|

CHINARES PHARMA(3320)

Analysis:

China Resources Pharmaceutical Group (3320) is principally engaged in the manufacture, distribution and retail of pharmaceutical and healthcare products. The Group actively implemented the strategy of “Healthy China”, accelerated innovation and transformation, while continuously enhanced the innovative research and development capabilities, so as to promote the industrial upgrading. Besides, the Group continuously optimised the business structure, field layout and regional layout by empowering the business development with digitalization and driving the efficiency improvement and model innovation, with an aim to continuously improving the core competitiveness. For the six months ended 30 June 2022, the Group recorded a total revenue of HK$125,716.5 million, representing an increase of 9.8% compared to that for the first half of 2021. profit attributable to owners of the Company of INCREASED 24.1% to HK$3,025 million. Going forward, the Group will continuously increase the investment in R&D, the overall innovation investment accounted for a significant increase, of which the intensity of investment in biopharmaceutical research and development exceeded 50%. The Group will enrich its product pipelines by accelerating deployment in the fields of oncology, immunology, cardio-vascular and so on. The development of antibodies, vaccines, recombinant proteins and other products will also be its focus. (I do not hold the above stock)

Strategy:

Buy-in Price: $4.95, Target Price: $5.35, Cut Loss Price: $4.75

|

COSCO SHIP ENGY(1138)

Analysis:

COSCO Shipping Energy Transportation Co., Ltd is a specialized company engaging in the shipping of energy, including oil and natural gas operations, and chemical products. The company`s major business includes international oil shipping, domestic oil shipping, and LNG shipping. We believe that the company will benefit from the rising international oil shipment in the medium and long term. From the perspective of supply, the supply of large oil tankers VLCC has been declining. First, a considerable number of VLCC are gradually retiring. Second, shipyards have limited capacity to produce VLCC. From the perspective of demand, the demand for oil transportation is increasing. First, crude oil production is recovering. Second, the oil embargo on Iran and Venezuela is expected to be lifted. Third, the sanctions on Russia`s oil will increase crude oil shipping distance. We believe that oil shipment will be in short supply in the medium and long term, so COSCO Shipping Energy, the leader in oil transportation, will benefit.

Strategy:

Buy-in Price: $6.37, Target Price: $7.10, Cut Loss Price: $5.80

|

|

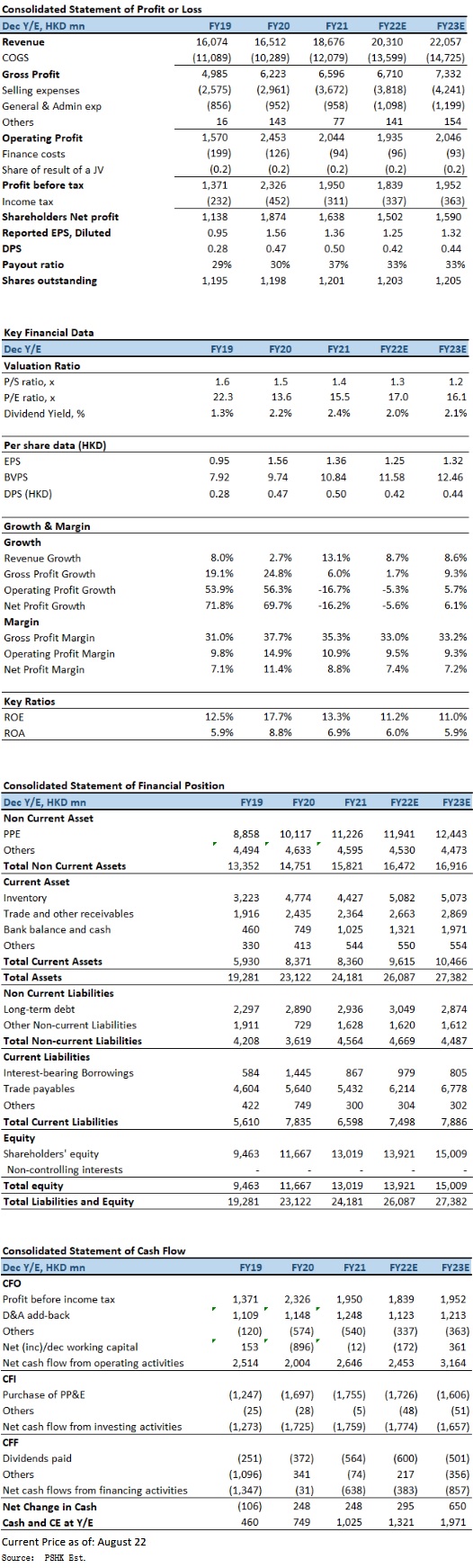

Vinda International (3331.HK) - Focus on Premiumization, implement pricing initiatives to mitigate costs increases

Focus on premiumization, implement pricing initiatives to mitigate costs increases For 1H2022, total revenue of Vinda International increased by 6.6% (growth at constant exchange rates:6.9%) to HK$9,680mn. Overall revenue in 1Q2022/2Q2022 was HK$4,566mn (+2.2%YoY) and HK$5,114mn (+10.8%YoY) respectively. Net profit declined by 34.1% to HK$638mn. Net profit for 1Q2022/2Q2022 was HK$344mn (-37.8%YoY) and HK$294mn(-29.1%YoY) respectively. The net profit margin narrowed by 4.0ppts to 6.6%. Basic EPS was 53.0 HK cents (1H2021: 80.6 HK cents), with interim dividend of 10.0 HK cents per share for the Period. In terms of business segment, the tissue segment accounted for HK$7,963mn of revenue, an increase of 6.1% YoY or 5.9% at constant exchange rates, representing 82% of the total revenue (1H2021: 83%). Focus on premiumization strategy has contributed to an increased share of premium portfolio. This effort to drive higher category margins helped to soften the impact of rising raw material costs and promotional pressures. However, gross margin of the tissue segment was still dropped to 31.6% (1H2021: 37.8%). Revenue from the personal care business increased by 9.0% to HK$1,717mn in 1H2022, which was a 11.7% increase at constant exchange rates and represented 18% of the total revenue (1H2021: 17%). Gross margin of the personal care segment was 34.1% (1H2021: 35.3%). In terms of sales channel, traditional channel, key accounts managed supermarkets and hypermarkets, B2B corporate clients and e-commerce platforms accounted for 26%, 23%, 10% and 41%, respectively, of the total revenue. As the dominant consumption channel, e-commerce revenue recorded an organic sales increase of 14.3%. Gross profit was down by 8.7% to HK$3,100mn. Gross profit was negatively impacted by input costs pressures such as raw material, energy and distribution costs. Vinda took decisive actions including multiple pricing initiatives in mitigating input cost pressures. Although other mechanisms such as disciplined cost management and continuous product mix improvement were also deployed, gross margin was still dropped 5.4ppts to 32.0%. Company valuationCOVID containment measures in mainland China in response to COVID-19 resurgence has led to lower demand and logistic disruptions, Vinda's earnings were also negatively impacted by continuous rise in input (wood pulp prices at high levels) and logistic costs. However, the overall sales performance remained resilient. In addition, believed that Vinda will continue to implement pricing initiatives, and enhance cost management, to mitigate headwinds from raw material and other input costs increases, and expects that this unfavorable situation will be alleviated in the second half of the year. We expect FY2022E-FY2023E EPS to HK1.25 and HKD1.32 respectively, with TP HKD21.0, implies a FY2022E P/E of 16.8x, in line with its 5-years average. Our investment rating is “Neutral”. Risk factors1) Resurgence of COVID-19 in China; 2) Large fluctuations in wood pulp prices; 3) Economic recovery momentum slower than expected, consumer confidence weakens further; and 4) Industry competition is intense than expected. Financial

Click Here for PDF format...

| Recommendation on 29-8-2022 | | Recommendation | Neutral | | Price on Recommendation Date | $ 21.200 | | Suggested purchase price | N/A | | Target Price | $ 21.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2022 Phillip Securities (HK) Ltd. All Rights Reserved.

|