|

TECHTRONIC IND(669)

Analysis:

TECHTRONIC INDUSTRIES (669) delivered strong results for the first half of 2022. For the six months ended 30 June 2022, it grew sales by 10% to US$7 billion. In local currency, sales grew 12.1%. Combined with its 2021 first half sales growth of 52%, TTI has increased sales by 67% over this two-year period. Net profit rose 10.4% to US$578 million and gross margin improved for the 14th consecutive first half expanding 50 bps to 39.1%. The margin improvement was the result of new product introduction, product mix, category expansion, improvements in operational efficiency and supply chain productivity together with very effective action plans to navigate global supply constraints, commodity headwinds and logistic costs increase. (I do not hold the above stock)

Strategy:

Buy-in Price: $94.00, Target Price: $104.00, Cut Loss Price: $89.00

|

CMS(867)

Analysis:

In 2021, China Medical System(00867)has achieved sustained and steady growth in business performance, and recorded a turnover of RMB8,337.2 million (2020: RMB6,946.0 million), representing an increase of 20.0% YoY; in the case that all medicines were directly sold by CMS, turnover would increase by 24.8% to RMB9,230.2 million (2020: RMB7,395.2 million). Profit for the year reached RMB3,025.3 million (2020: RMB2,555.7 million), representing an increase of 18.4% YoY. Gross profit up 21.7% to RMB6,246.9 million (2020: RMB5,134.2 million); in the case that all medicines were directly sold by CMS, gross profit up 24.7% to RMB6,039.2 million (2020: RMB4,842.7 million). As at 31 December 2021, CMS has acquired nearly 30 innovative products from all over the world. Among them, 9 products had been approved for marketing in the U.S. and/or Europe, and the new drug applications of 3 innovative products were accepted by NMPA. Although the National Volume Based Procurement remained the most influential policy for pharmaceutical companies. Since none of the chemical names of major products sold by CMS was included in the National VBP catalog, thus the policy has not negatively affected the operation and profitability of CMS. It's worth noting that CMS continues to promote its diversified development, and accelerate the incubation and development of new businesses, such as the dermatology and medical aesthetic business, ophthalmology business and healthcare business that are immune to the National VBP, so as to hedge against the potential impact of the CMS 's marketed products that may be included into the National VBP in the future, and further ensure the sustainable business growth of CMS.

Strategy:

Buy-in Price: $12.82, Target Price: $14.00, Cut Loss Price: $11.94

|

|

Xtep International (1368.HK) - 1H2022 Positive profit alert in line with consensus

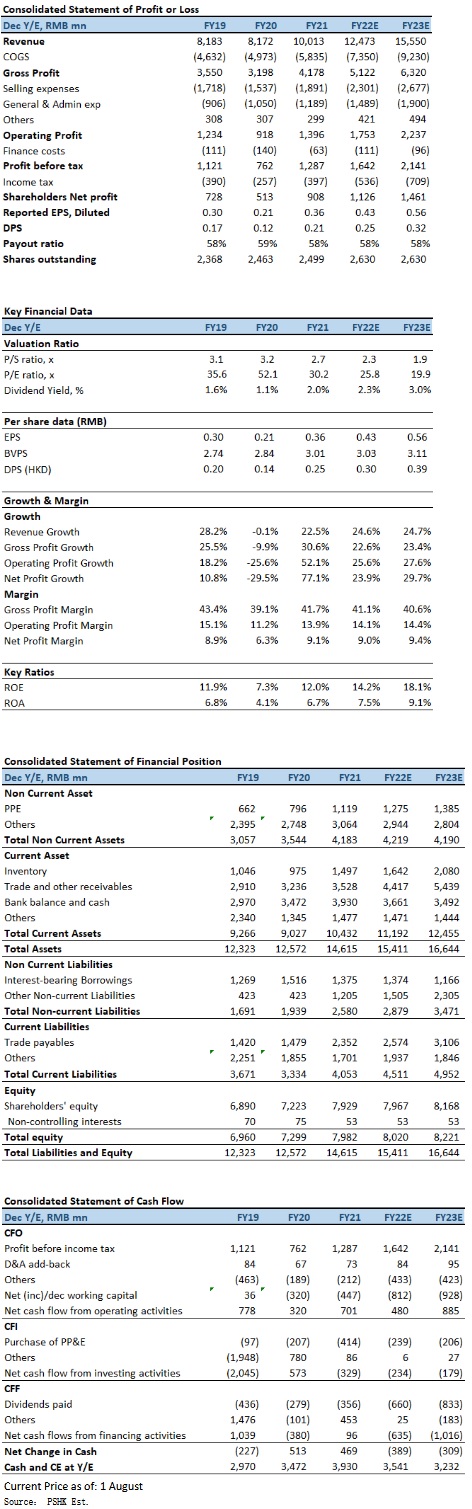

1H2022 Positive profit alert in line with consensus Xtep announced the operation data of 2Q2022. Xtep core brand products retail sell-through (including offline and online channels) grew by mid-teens (30 % – 35 % growth in 1Q2022), retail discount level at 25% – 30% (25% discount at 1Q2022). For the six months ended 30 June 2022, core brand products retail sell-through (including offline and online channels) grew by 20 % – 25 %, and inventory turnover was around 4.5 months (about 4 months in 1H2021, 1Q2022), estimated to be related to the impact of the COVID. Xtep also expected to record a significant increase of not less than 35% in its unaudited consolidated profit attributable to shareholders for 1H2022 as compared to that for the corresponding period in 2021, which is also in line with market consensus. Such increase was primarily due to a not less than 35% growth in consolidated revenue mainly attributable to: (1) remarkable sales fair orders resulting from encouraging retail performance of the core Xtep brand and Xtep Kids` business driven by their breakthrough in product innovation, retail channel upgrade and increased brand awareness; and (2) an impressive YoY revenue growth of over 100% for Saucony under the professional sports segment owing to its strong retail sales particularly in its e-commerce business. Adverse impact of COVID on the economy is fading in June, 618 sales growth 64% The adverse impact of the latest round of COVID outbreaks on the economy is fading, and the resumption of work and production in key cities, core brand products sales are expected to gradually improve. In fact, according to the 618 Shopping Festival sales data in 2022, Xtep recorded a 64% YoY online sales growth to RMB650mn, while the online sales of the core Xtep brand surged 61% to RMB590mn and those of Xtep Kids swelled 103% to RMB75mn. Saucony's even rocketed 135%, the most among all international sports shoe brands during the Festival. Company valuationIn 2Q2022, Xtep's core brand products retail sales growth slowed down due to the impact of the resurgence in pandemic. However, Xtep continues to cooperate with international brand distributors and launched a new store in Tangshan Rongda Shopping Mall with Pou Sheng in July. With the expansion of quality channels, which may help the sales growth of core brand and offset the impact of the COVID in the first half of the year. We adjust our FY2022E EPS forecast to RMB0.43 (down slightly compare with March 2022 report), with TP at HKD13.01, represents of 26.2x P/E (equivalent to the average P/E ratio of the past 2 years plus 1 standard deviation). We downgrade our investment rating to “Neutral”. Risk factors1) Resurgence in COVID in mainland; 2) Weak domestic growth and consumer spending in sportsware; 3) Intensified competition in the industry; and 4) Slower-than-expected in new brands development. Financial

Click Here for PDF format...

| Recommendation on 12-8-2022 | | Recommendation | Neutral | | Price on Recommendation Date | $ 12.800 | | Suggested purchase price | N/A | | Target Price | $ 13.010 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2022 Phillip Securities (HK) Ltd. All Rights Reserved.

|