Sectors:

Air & Automobiles (Zhang Jing),

TMT, Semiconductors, Consumer & Healthcare (Eric Li)

Automobile & Air (ZhangJing)

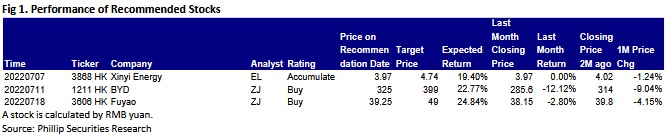

This month I released 2 updated reports of BYD (1211.HK),and Fuyao (3606.HK) which got attention by their unique Competitive edge.

BYD's new energy vehicle sales hit another record high in June: a total of 134,036 new energy vehicles were sold, up163% yoy and 17% mom, which is expected to be higher than the overall rise in domestic new energy vehicles. The cumulative sales volume for the first six months was 641,350 units, up 314.9% yoy, reaching 43% of the annual sales target of 1,500thousand units.

The overall vehicle market picked up in June as the resumption of work and production continued. With strong product competitiveness, the flagship model of the Dynasty series, Han, saw hot sales, recording sharp increases for several months in a row. In June, its sales volume exceeded 20 thousand units for two consecutive months, reaching 25,439 units, up 203% yoy, of which the delivery of Han DMI was up 386% yoy and that of Han EV closed to 13 thousand units. The cumulative sales volume for the first six months exceeded 250 thousand units, continuing to lead the sedan segment of the same class.

The sales of other models of the Dynasty series was also high: 8,134/26,623/32,077/19,731 units of the Tang/Qin/Song/Yuan series were sold in June, up 159%/71.7%/113%/1494% yoy, with a cumulative sales volume of 55,825/146,737/163,356/78,662 units in the first six months.

This year and next are major product years for BYD, which is expected to launch no less than 20 new vehicle models in total, including facelifts. This year, the Destroyer 05, Seal, Denza D9, 22 Tang EVs, 22 Han EVs, DM-i, DM-p and Qin Plus DM-i have already been launched, and in the second half of the year and next year, BYD will continue to launch Denza SUVs, the Warship series, Sea Lion and Seagull. The product matrix will be further improved and, judging from the current optimistic pre-sale situation, the product unit price is expected to continue to see upward breakthrough. In terms of STOP valuation adopt, we give the target price of 399 HK$.

According to the results report for Q1 2022, Fuyao Glass reported operating revenue of RMB6.55 billion, up 14.8% yoy, a new record for the same period and significantly outperforming the overall growth rate of the automobile industry (+2%). We believe that the increase in the unit price of the Company's products and the Company's global expansion of its market share against the trend are the main reasons. The Company also reported a net profit of RMB870 million, up 1.9% yoy and up 58.4% qoq, with a growth rate lower than that of revenue, mainly due to RMB appreciation, increasing freight charges and the rising price of sodium carbonate, the raw material. If the impacts of such factors were ignored, the total pre-tax profit was up 24.4% approximately yoy, and core earnings showed a strong performance.

The Company continued to promote technology upgrading and increase the added value of products. Specifically, the ASP of its automobile glass continued to grow from RMB132/m2 in 2013 to RMB180/m2 in 2021, and is expected to exceed RMB200/m2 in 2024. In the future trend of automobile glass to be safe, comfortable, energy-saving, environmentally friendly, intelligent and integrated, the Company will reinforce its competitiveness and capability against risks.

We expect the cost headwinds to gradually ease as sodium carbonate price and freight charges come down from their highest peaks. Furthermore, the trend of RMB exchange rate has been benefiting the Company's performance since the beginning of this year and the Company saw a continuous growth of its global market share and a continuous rise in its product unit price and profitability, which, as we expect, will drive the Company's performance to continue to go stronger in H2. The Company has also raised funds to enter the field of photovoltaic glass, and has been expanding its product scope to open room for long-term sustainable development. We give the "BUY" rating, with a revised target price to be HK$49.

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

This month I released the report of Xinyi Energy(3868)

During 2021FY, the consolidated revenue of Xinyi Energy recorded an increase of 33.4% YoY to HK$2,296.6 million. Profit for the year attributable to the equity holders surged by 33.7% to HK$1,232.3 million. Basic earnings per share amounted to 17.33 HK cents, a growth of 28.9% YoY. With a final dividend of 10.0 HK cents per share, it represents 99.5% of the distributable income. The full year dividend of 17.4 cents was in line with market consensus.

The increase in revenue was not only due to the increase in sunshine hours throughout the year & a significant increase in electricity generation, mainly attributable to the full operation of the five solar farm projects in the total of 340 megawatts (“MW”) acquired in 2020 (the “2020 Portfolio”) and the completion of the acquisition of the eight new solar farm projects in the total of 660 MW acquired in 2021 (the “2021 Portfolio”). In total, as of 31 December 2021, the aggregated approved capacity of the solar farms projects of the Group amounted to 2,494 MW, as compared to 1,834 MW as of 31 December 2020. In addition, management has increased new solar farm projects acquisitions to 1 GW in 2022 (660 MW in 2021), primarily for grid-parity projects, with half from parent company Xinyi Solar and half from third parties. Going forward, management expects to add 1 GW per year.

During the year, gross profit increased by 34.7% YoY to HK$1,679.4 million, which is in line with the increase in revenue. The increase was mainly due to the greater contributions from both the solar power electricity generation and service fee income from the provision of the solar farm operation and management services businesses. Overall gross profit margin slightly increased by 0.7 percentage point to 73.1%. The increase was primarily due to increase in revenue outweighed the increase in cost of sales.Trade receivables had a turnover of 646 days and trade receivables amounted to HK$4,628 million, representing a YoY increase of 32.2%; of which, tariff adjustment receivables (government subsidies) accounted for 97.7%. Although all tariff adjustment receivables are expected to be collected (all due from state-owned enterprises, The State Grid Corporation and the China Southern Power Grid), Ministry of Finance does not set out a rigid timetable for the settlement of tariff adjustment receivables and the delay in receiving the receivables may affect the business and financial condition, cash flow and liquidity of the company.

In March 2022, the Ministry of Finance released the Report on the Implementation of the 2021 Central and Local Budgets and the 2022 Draft Central and Local Budgets, which mentions "promoting the resolution of the subsidy funding gap for renewable energy power generation". The market expects a big increase in the central government's fund budget expenditure at this level, which may be related to solving the shortfall of renewable energy subsidies. If the renewable energy subsidy shortfall is resolved, the company is expected to reduce its receivables and improve its cash flow position, which will allow it to use more funds to build new projects.

Click Here for PDF format...