale price. Launched co-branded products with Captain Tsubasa, Minions and The Three-Body Problem, etc. through the strong and powerful core brand spokespersons and IP resource integration in the first half of 2021, with the aim of further differentiating its 361 Degrees Kids brand.

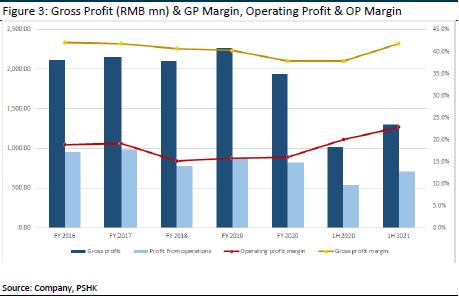

the gross profit margin of 361 Degrees during the period reached 41.8%, an increase of 4ppt yoy, which is the highest level in the same period since 2017. The gross profit margin (yoy change) of the four major business periods of footwear, apparel, accessories and 361 Degrees Kids' products was 43.1% (+1.8ppt), 41.2% (+5.2ppt), 39.3% (+11.9ppt) and 42.0% (+6.0ppt), mainly due to the improvement in the domestic retail market, an increase in the proportion of sales revenue generated from e-commence platform and the AWP of the distributors ‘products return to the normal level before the outbreak of epidemic.

For 1H2021, selling and distribution expenses increased by 30.8% yoy to RMB461.7 million (1H2020: RMB352.9 million). Advertising and promotional expenses increased by 25.1% yoy (1H2020: RMB197.7 million) and accounted for approximately 8.0% (+0.6 ppt) of the Company revenue. In addition, 361 Degrees restarted some sponsorship programs and took a more aggressive approach for advertising and promotion activities. The e-commerce business increased by 54.5% yoy to RMB487.8 million and accounted for approximately 15.7% of the total revenue. The major expenses incurred by the e-commence operation increased by 58.8% yoy. Administrative expenses increased by 15.3% yoy, which was similar to the increase in revenue. Operating profit margin increased by 2.9ppt to 22.9%.

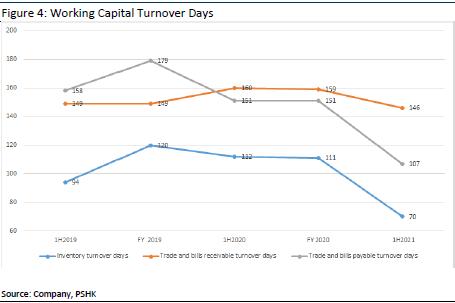

The operating efficiency of 361 Degrees has been improved. In 1H2021, the number of inventory turnover days decreased significantly from 41 days to 70 days yoy. The improved inventory turnover cycle was mainly due to the recovery in the market and the distributors’ more aggressive attitude on taking the delivery of the orders according to the expected timetable to meet the strong market demand, and improve the efficiency of sales channels, including: 1) Launching the ninth-generation image stores and fourth-generation retail outlets under the brand of 361º Kids to upgrade the professional image of the store, and encourages its distributors and their authorised retailers to open larger stores in shopping malls and department stores in the future while rationalising the retail network by closing down smaller stores so as to optimise the distribution channel mix, enriched the shopping experience and effectively improved the stores’ efficiency. As at 30 June 2021, core brand’s retail network and points-of-sale in total offering 361º Kids products comprised 5,155 stores and 1,745 stores respectively, a net closure of 10 core brand’s retail stores and a net increase of 42 Kids products stores compared to the end of December 2020. 2) Carried out numerous live streaming shows with specific themes and rich content on well-known domestic live streaming platforms such as Tmall, Kuaishou, Tiktok, Bilibili and Alipay Sports, to respond the upsurge in delivery of goods during live streaming in the market. Launched the proprietary WeChat mini program “You Yan You Du” to enable a round-the-clock online consumption experience which can be dubbed “Thousands of Stores with Thousands of Images” at WeChat Mall, and tap the traffic of viewers in a vertical of online community.

Strong momentum in Lower-Tier Retail Market

Geographically, approximately 76.26% of the stores were located in third- and lower-tier cities in China, while 23.7% were located respectively in first-and second-tier cities in the country. Geographically, approximately 70.77% of the POS offering 361 Degrees Kids products were located in third-tier and lower-tier cities in China. Over the past years, the growth of China’s retail market is especially contributed by the lower-tier retail market, whose market size has grown from RMB9.9 trillion in 2015 to RMB15.1 trillion in 2020, representing a CAGR of 8.8% (overall retail market increasing by a CAGR of 8.6%). Meanwhile, benefiting from a large population, rising income level, as well as favorable policy trends, China’s lower-tier retail market has increasingly contributed to the overall retail market with huge growth potential.

According to the Frost & Sullivan Report, the permanent resident population in China’s lower-tier market reached 1.23 billion by the end of 2020, accounting for over 87% of China’s total population. With the continued improvement in living standards and support from local governments, the GDP of China’s lower-tier market has grown from RMB53.0 trillion in 2015 to RMB78.8 trillion in 2020, which accounted for 77.6% of China’s total GDP in 2020, and is expected to further increase to RMB109.9 trillion by 2025. The annual per capita disposable income in China’s lower-tier market is expected to grow at a CAGR of 7.2% from approximately RMB29,000 in 2020 to approximately RMB40,000 in 2025, higher than the growth of 6.3% in the tier-one and -two market. The increasing household income level is expected to lead to stronger consumer spending power in the lower-tier market. The market size of China’s lower-tier retail market is also expected to increase from RMB15.1 trillion in 2020 to RMB20.6 trillion in 2025.

Positioning “professional sporting goods” and “fashionable sporting goods”, 361 Degrees concentrated its resources on the development of three core types of sporting goods, namely basketball, running, and comprehensive training. In addition, signed a contract with international basketball superstar Aaron GORDON (the latest signed Spencer Dinwiddie of the NBA Washington Wizards), sponsored marathon events and elite runners and gave its support to various national and professional sports teams, signed a contract with well-known young China actor GONG Jun as the global endorser to attracts more young fans for the brand, and launch a number of co-branded products such as The Three-Body Problem, Minions, Captain Tsubasa, Saint Seiya and Initial D. Those would help 361 Degrees to compete with domestic and foreign top sports brands.

Company valuation

The senior unsecured US Dollar Notes were fully redeemed by 361 Degrees at the maturity date on June 2021 and it is expected that the financial cost should be largely reduced. In addition, since the company mainly adopts a distributorship business model, in which the quarterly trade fairs are highly correlated with the company's sales and is about 6 months ahead of the company's financial statements. As relatively strong 2H21 sales, we expect full-year revenue in 2021 and 2022 to maintain at least double-digit growth. Following the financial performance back to the normal level in the situation before the pandemic happened in early 2020, it is expected that the Company to resume dividends in 2022 and 2023. We expect 2021-2022 EPS to be RMB0.28 and RMB0.32 respectively. Our TP is HKD5.29, represents 16.0x and 13.9x 2021 and 2022 (the industry average is about 19.0x). Our investment rating is “Buy”.

Risk factors

1) Weak domestic growth and consumer spending (including online & lower-tier cities) in sportsware; 2) Intensified competition in the industry; and 3) Slower-than-expected revenue growth.

Financial

Click Here for PDF format...