|

IH RETAIL(1373)

Analysis:

International Housewares Retail (1373) Its retail network comprises 384 stores in Hong Kong, Singapore, Macau, East Malaysia, Cambodia and Australia. For the six months ended 30 April 2022, driven by the growth in overall comparable store sales and the increase in the average ticket size as a result of the surging demand for anti-pandemic supplies, the Group`s revenue increased by 8.5% to a historical high of HK$2,920,775,000. The Group`s gross profit rose by 9.7% to HK$1,334,677,000, while the gross profit margin was 45.7% (2020/21: 45.2%). Profit attributable to owners of the Company was HK$220,822,000. The Board has resolved to recommend payment of a final dividend of HK12.0 cents per share. Together with an interim dividend of HK10.5 cents and a special dividend of HK4.2 cents per share already paid, the total dividend for the Year would be HK26.7 cents per share, representing a dividend yield close to 9%. (I do not hold the above stock)

Strategy:

Buy-in Price: $2.90, Target Price: $3.20, Cut Loss Price: $2.75

|

ND PAPER(2689)

Analysis:

The major contributor of the Nine Dragons Paper(02689)revenue was still its packaging paper business, including linerboard, high performance corrugating medium and coated duplex board, which accounted for approximately 93.3% of the revenue, with the remaining revenue of approximately 6.7% generated from its printing and writing paper, high value specialty paper and pulp products. For the six months ended 31 December 2021, ND Paper achieved a revenue of approximately RMB34,471.3 million, representing an increase of approximately 11.6% YoY. Driven by various uncertainties, which led to a significant economic slowdown in China and affected the demand for packaging paper to a considerable extent. However, the sales volume remained relatively stable and reached approximately 8.4 million tonnes, decreased by approximately 1.6% YoY. The slight decrease in sales volume was driven by approximately 0.2 million tonnes decrease in the China business. The sales volume of linerboard and coated duplex board for the period decreased by 3.5% and 4.4% YoY respectively while high performance corrugating medium for the period increased by approximately 13.6% YoY. As for the costs, due to the soaring prices of coal, chemicals and recovered paper as well as the surging shipping costs, coupled with the launch of green policies in respect of “coal-togas” transition and dual control of energy consumption, the gross profit margin decreased to approximately 13.6% (20.9% for the same period in 2020)。However, the current price of the stock may have reflected many of the negative effects, and it is estimated that the economic measures implemented by the government for boosting industrial development in second half, e-commerce development and the “plastic ban”, the chance of a seasonal rebound increased in the next few months.

Strategy:

Buy-in Price: $6.98, Target Price: $7.70, Cut Loss Price: $6.46

|

|

Xtep International (1368.HK) - 1H2022 Positive profit alert in line with consensus

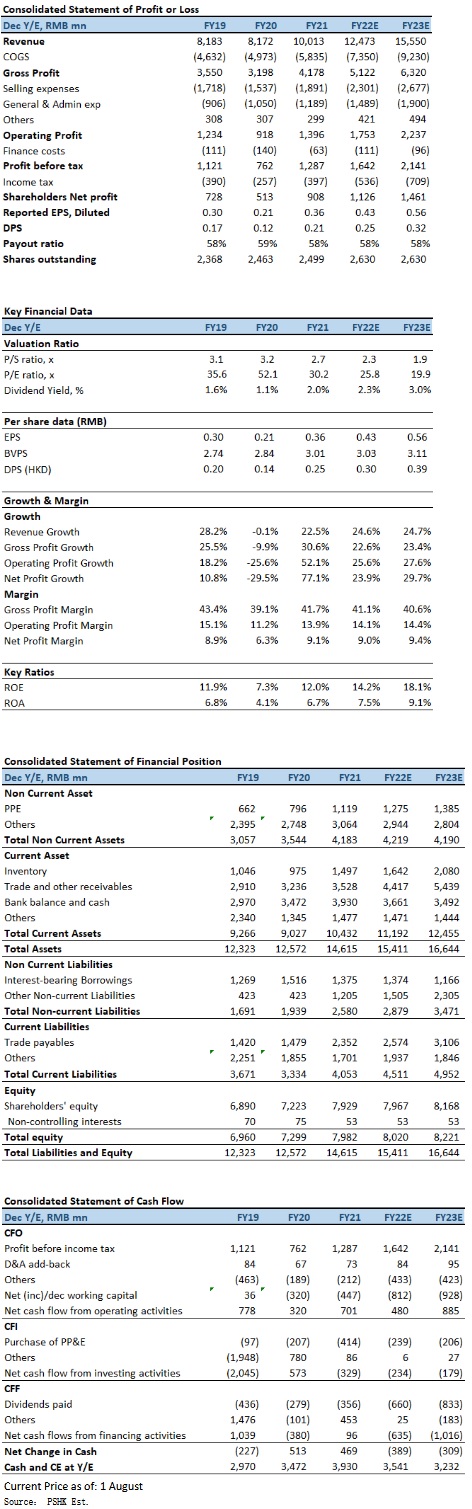

1H2022 Positive profit alert in line with consensus Xtep announced the operation data of 2Q2022. Xtep core brand products retail sell-through (including offline and online channels) grew by mid-teens (30 % – 35 % growth in 1Q2022), retail discount level at 25% – 30% (25% discount at 1Q2022). For the six months ended 30 June 2022, core brand products retail sell-through (including offline and online channels) grew by 20 % – 25 %, and inventory turnover was around 4.5 months (about 4 months in 1H2021, 1Q2022), estimated to be related to the impact of the COVID. Xtep also expected to record a significant increase of not less than 35% in its unaudited consolidated profit attributable to shareholders for 1H2022 as compared to that for the corresponding period in 2021, which is also in line with market consensus. Such increase was primarily due to a not less than 35% growth in consolidated revenue mainly attributable to: (1) remarkable sales fair orders resulting from encouraging retail performance of the core Xtep brand and Xtep Kids` business driven by their breakthrough in product innovation, retail channel upgrade and increased brand awareness; and (2) an impressive YoY revenue growth of over 100% for Saucony under the professional sports segment owing to its strong retail sales particularly in its e-commerce business. Adverse impact of COVID on the economy is fading in June, 618 sales growth 64% The adverse impact of the latest round of COVID outbreaks on the economy is fading, and the resumption of work and production in key cities, core brand products sales are expected to gradually improve. In fact, according to the 618 Shopping Festival sales data in 2022, Xtep recorded a 64% YoY online sales growth to RMB650mn, while the online sales of the core Xtep brand surged 61% to RMB590mn and those of Xtep Kids swelled 103% to RMB75mn. Saucony's even rocketed 135%, the most among all international sports shoe brands during the Festival. Company valuationIn 2Q2022, Xtep's core brand products retail sales growth slowed down due to the impact of the resurgence in pandemic. However, Xtep continues to cooperate with international brand distributors and launched a new store in Tangshan Rongda Shopping Mall with Pou Sheng in July. With the expansion of quality channels, which may help the sales growth of core brand and offset the impact of the COVID in the first half of the year. We adjust our FY2022E EPS forecast to RMB0.43 (down slightly compare with March 2022 report), with TP at HKD13.01, represents of 26.2x P/E (equivalent to the average P/E ratio of the past 2 years plus 1 standard deviation). We downgrade our investment rating to “Neutral”. Risk factors1) Resurgence in COVID in mainland; 2) Weak domestic growth and consumer spending in sportsware; 3) Intensified competition in the industry; and 4) Slower-than-expected in new brands development. Financial

Click Here for PDF format...

| Recommendation on 10-8-2022 | | Recommendation | Neutral | | Price on Recommendation Date | $ 12.800 | | Suggested purchase price | N/A | | Target Price | $ 13.010 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2022 Phillip Securities (HK) Ltd. All Rights Reserved.

|