2021 results beat consensus

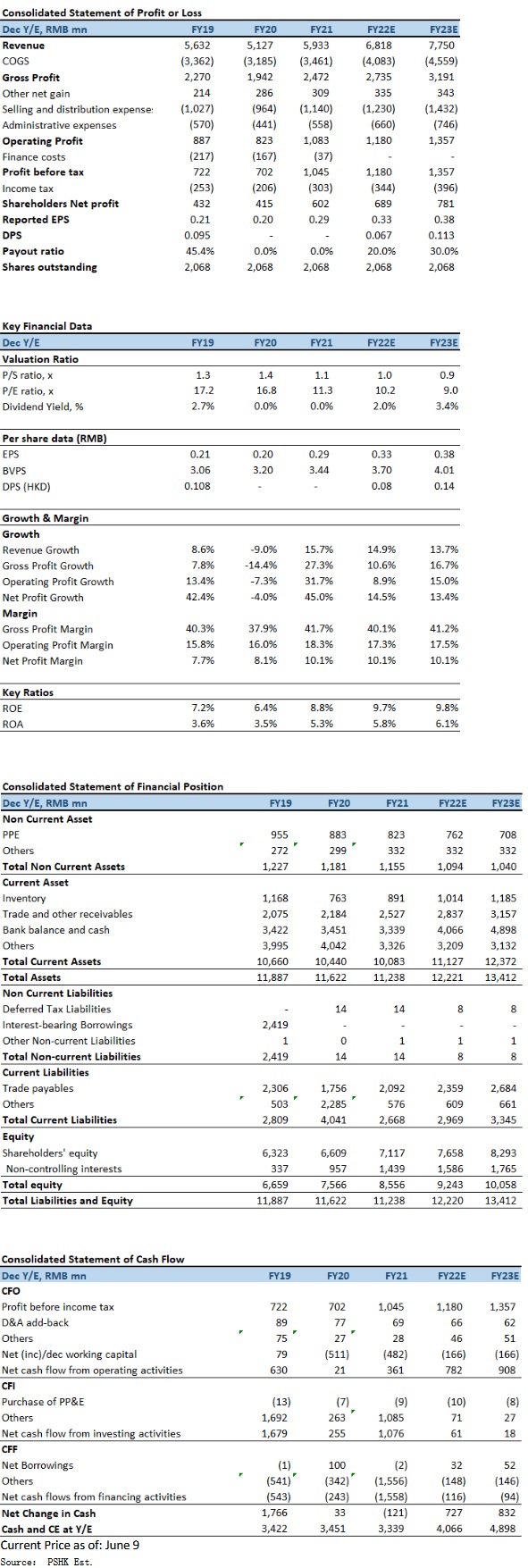

During 2021FY, 361 Degrees International Limited (361 Degrees) recorded a revenue of RMB5,933.5mn (2020: RMB5,127mn), increasing 15.7% YoY, slightly below our estimates of RMB6,040mn but roughly in line with consensus estimates RMB5,922mn. Profit attributable to the equity shareholders of the Company was RMB601.7 million, increase of 45% and 39.2% by compared with 2020 and 2019 respectively, above our and consensus estimates of RMB507.4mn and RMB549.0mn respectively. Net margin was up by 2ppt YoY to 10.1%.

The revenue of footwear products and clothing products were RMB2,532mn (accounting for 42.7% of the overall revenue) and RMB2,147mn (accounting for 36.2% of the overall revenue), an increase of 21.7% and 7.3% YoY. By adjusted the upgrade of product mix by launching a variety of new products with a higher average wholesale price (AWP) and drove the revenue growth from the e-commerce business, the AWP of footwear and apparel products are back to pre-epidemic levels, increased by 4.4% and 2.3% YoY. In addition, the sales volume of footwear and apparel products increased by 16.6% and 4.8% YoY, respectively. This was mainly due to the recovery in the market and continuous brand image enhancement as well as introducing high-quality new products. The sales volume of the accessories edged down by 0.8% YoY but the AWP of the accessories increased by 31.2% YoY which led to a YoY increase of 30.3% in the revenue to RMB69mn from the sales of accessories. Also benefited from the recovery of the market, the revenue from 361 Degrees Kids for the year continued to grow, recording a YoY increase of 18.7% to RMB1,107mn, and accounted for approximately 18.7% of the total revenue during the year. The growth was attributable to a YoY increase of 18.4% in the sale volume of products and a YoY increase of 0.2% in AWP.

Gross profit margin and operational efficiency improved

Cost of sales was increased by 8.7% YoY, in which, the cost of internal production and outsourced products increased by 16.9% and 2.9% YoY, respectively. The increase in cost of internal production was attributable to the increase in raw materials consumed by 19.7% and labour cost by 31.8% YoY. Gross profit of RMB2,472.4mn for the year of 2021, representing an increase of 3.8 percentage points in the gross profit margin to 41.7%. The gross profit margins of footwear, apparel, accessories and 361 Degrees Kids increased by 4.5ppt, 4.7ppt, 10.0ppt and 0.2ppt to 43.1%, 41.4%, 38.4% and 41.2% respectively. The gross profit margin improved, mainly due to an upward adjustment of the AWP charged to distributors back to the normal level in the situation before the pandemic happened in early 2020 in view of the improved market environment in China and the increase in proportion of sales revenue generated from its e-commence platform. In addition, Other factors that contributed to an increase in the profit margin also included the decrease in production cost because of the improved production efficiency and effective cost control over the subcontractors. Overall operational efficiency has also improved, with the average trade and bills receivable cycle was 149 days a 10-day decrease from 2020; the average inventory turnover cycle was decreasing by 24 days to 87 days.

As at 31 December 2021, the 361 Degrees core brand’s retail network comprised 5,270 stores (the latest ninth-generation image stores 1486, accounting for 28.2% of the total number of the Group’s stores), representing a net increase of 105 stores compared to the end of 31 December 2020. although under the uncertain market situation caused by the epidemic, the Company Core Brand’s retail network approximately 77.2% of the stores were in less impact third- and lower-tier cities in China, while 4.6% and 18.2% of which were located respectively in first- and second-tier cities in the country. In 2021, sales from e-commerce platforms amounted to RMB1,227mn, increase 55.1% YoY, and accounted for approximately 21% of the total revenue.

1Q2022 Recorded High Growth in E-commerce

For the 1Q2022, the retail sales (in terms of the retail value) of core branded products recorded high teens growth compared to the same period of 2021. The retail sales (in terms of the retail value) of kids branded products recorded 20-25% growth compared to the same period of 2021. Meanwhile, overall e-commerce products recorded approximately 50% growth compared to the same period of 2021, which accelerated from the 35-40% YoY growth in 4Q2021.

China Total Retail Sales of Consumer Goods in April decrease of 11.1%

In April, the local epidemic had spread widely and frequently, affecting most provinces across mainland China. Residents went out to shop and eat less often, and the sales of non-essential commodities and the catering industry were significantly impacted. According to data released by the National Bureau of Statistics of China, the total retail sales of social consumer goods in April was RMB2,950bn, a YoY decrease of 11.1%, a significant deterioration from the 3.5% decline in March, and a far below market expectations of 6.6% decline. The retail sales of urban consumer goods was RMB2,563.7bn, down 11.3% YoY; the retail sales of rural consumer goods was RMB384.6bn, down 9.8%. During the period, retail sales of goods decreased by 9.7%; among them, clothing, shoes and hats & Knitwear decreased by 22.8% YoY. Due to the negative impact of the epidemic, retail and catering companies continue to develop online businesses and accelerate the development of contactless services such as Internet sales and food delivery. From January to April, the online retail sales of physical goods increase of 5.2%, accounting for 23.8% of the total retail sales of social consumer goods, an increase of 0.6ppts from January to March; in the online retail sales of physical goods, food and use goods increased by 12.9% and 6.3% respectively, but the online retail sales of upgraded commodities such as gold, silver, jewelry and sports & entertainment products maintained rapid double-digit growth.

Company valuation

Since nearly 80% of the company's stores are located in third- and lower-tier cities in China, in addition to being relatively less affected by this round of epidemic, the growth of the domestic retail market is also more prominent than that in first- and second-tier cities. The company's products are positioned at high cost performance, “specialised, youthful and internationalised”, and e-commerce channels increases the coverage of markets, which will help enhance brand competitiveness and drive sales recovery. Management indicated that sales turnover growth in the 2Q2022 could still reach about 20% and maintained low double-digit growth guidance for the full year. We expect 2022-2023 EPS to be RMB0.33 (slightly increase of RMB0.01 by compared with previous report) and RMB0.38 respectively. However, considering that the industry average P/E ratio has fallen to 11.9x, our new TP is HKD4.43, represents 11.3x and 9.96x 2022 and 2023 respectively. Our investment rating is “Accumulate”.

Risk factors

1) Weak domestic growth and consumer spending (including online & lower-tier cities) in sportsware; 2) Intensified competition in the industry; 3) the spread of COVID-19 variants affects the consumer spending; and 4) Slower-than-expected revenue growth.

Financial

Click Here for PDF format...