Investment Summary

Revenue Hits New High in Q1, Core Earnings See Strong Performance

According to the results report for Q1 2022, Fuyao Glass reported operating revenue of RMB6.55 billion, up 14.8% yoy, a new record for the same period and significantly outperforming the overall growth rate of the automobile industry (+2%). We believe that the increase in the unit price of the Company's products and the Company's global expansion of its market share against the trend are the main reasons. The Company also reported a net profit of RMB870 million, up 1.9% yoy and up 58.4% qoq, with a growth rate lower than that of revenue, mainly due to RMB appreciation, increasing freight charges and the rising price of sodium carbonate, the raw material.

In Q1, the Company recorded a gross margin of 35.75%, down 4.85 ppts yoy, mainly due to changes in accounting standards (inclusion of transportation charges in operating cost), RMB appreciation, increasing freight charges and the rising price of sodium carbonate, the raw material. In particular, increasing freight charges/the rising price of sodium carbonate, the raw material/RMB appreciation caused gross margin to fall by approximately 0.76/1.1/0.81 ppts, respectively. Meanwhile, RMB appreciation led to RMB135 million of exchange loss from financial expenses (which was only RMB70 million in the previous period). If the impacts of such factors were ignored, the total pre-tax profit was up 24.4% approximately yoy, and core earnings showed a strong performance.

Product Unit Price Continues to Rise as Product Mix Goes Up

The Company continued to promote product technology upgrading and increase the added value of products, and has been maintaining a high R&D investment ratio in the industry. Driven by them, ASP continued to rise. In 2021, the proportion of high-value-added products, including ceiling glass, HUD, camera glass, coated glass and tempered soundproof car door glass, increased by 3.31 ppts approximately and the ASP of automobile glass increased by 3.8 ppts. In Q1 2022, the proportion of high-value-added products increased by 6.2 ppts approximately, and ASP increased by 9.2% yoy. Specifically, the ASP of the Company's automobile glass continued to grow from RMB132/m2 in 2013 to RMB180/m2 in 2021, and is expected to exceed RMB200/m2 in 2024. In the future trend of automobile glass to be safe, comfortable, energy-saving, environmentally friendly, intelligent and integrated, the Company will continue to reinforce its competitiveness and capability against risks.

Overseas Business Continues to Improve

Overseas competitors have been downsizing automobile glass business in recent years, while Fuyao Glass has been actively upscaling the business with increasing competitiveness. In 2021, the Company's global market share increased by 3 ppts to 31% over the previous year, and it is expected that it will continue to increase to 34% in 2024. In Q1 2022, Fuyao Glass reported a yoy increase of 17.2% and 18.1% in its domestic and overseas revenue, respectively. In particular, the revenue of Fuyao Glass America amounted to USD167 million, up 24% yoy, and its net profit margin was 8% approximately, up 1 ppt approximately from 7% approximately in 2021. The FYSAM plant in Germany also saw its losses further narrowed, and expects to turn losses into gains in H2 as orders are gradually put into production, and it is expected to become the Company's most resilient business in the future.

Headwinds to Gradually Ease, Result Expected to be Stronger since H2

We expect the cost headwinds to gradually ease as sodium carbonate price and freight charges come down from their highest peaks. Furthermore, the trend of RMB exchange rate has been benefiting the Company's performance since the beginning of this year and the Company saw a continuous growth of its global market share and a continuous rise in its product unit price and profitability, which, as we expect, will drive the Company's performance to continue to go stronger in H2. The Company has also raised funds to enter the field of photovoltaic glass, and has been expanding its product scope to open room for long-term sustainable development.

Investment Thesis

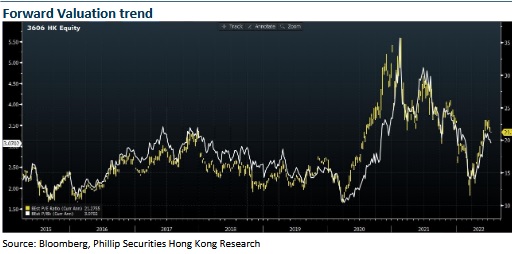

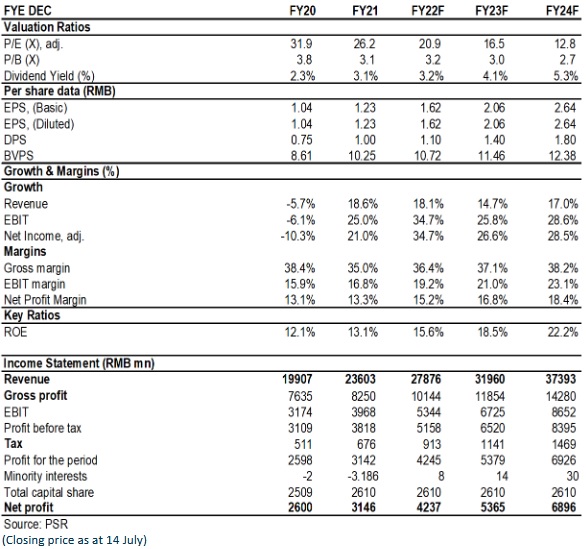

Overall, considering the steady leading position, continuous optimization of the product structure and a high dividend rate, we give the "BUY" rating, with a revised target price to be HK$49, equivalent to 26/20.6/16x P/E for 2022/2023/2024E. (Closing price as at 14 July)

Risks

Demand for automobiles keeps sluggish; cost of raw materials increases; RMB appreciates

Catalyst

Success market development of overseas automobile market; rebound of domestic demand for automobile; depreciation of RMB

Financials

Click Here for PDF format...