|

MORIMATSU INTL(2155)

Analysis:

Morimatsu International (2155) is principally engaged in the design, manufacture, installation, operation and maintenance business, which is mainly applied to the core process equipment, process systems and comprehensive solutions including chemical reactions, biological reactions and polymerization reactions. The downstream industries/sectors served by the Group currently include oil and gas, daily chemicals, new chemical materials, pharmaceutical (including biopharmaceutical and synthetic chemical drugs), raw materials of power battery (including metallic ores and lithium battery raw materials) and electronic chemicals (including the production of photovoltaic raw materials and high-purity chemical reagents), etc. According to its positive profit alert, the consolidated revenue of the Group for the six months ended 30 June 2022 is expected to record an increase of not less than 50% as compared to the corresponding period last year. Such expected increase is mainly attributable to the significant increase in orders from the pharmaceutical industry and raw materials of power battery (including mining and metallurgy) industry. The consolidated net profit of the Group will record an increase of not less than 100% as compared to the corresponding period last year. Such expected increase is mainly attributable to the significant increase in revenue as a result of the expansion of the business scale of the Group and the enhanced production capacity. (I do not hold the above stock)

Strategy:

Buy-in Price: $7.60, Target Price: $8.50, Cut Loss Price: $7.20

|

YNALCO(000807.SZ)

Analysis:

The company is an aluminum company, mainly powered by hydropower. The company currently has 1.4 million tons of alumina and bauxite production capacity, 3.25 million tons of electrolytic aluminum production capacity, 800,000 tons of carbon production capacity, 1.4 million tons of aluminum alloy production capacity, and 170,000 tons of aluminum sheet, strip, foil production capacity, forming a vertically integrated enterprise. The core competitiveness of the company is its geographical advantage. There are abundant bauxite and hydropower resources in Yunnan. In addition, Aluminum Corporation of China recently announced that it will acquire a 19% stake in Yunnan Aluminum. After the acquisition, the company will hold a 29.1% stake in Yunnan Aluminum, becoming the controlling shareholder of Yunnan Aluminum. We expect that after the completion of the acquisition, the horizontal competition between Chinalco and Yunnan Aluminum will be resolved, and synergies between Chinalco and Yunnan Aluminum are more likely to emerge. Therefore, we expect the company will have a medium- to long-term development advantage.

Strategy:

Buy-in Price: RMB9.39, Target Price: RMB13.50, Cut Loss Price: RMB7.20

|

|

Chinasoft (354.HK) - Enrich a New Era of OpenHarmony Ecosystem, Cloud intelligent business as the second curve

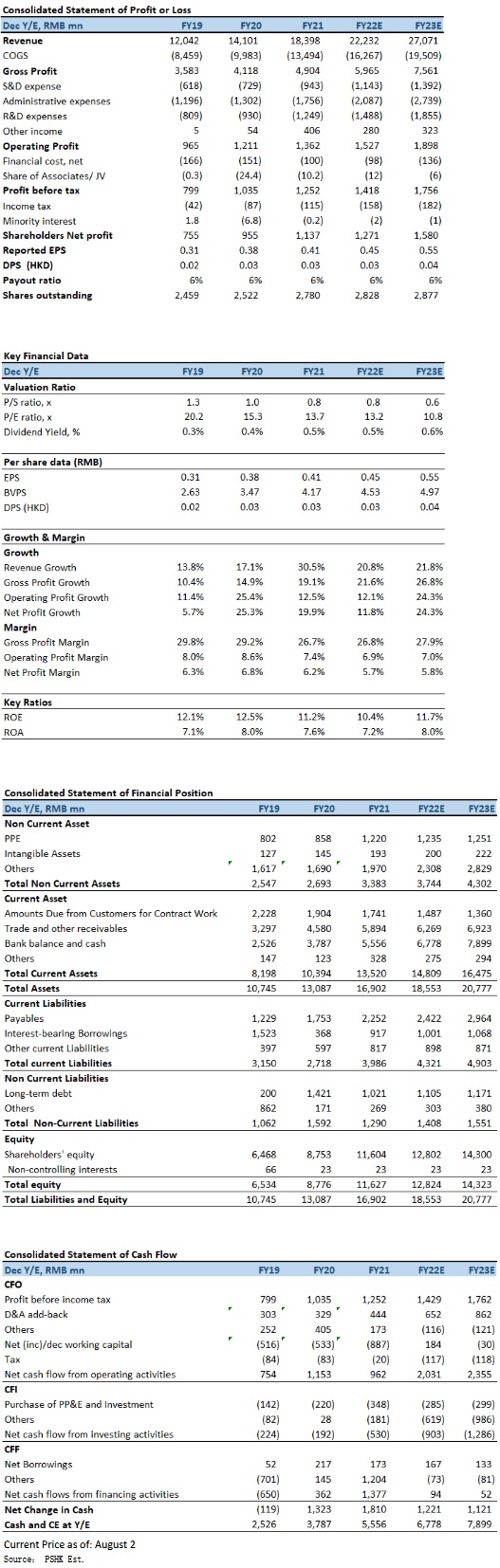

In FY2021, the Chinasoft's revenue was RMB18,398.076 million, representing a YoY growth of 30.5% (FY2020: RMB14,101mn). The service revenue was RMB18,132.013mn, representing a YoY growth of 31.8% (FY2020: RMB13,762mn). The growth was mainly driven by the steady growth of the core large customer business and the rapid growth of cloud intelligent business. Profit attributable to the shareholders was RMB1,137mn (FY2020: RMB955mn), representing a YoY growth of 19.1%. EPS for FY2021 was RMB40.89 cents (FY2020: RMB37.86 cents), representing a YoY increase of 8.0%. In terms of segment revenue, the revenue of TPG was RMB16,622mn (90.3% of total revenue), represented a YoY increase of 34.1%, the increase was mainly from the growth of core clients businesses such as HSBC, Tencent, Ali, Honor and other top ICT infrastructure and smart terminal provider. But the results of TPG just increased 4.1% YoY to RMB1,210mn, which was mainly due to the decline in the gross profit margin of the business during the reporting period and the further increase in R&D investment. The revenue of IIG was RMB1,776mn(9.7% of total revenue), represented a YoY increase of 4.2%, the increase was mainly due to the growth brought by the Internet platform business of the software industry of JointForce. The results of IIG was RMB148mn represented a YoY increase of 19.2%, the increase was mainly due to the improvement in the gross profit margin of the business and the decrease in provision for bad debt. Market share capture, gross margin pressure During the reporting period, gross profit was RMB4,904mn (FY2020: RMB4,118mn), representing a YoY growth of 19.1%. The gross margin was 26.7% (FY2020: 29.2%), representing a YoY decrease of 2.5ppt. The gross margin (to service revenue) was 27.0% (FY2020: 29.9%), representing a YoY decrease of 2.9ppt. The fluctuation of the gross profit margin was mainly due to the company was optimistic about the strategic transformation prospects of major clients, and under the premise of ensuring rapid revenue growth, sacrificed the short-term profits to seize the first mover position and market share; In 2020, the social security provident fund was reduced or exempted, and it returned to normal during the reporting period; Chinasoft increased investment in strategies and new businesses, and increased the reserve of mid-to-high-end technical talents. R&D expenses were RMB1,249mn (FY2020: RMB930mn), representing a YoY increase of 34.3%. During the reporting period, the main reason for the increase was continued to increase its R&D investment in cloud intelligent business and industrial Internet platforms, which further increased the total R&D expenses. In 2021, the R&D expenses accounted for 6.8% (FY2020: 6.6%) of the total revenue, representing a YoY increase of 0.2ppt. As of the end of 2021, the total number of employees reached 92,039, an increase of 21.2% YoY. Among them, the number of technical personnel reached 87,401, accounting for 95% of the total number of employees, including 32,601 project managers, consultants and senior engineers, accounting for 37.3% of the total number of technical personnel. During the reporting period, Chinasoft has 2,083 active customers (the service revenue from the top five and top ten customers accounted for 71.3% & 78.2% of the total service revenue respectively) in 47 countries around the world. Among them, the company has 161 large customers, has a number of Fortune 500 clients including HSBC, Tencent, Alibaba, Honor, Ping An, China Mobile, Baidu, Microsoft, China Telecom, and other top ICT infrastructure and smart terminal provider etc. Company was ranked 80th in the Gartner Global IT Services Market Share TOP100 for four consecutive years, while revenue and profit reached new highs. Seized the strategic window period of OpenHarmonyOS, Chinasoft has actively explored a new business model for the joint operation of OpenHarmony applications and services, expanded more hardware terminal products to join the OpenHarmony ecosystem, and promoted the development of the OpenHarmony ecosystem. The cloud intelligent business group, as the second curve, continued to maintain strong growth. Chinasoft ranked second in the IDC Third-party cloud management service market, and cloud migration and cloud development professional services both ranked first. Financial business steadily improved, added 29 new clients including domestic and foreign banks, private banks, and overseas financial institutions. Continued to cultivate the Internet industry, accelerated the penetration of major clients such as Tencent, Ali, Baidu, etc., while maintaining leading position, continued to expand the clients of wellknown Internet companies such as ByteDance, Meituan, JD.com. Operator IT service business has grown steadily, made breakthrough of acquiring key clients such as Migu Video, Migu Digital Media, China Telecom Tianyi Telecom Terminal, and CEC Hongxin for the first time, and cooperated with operators to promote 5G To B digital factory solutions, covering Aluminum, steel, mechatronics, transportation and other industries. Company valuationSince the listing on the Growth Enterprise Market in 2003, company's revenue and service revenue have maintained rapid growth. From 2003 to 2021, recorded CAGR growths of 29.9% and 37.6% for its revenue and service revenue. The company maintains its FY2022 revenue growth guidance of 20-30% YoY, with a revenue target of $30 billion for FY2023. Chiansoft, SZ Kai Hong Digital Industry Development Co., the People's Government of Tianjin Municipality and Qingdao Guochuang Intelligent Household Appliances Research Institute went into an Agreement for Strategic Cooperation in 2022. Chiansoft will parnter with SZ Kai Hong to popularize and implement OpenHarmony system solutions in the area of the smart city, smart government affairs and smart communities, focus on promoting the adaption and application of commercial release version of OpenHarmony for Party and government, traffic, energy, water conservancy & water service, finance, industry and other fields, facilitate and build an OpenHarmony industrial demonstration zone in Tianjin featured with robust industrial ecology, leading core technologies, resourceful application scenarios and powerful industrial competitiveness by setting up benchmarking model cases. Meanwhile, Chiansoft, SZ Kai Hong and Qingdao Guochuang start from OpenHarmony to develop pan-terminal operating systems in household appliance industry in combination with smart security and scenarized technology. Three parties will jointly promote the development of operating system application components, chips, modules, development board, complete machine and other kits which are oriented to the household appliance field to form a kit of solution for household products from non-intellectualization to intellectualization or low-end intellectualization to high-end intellectualization or from end to end. Moreover, Chiansoft has recently signed a technical service agreement with BYD Auto Industry, to jointly promote the intelligence level of intelligent connected vehicles and accelerate the intelligent upgrade of the automotive industry. we Forcast FY2022E EPS to be RMB0.45, with TP HKD8.21, implies a FY2022E P/E of 15.6x (2-years average). Our investment rating is “Accumulate”. Risk factors1) The pandemic has worsened more than expected; 2) the development of OpenHarmony application was slower than expected; and 3) the development of intelligent cloud business was worse than expected. Financial

Click Here for PDF format...

| Recommendation on 5-8-2022 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 6.940 | | Suggested purchase price | N/A | | Target Price | $ 8.210 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2022 Phillip Securities (HK) Ltd. All Rights Reserved.

|