|

INNOVENT BIO(1801)

Analysis:

INNOVENT BIOLOGICS (1801) announced that during the second quarter of 2022, the Group has generated product revenue of over RMB1,000 million, mainly attributable to the expansion of commercial portfolio and ramp-up of commercial products. It continues to make progress in its pipeline which consists of more than 20 valuable assets, including seven commercialized products, and 20 odd assets in various clinical stages. It keeps advancing the development progress for multiple assets in registration or pivotal clinical trials which supports at least three potential New Drug Application (NDA) submissions in the year of 2022. Separately, it also achieved positive Proof-of-Concept (PoC) data readout for seven novel assets to potentially move forward into the late clinical stage and even NDA submissions in the year of 2022, all with promising market potentials in global and/or regional markets. (I do not hold the above stock)

Strategy:

Buy-in Price: $35.00, Target Price: $38.00, Cut Loss Price: $33.50

|

FARATRONIC(600563)

Analysis:

The company is a leading enterprise in the production of film capacitors. In terms of scale, it ranks first in China and third in the world. The film capacitors produced by the company can be used in photovoltaics, wind power, and new energy vehicles. In 2021, the company`s photovoltaic, wind power, and new energy vehicle revenue accounted for 31% and 27% of total revenue, driving the company`s rapid growth. As cars are becoming more electrified, intelligent, and high-voltage, the quantity and quality of film capacitors in new energy vehicles will increase significantly, raising both the quantity used and the prices of film capacitors. In terms of photovoltaic and wind power, thin film capacitors can protect the connected inverter. We believe that the thin film capacitor business will benefit from the rapid growth of photovoltaics and wind power. In terms of market structure, we believe that the film capacitor industry is shifting to China because China`s manufacturing cost is lower than those of countries producing film capacitors. We believe that Faratronics will benefit from the long-term rapid development of new energy and the localization of film capacitors, hence the company has medium and long-term investment value.

Strategy:

Buy-in Price: RMB199.63, Target Price: RMB234.00, Cut Loss Price: RMB170.00

|

|

Xtep International (1368.HK) - 1H2022 Positive profit alert in line with consensus

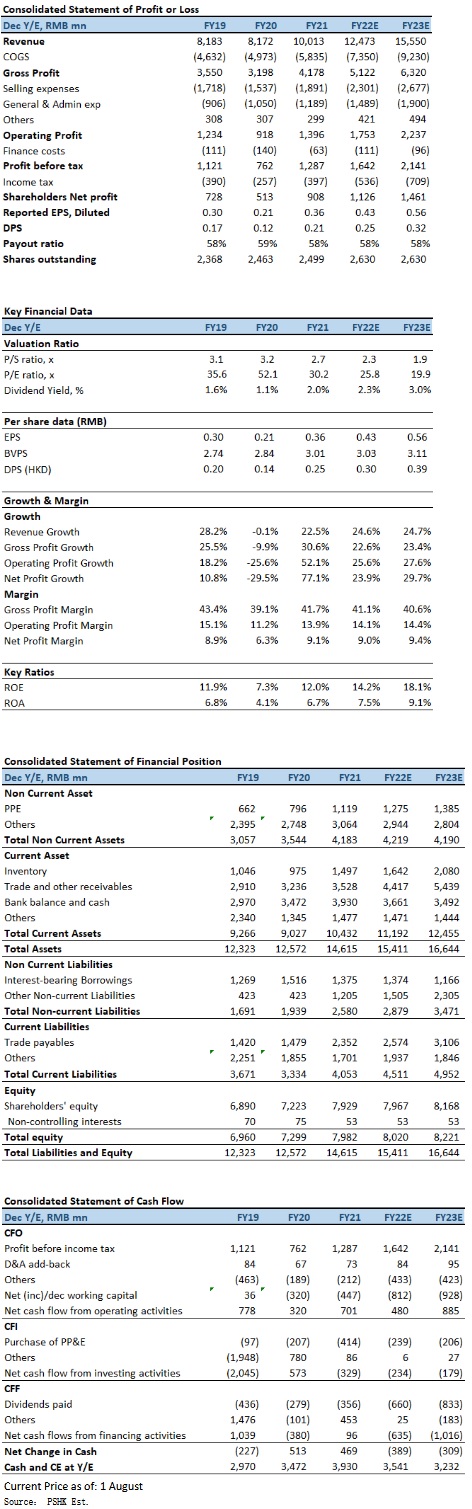

1H2022 Positive profit alert in line with consensus Xtep announced the operation data of 2Q2022. Xtep core brand products retail sell-through (including offline and online channels) grew by mid-teens (30 % – 35 % growth in 1Q2022), retail discount level at 25% – 30% (25% discount at 1Q2022). For the six months ended 30 June 2022, core brand products retail sell-through (including offline and online channels) grew by 20 % – 25 %, and inventory turnover was around 4.5 months (about 4 months in 1H2021, 1Q2022), estimated to be related to the impact of the COVID. Xtep also expected to record a significant increase of not less than 35% in its unaudited consolidated profit attributable to shareholders for 1H2022 as compared to that for the corresponding period in 2021, which is also in line with market consensus. Such increase was primarily due to a not less than 35% growth in consolidated revenue mainly attributable to: (1) remarkable sales fair orders resulting from encouraging retail performance of the core Xtep brand and Xtep Kids` business driven by their breakthrough in product innovation, retail channel upgrade and increased brand awareness; and (2) an impressive YoY revenue growth of over 100% for Saucony under the professional sports segment owing to its strong retail sales particularly in its e-commerce business. Adverse impact of COVID on the economy is fading in June, 618 sales growth 64% The adverse impact of the latest round of COVID outbreaks on the economy is fading, and the resumption of work and production in key cities, core brand products sales are expected to gradually improve. In fact, according to the 618 Shopping Festival sales data in 2022, Xtep recorded a 64% YoY online sales growth to RMB650mn, while the online sales of the core Xtep brand surged 61% to RMB590mn and those of Xtep Kids swelled 103% to RMB75mn. Saucony's even rocketed 135%, the most among all international sports shoe brands during the Festival. Company valuationIn 2Q2022, Xtep's core brand products retail sales growth slowed down due to the impact of the resurgence in pandemic. However, Xtep continues to cooperate with international brand distributors and launched a new store in Tangshan Rongda Shopping Mall with Pou Sheng in July. With the expansion of quality channels, which may help the sales growth of core brand and offset the impact of the COVID in the first half of the year. We adjust our FY2022E EPS forecast to RMB0.43 (down slightly compare with March 2022 report), with TP at HKD13.01, represents of 26.2x P/E (equivalent to the average P/E ratio of the past 2 years plus 1 standard deviation). We downgrade our investment rating to “Neutral”. Risk factors1) Resurgence in COVID in mainland; 2) Weak domestic growth and consumer spending in sportsware; 3) Intensified competition in the industry; and 4) Slower-than-expected in new brands development. Financial

Click Here for PDF format...

| Recommendation on 8-8-2022 | | Recommendation | Neutral | | Price on Recommendation Date | $ 12.800 | | Suggested purchase price | N/A | | Target Price | $ 13.010 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2022 Phillip Securities (HK) Ltd. All Rights Reserved.

|