Investment highlights

Tan Jai International, which has been in business for more than 24 years, is the representative brand of Asian noodle specialty stores. Its has two brands called “TamJai” and “SamGor” which account for 64.4% market share of in Hong Kong (calculated based on 2020 revenue). In 2018, the company was acquired by Toridoll (Toridoll Japan, Tokyo Stock Exchange listed company: 3397), a well-known multi-brand restaurant group operating the world's largest udon chain " Marugame". Currently, the business has expanded to mainland China and Singapore.

Expand restaurant network to consolidate its market position

Up to now, the company had 157 restaurants, an increase of 46.7% compared with April 1, 2018. There are 150 restaurants in Hong Kong strategically located in various business areas, such as business districts, shopping districts, commercial streets and residential districts to reach customers of different classes and expand their client base. Of the other 7 restaurants, 4 are located in mainland China and 3 are located in Singapore. The company plans to open approximately 44, 74, 24, 25 and 15 new restaurants in Hong Kong, China, Singapore, Japan and Australia respectively by March 31, 2024 and consolidate its market position by expanding its restaurant network in existing markets.

Adjusted profit will increase more than doubles in the first half of FY2022

Looking back at the interim period ended at September 2021, due to the increase in the number of operating restaurants and the substantial gain in comparable restaurant revenue, revenue rebounded sharply by 43% YoY to HKD 1.182 billion. During the period, although the profit fell by 11.8% to 138 million, after deducting one-off items such as government subsidies and listing expenses, the adjusted profit rose 1.08 times YoY to 147 million. Basic EPS for the half year were 13.8 cents compared to 15.6 cents for the same period last year. The company's smart scheduling has improved the cost-effectiveness of staff arrangements and improved manpower efficiency. The proportion of restaurant staff costs to revenue has been reduced to 24.1%, compared to 25.7% in the same period last year.

Benefit from the integration of central kitchens and proper cost control

The operating profit margin of Tan Jai International increased from 18.7% in 1HFY21 to 25.7% in 1HFY22, thanks to: i) a reduction in the cost share caused by bulk purchases; ii) Increase in average daily revenue per restaurant and reduction due to central kitchen integration which led to the reduction in asset depreciation, rental and related expenses resulted from the reduction. After deducting other one-time items, the adjusted profit margin increased from 8.6% to 12.4%.

Company valuation

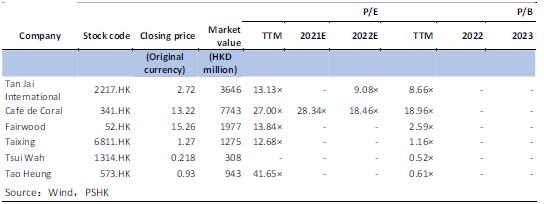

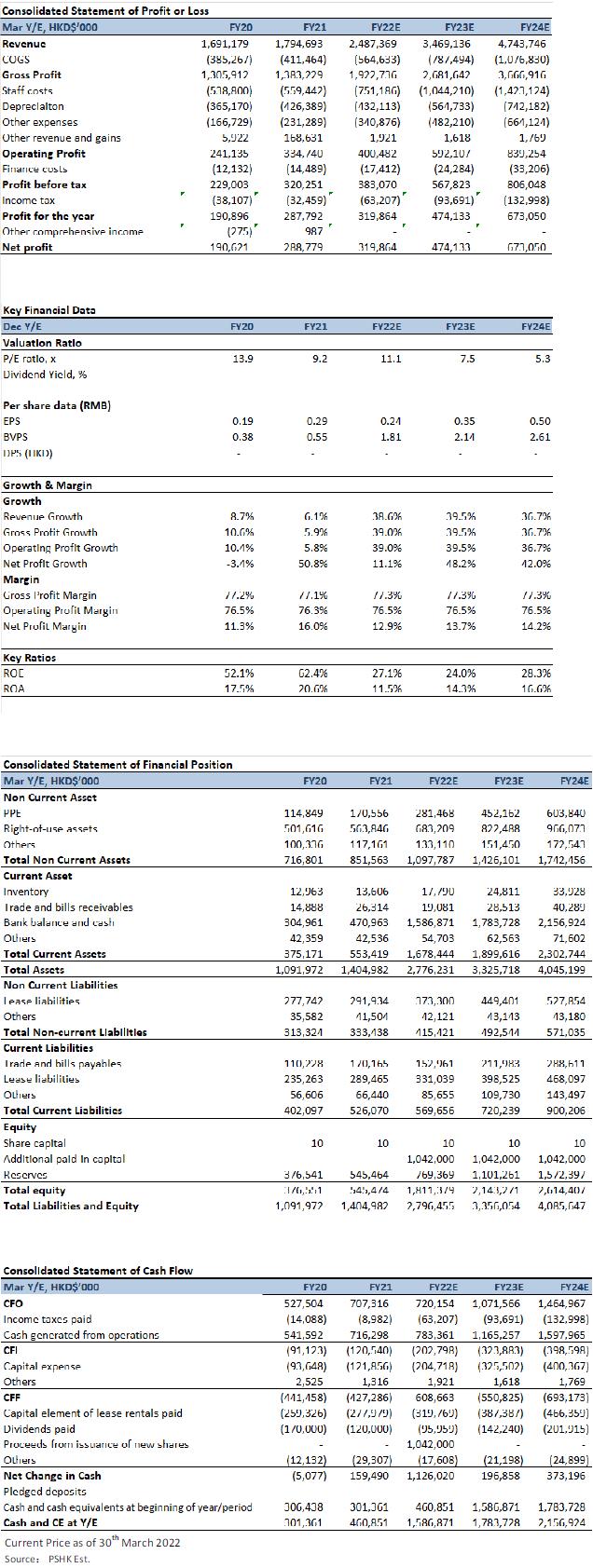

We predicted that Tan Jai International's total revenue will be 2.49 billion, 3.47 billion and 4.74 billion in 2022-2024, respectively. The revenue growth will mainly benefit from: 1) the expansion of restaurant network; 2) the increase in the average number of bowls sold per seat per day; 3) the per capita customer consumption rises. The company's EPS in 2022/2023/2024 are expected to be $0.24/0.35/0.50, and the target price is HK$4.77. Corresponding to 20x/13.5x/9.5x P/E ratio of 2022/2023/2024 (the historical average P/E ratio of the industry is about 22 times), the Company is given a “Buy” rating.

Risk factors

The epidemic has resurged and the expansion of the restaurant network has been less than expected.

Company introduction

The company has been in business for over 24 years and has a network of over 100 restaurants, becoming the representative brand of Asian noodle shops. The two brands under Tan Jai International are " Tan Jai " and " SamGor ". In 1996, the first restaurant under the brand name " Tan Jai " was opened in Hong Kong. Subsequently, the first restaurant under the " SamGor " brand was opened in Hong Kong in 2008. Both brands are rapidly expanding in Hong Kong, operating together over 100 restaurants in Hong Kong in 2017. In January 2018, Tan Jai Group was acquired by Toridoll (Toridoll Japan, Tokyo Stock Exchange listed company: 3397), a well-known multi-brand restaurant group operating the world's largest udon chain " Marugame". At present, the company's business has expanded to mainland China and Singapore, and will open the first restaurant under the " SamGor " brand in Singapore in 2020, and the first restaurant under the " Tan Jai " brand in mainland China in 2021. As of the end of September 2021, the company's restaurant network of 157 restaurant is all over Hong Kong, Mainland China and Singapore.

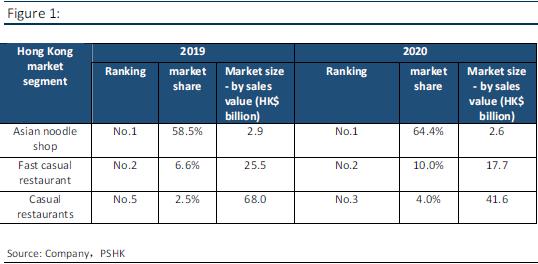

As a chain restaurant operator specializing in rice noodles, Tan Jai International has a leading position in the Asian noodle specialty store market in Hong Kong, with a market share of 64.4% (in 2020 revenue). The casual restaurant market and fast-casual restaurant market in Hong Kong are also firmly in the top position, with a significant increase in market share in all segments in 2020 which has strong competitiveness.

Industry analysis

The four sub-categories of the consumer food service industry in Hong Kong: casual restaurants, fast food restaurants, fine dining restaurants and other restaurants which accounted for 53.0%, 23.6%, 19.7% and 3.7% of the total industry revenue respectively in 2020. Among them, casual restaurants with the largest proportion are characterized by flexible service hours, diversified gourmet products and relatively affordable prices to attract a large quantity of clients.

Casual restaurants can be further subdivided into fast-casual restaurants and fine-casual restaurants. In 2020, the ratio of fast-casual restaurants and fine-casual restaurants will be approximately 4:6. Although fast-casual restaurants have a smaller proportion, their CAGR during 2016 to 2019 was 3.3% which was higher than that of fine-casual restaurants of –0.3% during the same period. We expect that driven by the convenience, good value for money and flexible operating model, fast-casual restaurants will lead industry recovery and drive the growth of the overall casual restaurant segment at a faster rate than other consumer food service categories, The CAGR of fast casual restaurants during 2020 to 2025 will be 11.8% compared to 10.1% for the overall consumer food service industry.

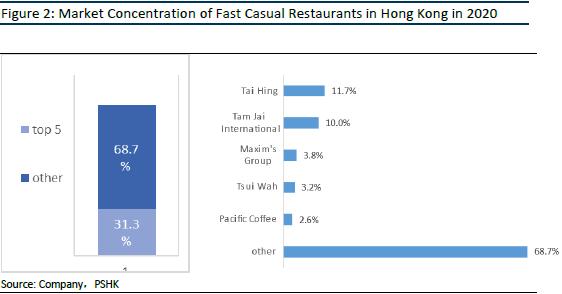

Casual restaurants category is highly competitive and has a low concentration with a CR5 of 23.3% in 2020. However, the competition pattern of fast-casual restaurants as a sub-category is relatively concentrated with 31.3% CR5 in 2020. The four leading companies have a huge restaurant network with more than 117 restaurants and the majority restaurants are Chinese restaurants which shows the importance of convenience and strategic location to Hong Kong consumers. The Asian noodle specialty store segment to which Tan Jai Group belongs is more highly integrated, with a CR5 of 92.1% in 2020 and Tan Jai accounts for more than 60% of the market share, ranking first in terms of market revenue and number of restaurants.

Fast-casual restaurants can flexibly cater to trends in ordering food from online platforms

The busy and fast pace of life of Hong Kong people and the outbreak of the epidemic have promoted the online and offline development of fast casual restaurants. Hong Kong people have always been known for their long working hours and busy lives. According to the Quarterly Report on General Household Survey released by the Census and Statistics Department, the median weekly working hours of Hong Kong employees in 2021 was 44 hours. Due to the long working hours, office workers and families generally prefer fast-casual restaurants with fast serving times and high checkout efficiency. At the same time, due to the impact of the epidemic, consumers are increasingly ordering food through home delivery and self-pickup platforms. From 2019 to 2020, the proportion of food takeaway and takeaway in the consumer food service industry in Hong Kong increased from 14.1% to 42.1%. The flexible operating model of fast-casual restaurants is catering to this trend, resulting in rapid growth.

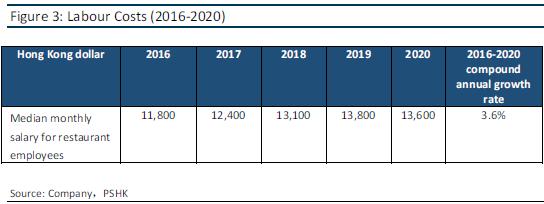

Rent and labor costs are key components of a restaurant's operating costs. Rental costs in Hong Kong are high which generally account for more than 30% of the total operating costs of restaurants in Hong Kong. Labor costs also increased during 2016 and 2020, with a median monthly salary of restaurant employees increasing at a CAGR of 3.6% to reach HK$13,600 in 2020. The profitability of many restaurant operators has been affected as a result. Nonetheless, larger chain restaurants have simplified food processing to reduce labor costs through economies of scale and adopted centralized purchasing policies to reduce unit costs of ingredients.

Chain restaurants make up a large proportion of restaurants in Hong Kong. In 2020, the total revenue of chain restaurants was 37.3 billion which account for 47.5% of the market share, while the sales revenue of independent restaurants was 41.2 billion which account for 52.5% of the market share. Although the overall market share of chain restaurants is still lower than that of independent restaurants, the CAGR during the period from 2016 to 2019 is higher than that of independent restaurants. From 2020 and 2025, revenue of independent restaurants are expected to record a CAGR of 11.3% to 70.5 billion, while chain restaurants are expected to record a CAGR of 8.6% to 56.2 billion during the same period.

Business Situation

The Company's extensive restaurant network helps to increase market share and promote business growth

As of the end of September 2021, the company had 157 restaurants, an increase of 46.7% compared with April 1, 2018. Among them, the number of restaurants in Hong Kong has increased to 150 and four new restaurants were opened in Shenzhen and three restaurants continued to operate in Singapore. The company plans to open 14 new restaurants in Hong Kong from October 2021 to March 2022, with several additional restaurants in the Greater Bay Area and Singapore during this period. In Japan, with the support of the company's controlling shareholder Toridoll Japan, two new restaurants are expected to open in the first quarter of 2022.

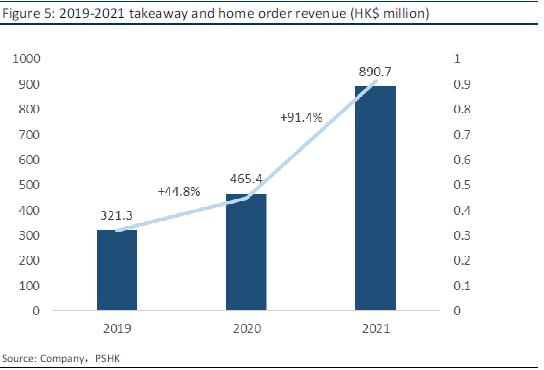

Although consumers` dining habits have changed due to the outbreak of the epidemic and the increasing popularity of online home-to-home services, the proportion of the revenue company's dine-in order to takeaway self-pickup and home order has dropped from 8:2 in 2019 to 2021. 5:5. However, dine-in orders will not be completely replaced by take-out and home-delivery orders, and online-to-home services generally only cover the customers in surrounding areas. Having a broad restaurant network can help the company grasp the demand for home-delivered orders and further promote business growth.

Highly standardized business model supports the company to rapidly and systematically expand to other new markets

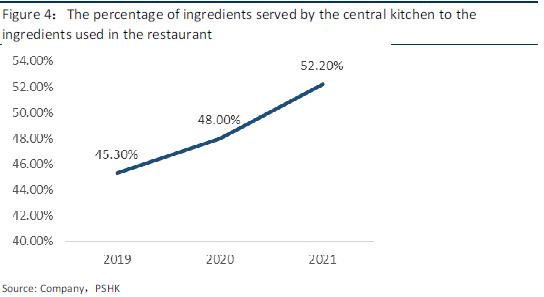

The company currently operates 2 central kitchens. One is in Hong Kong and the other is in Singapore. Central kitchens help ensure consistency of food taste and quality across restaurants, simplify food handling procedures at restaurant level and make food easier to be standardized. Not only that, central kitchen can save the installation of unnecessary cooking equipment in the restaurant, effectively reduce the capital expenditure of opening a new restaurant, thereby improving the scalability of the business. The company plans to set up central kitchens in Mainland China, Singapore and Australia and will process more new products in the central kitchens, including ingredients, snacks, soup bases and sauces.

�In addition, the company adopts a central procurement policy and has jointly developed a variety of different cooking equipment with cooking equipment suppliers, such as automatic rice noodle cooking machines and soup pots, to help kitchen staff more accurately control the cooking time or the amount of ingredients, effectively

unifying the taste and quality of restaurant food, reducing the manpower required to handle food and the risk of work-related injuries due to repetitive actions. As a result, restaurants do not need to hire skilled chefs and can more easily recruit suitable kitchen staff. On the other hand, the company has established comprehensive standardized procedures for opening, operating and managing restaurants to enhance operational and management efficiency and ensure consistent service quality. Standardized procedures include, but are not limited to, customer service, cleaning and disinfection, staff training and quality control.

Outperformed other major restaurant chains during the epidemic

As frontline employees are generally hired on an hourly rate based on flexible working schedules, the company can quickly respond to any epidemic prevention policies that restrict business hours and minimize staff costs. The restaurant also maintains a minimum amount of ingredients for up to three days to avoid waste and minimize the cost of ingredients. However, the main factor behind the company's ability to maintain stable earnings during this turbulent period is that the company's food products are very suitable for take-out and home delivery. Since the company's food only requires simple and quick procedures to prepare and cook, the restaurant can quickly fulfill take-out and home orders during busy hours and achieve higher sales. In fact, the company's revenue in 2021 has increased by 6.1%, which is better than the performance of the top five listed restaurant chains in Hong Kong. The top five listed restaurant chains in Hong Kong all saw their revenue drop by 14.0% to 47.8% over the same period. We believe that even if the COVID-19 situation improves and consumers resume dine-in dining in restaurants, online ordering and home delivery will still be the mainstream trend.

Looking back at the interim period ended September 2021, benefiting from the increase in the number of operating restaurants and the substantial increase in comparable restaurant revenue, revenue rebounded sharply by 43% YoY, increasing to 1.182 billion. During the period, although the profit fell by 11.8% to 138 million, after deducting one-off items such as government subsidies and listing expenses, the adjusted profit rose 1.08 times YoY to 147 million. Basic EPS for the half year were 13.8 cents compared to 15.6 cents for the same period last year. By improving

the cost-effectiveness of staff arrangements and improving manpower efficiency, restaurant staff costs as a percentage of revenue decreased to 24.1%, compared to 25.7% in the same period of the previous year.

The operating profit margin Tan Jai International's has increased from 18.7% in 1HFY21 to 25.7% in 1HFY22, thanks to: i) bulk purchasing leads to a reduction in the proportion of cost; ii) the increase in average daily revenue per restaurant and the reduction caused by the integration of the central kitchen reduced the proportion of asset depreciation, rental and related expenses. After deducting other one-time items, the adjusted profit margin will increase from 8.6% to 12.4%.�

Revenue Forecasts and Risk Factors

Revenue analysis

We predict that the total revenue Tan Jai International will reach 2.49 billion, 3.47 billion, and 4.74 billion in 2022-2024, respectively. The revenue growth will mainly benefit from: 1) the expansion of restaurant network; 2) the increase in the number of bowls sold per seat per day; 3) rise in per capita customer consumption. In the future, the company will continue to expand its existing restaurant network and expand into overseas markets and plans to increase the number of restaurants in operation to more than 300 by the end of fiscal year 2024. We believe that the number of company's operating restaurants in Hong Kong have little room for growth. It is expected to be similar to the more than 160 restaurants of another Hong Kong-listed restaurant chain, the Café de Coral Group. However, the Hong Kong business will continue to be the company's main source of revenue. Entering overseas markets can also bring new opportunities for the company. Last year, the local epidemic was still resurged, but the daily average number of bowls sold per seat in the restaurant has gradually recovered to the pre-epidemic level. Although the epidemic situation in Hong Kong has worsened recently, we believe that the company can respond flexibly to provide takeaway and home services to reduce the impact of epidemic prevention restrictions on restaurants. It is expected that the per capita consumption of customers still has room for improvement, mainly because the company has launched new products and high-end ingredients and sold additional snacks and beverages with high gross profit.

Company Valuation

We forecast that the company's EPS in 2022/2023/2024 to be HK$0.24/0.35/0.50, with a target price of HK$4.77, corresponding to 20x/13.5x/9.5x EPS in 2022/2023/2024 (the historical average P/E ratio of the industry is 22x). The Company is given a “Buy” rating (initial coverage).

Risk factors

The epidemic has resurged and the expansion of the restaurant network has been less than expected.

Financial data

Click Here for PDF format...