Investment Summary

The Loss Is Turned into a Profit in H2, and the Annual Loss Is Significantly Narrowed

Cathay Pacific recently reported its results. In 2021, it recorded a net loss attributable to shareholders of HK$5.53 billion, equivalent to a loss of approximately HK$0.951 per share. The loss decreased by 74.5% from the same period, compared with a loss of HK$21.65 billion in previous years. The Company reported a loss of HK$7,565 million in H1 and a profit of HK$2,038 million in H2, while the losses in H1 and H2 of 2020 were HK$9,867 million and HK$11,783 million, respectively. In H2, driven by the strong freight business, the Company successfully turned its loss into a profit, and reported a positive operating cash flow. As there is still a preferred stock dividend in arrears, no dividends will continue to be paid. As at the end of 2021, the total size of the fleet was 234 aircraft, which remained basically stable, of which 40 were freight aircraft, including six 777-300ER freight aircraft that were changed from passenger aircraft.

Fare Climb Does Not Make up for the Loss of Passenger Business Suspension, and the Results Are Supported by the Freight Business

In 2021, the Company's passenger service revenue and freight service revenue fell to HK$4,357 million and increased to HK$35,814 million, a year-on-year decrease of 63.5% and a year-on-year increase of 28.4%, respectively. The freight revenue accounted for nearly 90% of the total.

During the reporting period, the passenger yield increased by 87.4% year-on-year to a high level of HK$1.055. In general, the total passenger revenue still recorded a year-on-year decrease, equivalent to 5.9% in 2019. It was mainly due to the repeated suspension of passenger flights under the circuit breaker policy amid the severe pandemic. The Company's available passenger capacity fell sharply by 61.8% year-on-year (only equivalent to 8% in 2019). Due to the sharp decline in the load factor by 26.9 ppts to 31.1%, the fare climb did not compensate for such adverse effect.

The freight business was on the contrary. Benefited from an increase in the load factor (+8.1 ppts) and a rise in freight (+33.1%), the freight revenue still reported a year-on-year increase of 28.4% even though the available freight capacity decreased by 10.9%. The unit freight revenue per ATK rose to HK$3.21, a strong year-on-year increase of 48%.

Significant Decrease in Costs: Non-oil Costs Fall by 24%, and Fuel Hedging Records Profit

Benefiting from the sharp decrease in corporate restructuring costs and aircraft impairments, Cathay Pacific's impairment and related expenses fell back to HK$832 million in 2021 from HK$4,056 million in 2020. During the special period, the Company increased its efforts to control costs. The effect of throttling measures including the special vacation plan was remarkable. The non-oil costs were significantly reduced by HK$37,708 million or 24.4% year-on-year.

In terms of fuel, the fuel costs excluding fuel hedging increased by HK$1 billion or 12% year-on-year due to the increase in oil prices. However, including HK$2,336 million of profit recorded by fuel hedging (compared to a loss of HK$3,017 million in the same period), the net fuel costs fell by HK$4.25 billion or 38.2% year-on-year. International oil prices continued to climb higher from 2022 onwards. The Company is expected to continue to record fuel hedging profit in the first quarter.

Investment thesis

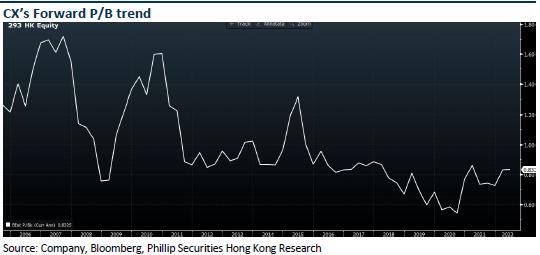

Due to the escalation of the Omicron variant, the Hong Kong government tightened the travel and operation restrictions at the beginning of the year, and tightened the quarantine arrangements for crew members. Cathay Pacific's operating data for the first two months of 2022 bottomed out again. However, after mid-March, driven by the continuous decline in new confirmed cases and the gradual easing of the pandemic, the Hong Kong government said that it would suspend the compulsory testing for the whole people, and announced the cancellation of the ban on flights from nine countries, including the United Kingdom and the United States, from April 1. The Company's results were greatly affected by the pandemic control. Once the control is over, the rebound under the recovery of demand will also be large. At present, the corresponding price-to-book ratio of the stock price is less than 0.7 times, which is the lowest point in the past 20 years.

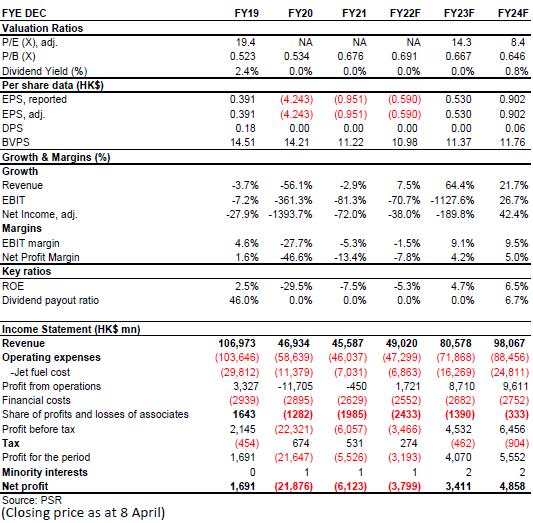

Based on the revised financial forecast, we lift target price to HK$9 for the Company, equivalent to 2022/2023/2024E 0.82/0.79/0.77 x P/B, reaffirming the accumulate rating. (Closing price as at 8 April)

Risk

Surging oil price

RMB depreciation

Demand affected by economy

Transformation program failed

Financials

Click Here for PDF format...