|

JLMAG(6680)

Analysis:

JL MAG RARE-EARTH (6680) is a producer of high-performance rare earth permanent magnets (REPMs). It ranks first in the world by high-performance REPM production volume. Since its establishment, it has focused on the R&D, production and sales of high-performance NdFeB rare earth permanent magnets (NdFeB PMs) used globally in the fields of new energy, energy conservation and environmental protection. Its products have a wide array of applications in new energy vehicles and automotive parts, permanent magnetic wind turbine generators, energy-saving variable-frequency airconditioners and other sectors. The Group has adequate orders in hand and the production capacity is fully utilized. With the completion, acceptance and operation of the “High-Performance REPM Base Project”, with an annual production capacity of 8,000 tonnes invested and constructed by the Group in Baotou, the annual production capacity of its high-performance REPM blanks has reached 23,000 tonnes. The production base has also transformed from a single factory to a group of factories in multiple locations. The Board of Directors has also adopted relevant plans to gradually increase the annual production capacity of the Company`s high-performance REPM blanks to 40,000 tonnes by 2025. (I do not hold the above stock)

Strategy:

Buy-in Price: $21.50, Target Price: $23.50, Cut Loss Price: $20.50

|

CHINA XLX FERT(1866)

Analysis:

China XLX Fertilizer is the 6th largest fertilizer company in China and the 1st largest fertilizer company in Henan that uses coal as raw material. As of 2020, the company's major product production capacity is 2.6 million tons of urea, 2.35 million tons of compound fertilizer, 600,000 tons of methanol, and 50,000 tons of furfuryl alcohol. The company's third production base in Jiujiang City, Jiangxi Province was put into operation in February 2021, and the second and third plant fixed bed renovation and upgrading projects in Xinxiang, Henan Province were put into operation in the fourth quarter of 2021, improving production capacity and efficiency, further consolidating the company's leading position in the fertilizer and chemicals industry. In 2021, the company's operating income will be approximately RMB 16.815 billion, a year-on-year increase of 61%; the net profit attributable to the parent company will be approximately RMB 1.294 billion, a year-on-year increase of 272%. Due to the domestic epidemic, the international situation, and the surge in upstream prices of crude oil and natural gas, the price of urea will remain high in 2022.

Strategy:

Buy-in Price: $6.23, Target Price: $9.10, Cut Loss Price: $4.50

|

|

CR Pharmaceutical (3320.HK) - Promote digital transformation and M&A cooperation to create competitive advantage through innovation and differentiation

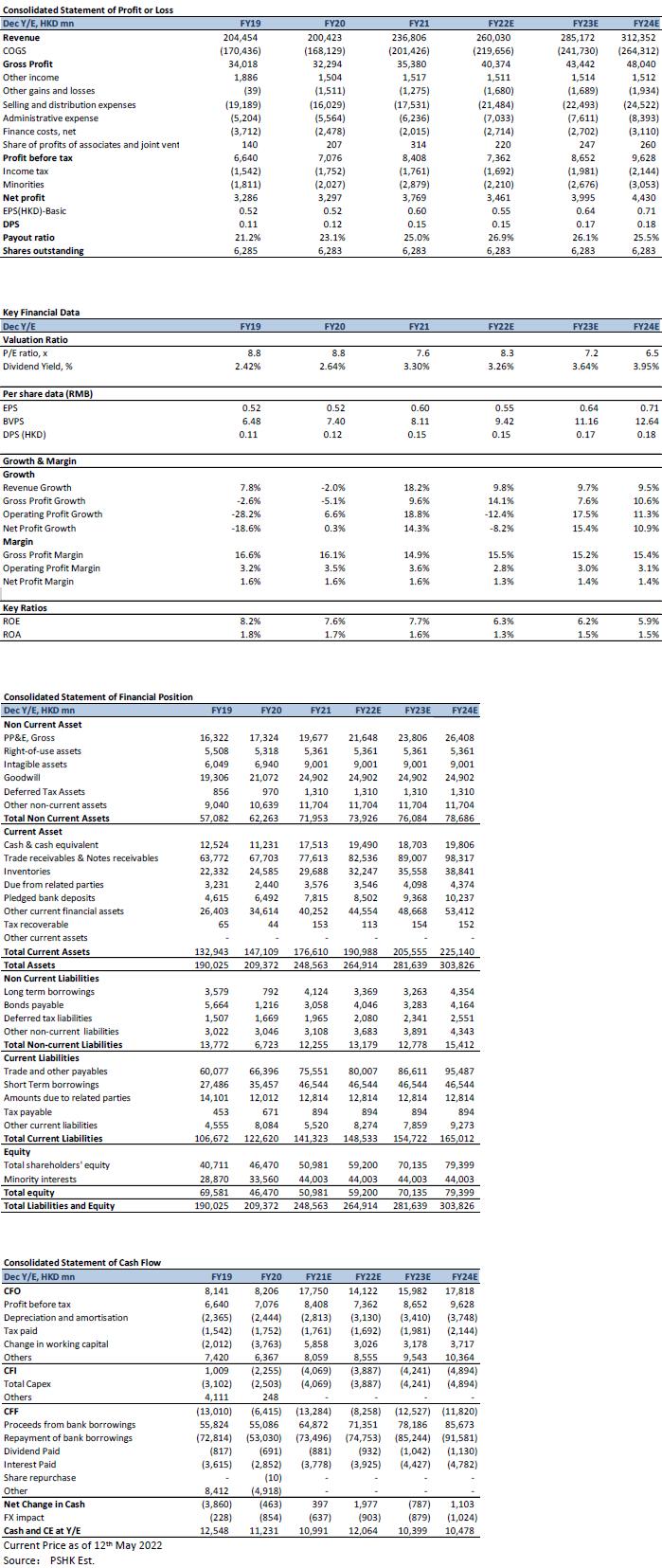

Investment highlightsCR Pharmaceutical is a leading integrated pharmaceutical company in China specializing in the pharmaceutical, distribution and retail of medicines. Its product portfolio includes chemical drugs, traditional Chinese medicines, biological drugs, and nutraceutical products. Its product coverage contains cardiovascular system, respiratory system, anti-tumor, central nervous system, immune system, genitourinary system, blood, digestive tract and metabolism, anti-infection, traditional Chinese medicine, etc. CR Pharmaceutical announced its 2021 annual results that the company achieved total revenue of HK$236.806 billion, with a YoY increase of 18.2%. The increase was mainly due to the relief of the epidemic and the recovery in performance. In particular, the pharmaceutical distribution business accounted for the largest contribution to revenue growth. The overall net profit reached HK$6.647 billion, with a YoY increase of 24.9%; The net profit attributable to owners of the parent company was HK$3.769 billion, with a YoY increase of 14.3%. Actively expand external mergers and acquisitions and innovative cooperation, and digitalization helps business development Revenue from the pharmaceutical business was HK$38.61 billion, with a YoY increase of 19.9%. The revenue of the CHC segment, the prescription drug segment and the biopharmaceutical segment all achieved growth, mainly due to the impact of the mitigation of the epidemic and driven by external mergers and acquisitions. The gross profit margin of pharmaceuticals in 2021 was 57.6%, with decrease of 2.9% compared with same period of last year mainly due to factors such as volume-based procurement and product structure, etc. From the perspective of product categories, chemical medicine and traditional Chinese medicine contributed a larger proportion of the income, accounting for 41.6% and 49.4% respectively. The company continues to lay out a high-growth track, incubate new industrialization opportunities, continuously optimize its business structure and enhance its core competitiveness. Accelerate the steady and professional development of the equipment distribution business and promote innovative value-added services through digital transformation. Revenue from distribution business was HK$199.13 billion with a YoY increase of 17.9%. Its gross profit was HK$12.36 billion and the margin was 6.2% with a YoY decrease of 0.9% mainly resulted from the ease of epidemic and the income from the export of epidemic prevention materials with high gross profit margins has decreased. The company's medical terminal coverage continues to improve and it strives to build an efficient and safe pharmaceutical integrated logistics network to continuously enhances its core competitive advantages. The company continues to vigorously promote the professional development of medical device distribution business, build national professional platform and professional service company and enhance innovative service capabilities. At the same time, the digital transformation process was promoted and the service platform “CR Micro Medicine”, a vertical operation service system of precision medicine for special diseases/rare diseases, was established. The transaction volume of the B2B online platform "CR Pharma e-Store" has grown steadily, covering a wide range of 28 provinces across the country. Deploy a "Dual Channel" qualified professional pharmacies to ensure a high-quality digital operation platform Retail business revenue was HK$7.61 billion with a YoY increase of 17.6% which was mainly due to the rapid growth of direct-to patient (DTP) business revenue. Its gross profit was HK$696 million with a gross profit margin of 9.2% with a YoY decrease of 1.1%, which was mainly due to the proportion of revenue from DTP business with lower gross profit margin increased. DTP business revenue was RMB 4.32 billion which accounted for 68.4% of the retail segment revenue with a YoY increase of 12.7%. The company actively deploys professional "Dual-Channel" qualified pharmacies such as DTP, creates a high-quality, integrated retail pharmacy operation platform and promotes an online and offline integrated digital retail 2C platform. Company Valuation and investment adviceCompared with the leading companies in the domestic pharmaceutical industry including Sinopharm Group Co. Ltd, Shanghai Pharmaceuticals Holding Co., Ltd. and Fosun Pharmaceutical Co., Ltd., the current PE ratio of CR Pharmaceutical is only about 7.6x which is lower than the industry average of 9.0x; We forecast that the company's EPS during 2022-2024 to be HK$0.55, HK$0.64, and HK$0.71 respectively and give a target price of HK$4.95. The corresponding PE ratio were to 9.0 x, 7.7 x, and 7.0x during 2022-2024 and the Company is given a “Accumulate” rating.

Risk factorsUncertainty brought about by epidemic resurgence, diversity of volume-based procurement policies have brought challenges to enterprises and the effect of external cooperation was below expectation. Financial data

Click Here for PDF format...

| Recommendation on 26-5-2022 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 4.550 | | Suggested purchase price | N/A | | Target Price | $ 4.950 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2022 Phillip Securities (HK) Ltd. All Rights Reserved.

|