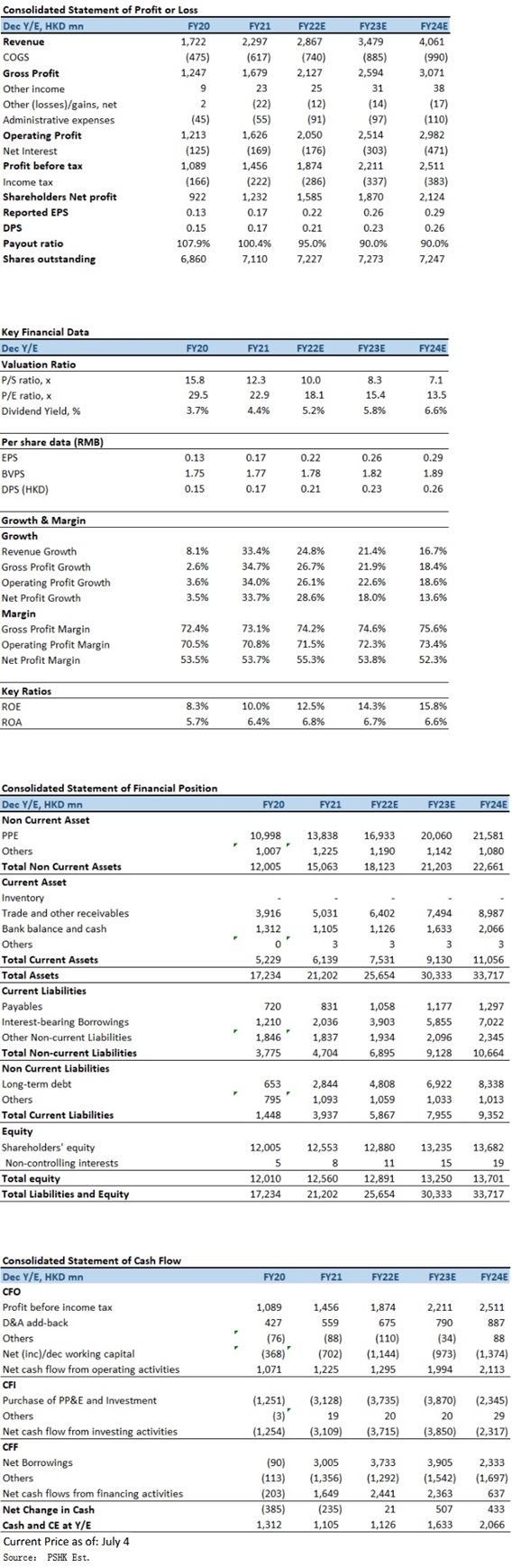

2021 results in line with consensus

During 2021FY, the consolidated revenue of Xinyi Energy recorded an increase of 33.4% YoY to HK$2,296.6 million. Profit for the year attributable to the equity holders surged by 33.7% to HK$1,232.3 million. Basic earnings per share amounted to 17.33 HK cents, a growth of 28.9% YoY. With a final dividend of 10.0 HK cents per share, it represents 99.5% of the distributable income. The full year dividend of 17.4 cents was in line with market consensus.

The Group's revenue was mainly derived from two core businesses, namely, (1) solar power electricity generation and (2) service fee income from the provision of the solar farm operation and management services. The former includes Sales of electricity and Tariff adjustment (represents amount received and receivable from the sales of electricity to the customer pursuant to the government policy on subsidies of solar energy in respect of the Solar Farm Business). Revenue contributed by the sales of electricity and the tariff adjustment significantly increased by 55.8% YoY to HK$1,068.4 million (46.5% of total revenue) and 18.6% YoY to HK$1,218.2 million (53.0% of total revenue) respectively. The Group recorded HK$10.0 million from the solar farm operation and management services rendered for the 2021FY, which represented for 0.4% of the total revenue.

Growth driven by new installed capacity

The increase in revenue was not only due to the increase in sunshine hours throughout the year & a significant increase in electricity generation, mainly attributable to the full operation of the five solar farm projects in the total of 340 megawatts (“MW”) acquired in 2020 (the “2020 Portfolio”) and the completion of the acquisition of the eight new solar farm projects in the total of 660 MW acquired in 2021 (the “2021 Portfolio”). In total, as of 31 December 2021, the aggregated approved capacity of the solar farms projects of the Group amounted to 2,494 MW, as compared to 1,834 MW as of 31 December 2020. In addition, management has increased new solar farm projects acquisitions to 1 GW in 2022 (660 MW in 2021), primarily for grid-parity projects, with half from parent company Xinyi Solar and half from third parties. Going forward, management expects to add 1 GW per year.

During the year, gross profit increased by 34.7% YoY to HK$1,679.4 million, which is in line with the increase in revenue. The increase was mainly due to the greater contributions from both the solar power electricity generation and service fee income from the provision of the solar farm operation and management services businesses. Overall gross profit margin slightly increased by 0.7 percentage point to 73.1%. The increase was primarily due to increase in revenue outweighed the increase in cost of sales.

Trade receivables had a turnover of 646 days and trade receivables amounted to HK$4,628 million, representing a YoY increase of 32.2%; of which, tariff adjustment receivables (government subsidies) accounted for 97.7%. Although all tariff adjustment receivables are expected to be collected (all due from state-owned enterprises, The State Grid Corporation and the China Southern Power Grid), Ministry of Finance does not set out a rigid timetable for the settlement of tariff adjustment receivables and the delay in receiving the receivables may affect the business and financial condition, cash flow and liquidity of the company.

Investment Thesis

In March 2022, the Ministry of Finance released the Report on the Implementation of the 2021 Central and Local Budgets and the 2022 Draft Central and Local Budgets, which mentions "promoting the resolution of the subsidy funding gap for renewable energy power generation". The market expects a big increase in the central government's fund budget expenditure at this level, which may be related to solving the shortfall of renewable energy subsidies. If the renewable energy subsidy shortfall is resolved, the company is expected to reduce its receivables and improve its cash flow position, which will allow it to use more funds to build new projects. We expect 2022-2024 EPS to be HKD0.22, HKD0.26 and HKD0.29 respectively, with PT of HKD4.74, implies a FY22E P/E of 21.6x (~2-yrs historical average) and FY22E yield of ~4.4%. Our investment rating is “Accumulate”.

Risk factors

1) lower-than-normal sunshine hours; 2) lower-than-expected new solar farm projects installations; 3) higher-than-expected acquisition costs; 4) changes in national policies on new energy and subsidies; and 5) higher-than-expected operating costs.

* The analyst has a financial interest in the listed corporation covered in this report.

Financial

Click Here for PDF format...