Positive profit alert with 2021 earnings up by no less than 70%

Xtep announced a positive profit alert, and is expected to record a significant increase of not less than 70% in its consolidated profit attributable to ordinary equity holders for the year 2021 as compared to that for the year 2020.

In addition, Xtep also announced the operation data of 4Q2021. Xtep's core brand products retail sell-through (including offline and online channels) grew by 20%-25% (mid-teens growth in 3Q2021), retail discount level stayed at 25%-20%, and inventory turnover was about 4 months, which was flat QoQ. The core brand products retail sell-through increased by more than 30% in 2021, which was better than a high single-digit growth in the same period last year. The inventory turnover was about ~4 months, better than ~5 months in 2020. A strong increase in consolidated revenue for the 2021 driven by: (1) an over 30% growth in core Xtep brand's revenue in second half of 2021 due to robust sales orders from distributors following our successful launch of signature functional and lifestyle products and retail channel upgrade during the Year; (2) accelerated revenue growth of the core Xtep brand's e-commerce and kids` businesses given the respective completed restructurings from branding, products to operations. An expansion in the gross profit margin of the core Xtep brand primarily attributable to (1) our continual effort in product innovations and better product offerings; and (2) a lower base of comparison triggered by the one-off inventory buy-back in 1H2020.

RSV improvement in 4Q21 continued in Jan 2022

Management mentioned an accelerated growth in FY2021E, which was a result of core brand channel upgrades, ramp up of 9th generation stores, focus on retail experience & launch brand story, which increasing the associated purchase rate and sales per unit area. Xtep's ASP continued to rise as product and brand upgrades, including the launch of professional running shoes such as 160X and 260X series, and premium XDNA apparel such as the cross-over with Shaolin. In addition, kids/online grew faster after the completion of restructuring.

Management also mentioned that Product sold-out rate remained robust, with 1Q2021 and 2Q2021's >80%, 3Q2021's close to 80% and 4Q2021's close to 60%. The RSV growth momentum remained from Jan to date, discount & channel inventory remained at a healthy level.

Management noted that this strong growth momentum should have continued into 2022 year-to-date, as the 1Q-3Q22 procurement orders from distributors witnessed ~30% YoY growth. Management expects the core brand topline growth will be >30% in 1H22 and >25% for 2022 as the base is relatively high in 2021H2. Revenue growth for athleisure brands (K-Swiss, Palladium) and professional sports brands (Saucony, Merrell) to reach at least 30% and 50% respectively, in 2022.

Company valuation

Xtep's five-year plan (2021-2025) targets to deliver a CAGR of 23% in core brand sales to Rmb20bn in 2025. The new brand will grow at a CAGR of 30%, and the goal is to reach CNY 4 billion in 2025. Management is confident that core Xtep brand five-year sales growth target being on track, driven by: (1) running shoes sales remained very promising after expanding the premium running shoes products; (2) fast-growing Xtep kids robust sales trend of up >40% in 2021, recent trade fair continued the strong momentum > 50%; (3) new brands acquired in 2019 help expansion, and increase investment in private traffic online sales as well as continue to expand sales in an omni-channel model. We expect the growth of Xtep to be higher than that of its peers, mainly due to its smaller base compared to other peer brands, and also see that the company's effectiveness in product upgrades, channel upgrades, brand upgrades and management upgrades.

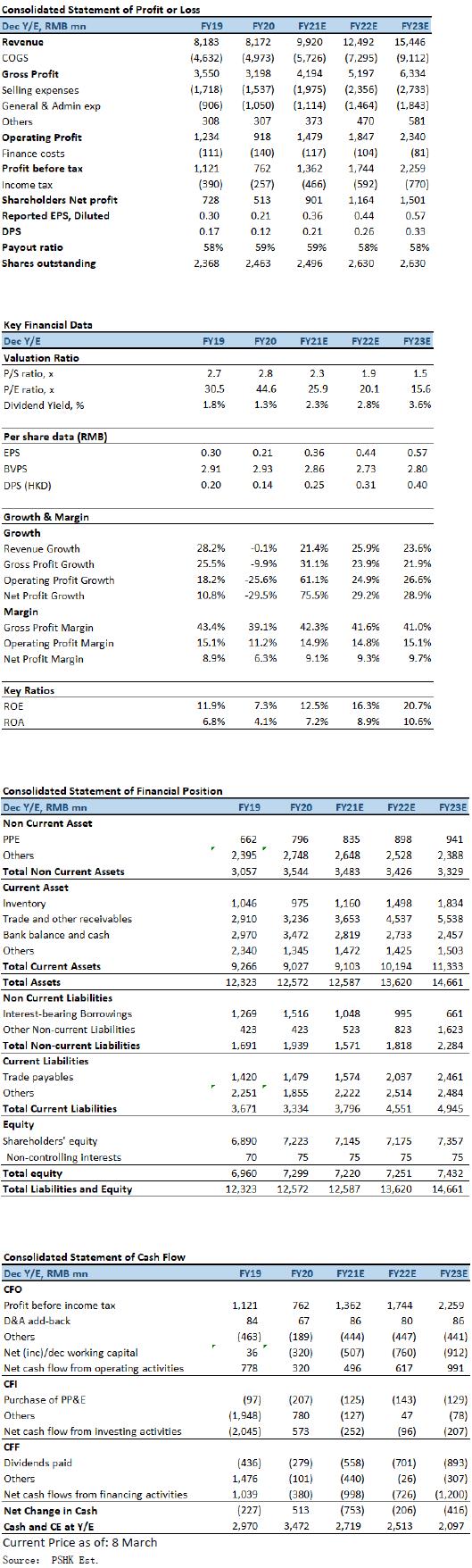

We expect 2022 estimated EPS to be RMB0.44 and our TP at HKD14.15, represents of 26.0x forward P/E (estimate is more conservative than our last report in Sep. 2021). The valuation of Xtep at <1.x PEG, but already reflect a lot of positive factors to a certain extent. Thus, our investment rating maintain “Buy”.

Risk factors

1) Weak domestic growth and consumer spending in sportsware; 2) Intensified competition in the industry; and 3) Slower-than-expected in new brands development.

Financial

Click Here for PDF format...